A total of £76 million of investor money is believed to be at risk.

Lawyers for Carlauren investors alleged that Sean Murray transferred significant sums into his own personal account.

Murray responded that the money was accounted for and was just resting in his personal account.

Mr Murray, who represented himself at the hearing in London, previously told the court there were no missing millions and although money had been transferred to his personal account, he said it was being held in trust for the company.

Carlauren CEO Sean Murray puts the writing on the wall. (A joke too bad not to repeat.)

In April Carlauren launched a fraudulent copyright takedown attempt on Bond Review, claiming under penalty of perjury that our articles had been stolen from a made-up Spanish-language blog (which itself consisted of stolen articles from various sources) that somehow managed to review Carlauren’s investments before they existed.

The company then descended into further ignominy as an “Ibiza-style” club on the Isle of Wight failed to open, rubbish piled up outside its properties and elderly residents were thrown out of a Carlauren care home with only hours’ notice as Sean Murray’s latest investment empire crumbled.

Reports of Carlauren’s demise in July, based on a statement from the company that said it had “instructed” administrators, were not so much exaggerated as premature.

Carlauren attempted to appoint its own choice of administrators, but with the appointment of Quantuma and Duff & Phelps, that attempt has failed.

As always we’ll bring you more when the administrators issue their report.

Carlauren reportedly takes its name from a portmanteau of Sean Murray’s two daughters. “Thanks Dad.” Perhaps to avoid further damage to the innocent, the administrators could consider a rename.

Allansons investors watching Companies House hoping for some clue as to where £20 million of their money went will have to wait a bit longer, as Allansons LLP again used the one-day-trick to avoid filing accounts within the deadline.

The Companies Act requires private companies to file accounts within nine months of their accounting year ending, but due to a loophole in UK company law, you can extend the deadline by shortening your accounting period by a single day, which gives you an extra three months.

Allansons deployed this trick in August and now again on 18 November, meaning its last published accounts are now almost two years old.

“I sold the house I owned with my former husband and was looking to invest some money,” she said.

“The Growth Market said the investment was 100% safe and I very naively thought that was true.

“They sent a lot of articles about the courts already ruling that there had been over-charging of mortgage packages and the mortgage companies had set aside millions of pounds for further cases coming up.

“They explained how they’d got this solicitor who was taking up these cases and they were worth a return of 22 to 50% on investment over six to 18 months.

“I’ve been through a very difficult divorce and have been homeless for a while with the children and was just trying to better ourselves.

“I hear on a Facebook action group I’ve joined that some people have put in £100,000 or more.”

Two members of staff listed on The Growth Market’s website are Paul Farhi (who used the name Paul Taylor) and amateur boxer Lee Roberts (using the name Lee Cannon), both of whom served as directors of firms subject to an FCA warnings for allegedly conducting regulated activities without authorisation.

The Growth Market’s website is still up, claiming to offer “investor security in the form of “Asset Backing” or “Insurance Premium” ” and “Low-risk UK-based companies working in a Government Backed Sector”.

The SRA has not yet revealed its reasons for shutting Allansons down, beyond its original notice in May which stated that Roger Allanson had committed unspecified breaches of SRA rules.

In June the SRA’s Intervention Agent informed investors that their contract was still with Allansons (which can no longer acton the cases investors were funding), that they could not offer any assurances that they would be repaid, and that it is unlikely they would be able to claim from the SRA’s Compensation Fund, as this does not cover failed investments in litigation funding.

A crucial court date looms on Monday 25th as stricken Park First investors decide whether to appoint Park First’s own choice of administrators, Smith & Williamson, or rivals Quantuma LLP, proposed by an investor group and US investigators Safe or Scam.

A reminder of where we stand at the moment:

Back when the FCA shut down Park First as an illegal collective investment scheme, £33m of assets were ringfenced by the FCA to meet repayments to investors.

Smith & Williamson claimed that this sum would only be available to investors if they voted to appoint Smith & Williamson, otherwise Park First would withdraw it, and investors would risk getting nothing.

#TeamQuantuma claimed that this was false, and that the FCA had confirmed to Quantuma that the £33m was still ringfenced for investors regardless of which administrator they appointed.

Team Quantuma further claimed that the proposal to appoint Smith & Williamson in a Company Voluntary Arrangement amounted to allowing Park First to remain in charge of the business, writing off £115m owed by Park First group companies to the companies who owe investors money, and signing away their right to take action against the directors.

Smith & Williamson did not respond to my request for comment back in mid-October on whether their claim that investors had to appoint them to be sure of the £33m was “erroneous”. Nor has there been an update on their Park First minisite since 3 October. So make of that what you will.

According to Safe or Scam LLP, an 11th hour update from Smith & Williamson yesterday finally admitted that the £33m was not contingent on investors accepting S&W proposals, but said that Group First could still attempt to block payment if it didn’t get its way over the choice of administrator, which Safe or Scam LLP describe as “scaremongering”.

Quantuma of Solace

Quantuma’s efforts to persuade investors to give it the job (which is likely to be highly lucrative to either S&W or Quantuma, however much remains in the pot) have been stymied by S&W refusing to grant them access to investors’ contact details.

According to Team Quantuma, Group First has been telephoning all investors to try and find out how they will be voting on the 25th November.

Quantuma applied to the court for investors’ contact details so that they could put their own case, but S&W objected.

S&W say, hilariously, that allowing Quantuma to contact investors directly would put investors at risk of being targeted by scammers.

Hilarious because Park First have already been relentlessly targeted by scammers, using silly names like Herschel Escrow and Everton Rose, for months. These scammers generally claim that they know a Chinese investor who wants to buy your parking space for a huge sum, but first you have to put £7,500 in escrow / legal fees / blah blah / and now that money’s gone as well.

The important thing to note here is that Park First investors have confirmed in large numbers that the scammers did not just have their contact details, but knew that they owned a Park First car parking space.

That can’t happen without a major breach of General Data Protection Regulation on Park First’s part. How it managed to let part or all of its investor list fall into the hands of recovery scammers is beside the point (and will hopefully be fully investigated).

For its favoured administrators say that investors can’t speak to a rival in case they get targeted by scammers who already have their details, thanks to the lax GDPR compliance of the people who chose them, is a bit rich.

(Note well here that it does not matter from a data protection perspective whether scammers got hold of Park First investor details through incompetence, a rogue employee or something else. A breach is a breach, including one due to lax security and poor controls.)

The outcome is that the court did a Solomon and gave Quantuma only investors’ names and addresses. As 50% of Park First investors are reportedly in far-flung places like Russia, China and Malaysia, most of them will not receive postal correspondence in time for the 25th.

Team Quantuma has contacted 324 investors via a Facebook group, but this is of no help to victims in China as Facebook is banned there.

As Group First has had no compunction about ringing round investors to influence their vote, it is a bit like if the Tories were using the Government’s own databases to ring round the entire electorate and persuade them how to vote, but refusing to allow Labour to see the same list because “nah it’s data protection innit”.

Decision time

I am not going to tell investors to vote either way, and have no dog in this fight.

With so much money at stake, however, it is crucial that investors can make an informed decision. With that in mind, investors should read the updates from Smith & Williamson andthe counterclaims by Quantuma’s advocates carefully.

If Park First’s own choice of administrators, Smith & Williamson, are appointed, the first job they have is to persuade creditors that they are acting in their interests and not those of the people who appointed them. S&W are a well-established firm and I have no doubt that they will comply with their legal duties to act in creditors’ interests, but that is not the same thing as winning creditors’ confidence; justice must also be seen to be done.

It would be a shame if their first step was to make their appointment look like a stitch-up.

The couple had invested their life savings with Exmount in 2018, after they were promised between 9.12% and 10.35% annual returns on their investment with three- or five-year bonds. The couple began investing a small amount of money, but over the course of a year took out five mini-bonds with Exmount for a total of £45,000.

The pair tried to redeem the unregulated bonds in early August 2019. According to Chan, a company representative asked the couple to pay a £606 exit fee. The pair paid, thinking they could get their capital back, but were then told there had been an error, and were asked to send an additional £606.

Needless to say the couple never got their £1,212 or their £45,000 back.

Note that August 2019, when the customers attempted to redeem their bonds, was months after Exmount Construction had already done a runner and stopped responding to investor queries.

Whether the recovery fraud was perpetrated by Exmount personnel themselves, or whether Exmount sold their contact list to a third party who then contacted the couple claiming to be from Exmount, is unknown, and matters little.

Exmount Construction Limited went through a series of director changes in its final months, with the final director, Rakesh Raj, resigning on 1 August 2019. Raj was also a director of a shell company, ECD Group Limited (it is probably not a coincidence that ECD stands for Exmount Commercial Developments). Exmount Construction is now rudderless with no directors.

What should I do if I invested with Exmount Construction?

Investors who are owed money by an unregulated firm and aren’t being paid have two practical options: 1) seek legal advice from a registered solicitor, and risk throwing good money after bad, or 2) write it off and forget about it.

Investors can also report Exmount’s disappearance to Action Fraud, although they should not expect to hear anything back beyond an automatic acknowledgement.

If investors are cold-called by anyone claiming they can get their money back from Exmount in return for “legal fees” or “admin fees” or any other payment by the investor, it is a scam – just as in the case reported.

Relatively little news has emerged from MJS Capital since then, other than a filing on Companies House showing that a creditors committee has been formed, and the odd tidbit released to the press. The liquidators have not yet released a report into the liquidation of MJS Capital (now Colarb Capital plc) itself.

The liquidators, David Rubin & Partners, have however released a report into MJSC Marketing Limited, a shell company used by MJS Capital to move money.

MJSC Marketing Limited was formed by sole director and owner Nigel Peck, who was described as a member of MJS Capital’s advisory board in investment literature.

He has worked predominately in London, as well as Russia and the USA, with major companies holding both senior management and director positions focusing on marketing, sales, compliance, human resources, and corporate governance, and has many institutional connections. – MJS Capital brochure from 2017

Peck’s last regulated role in the UK was at Park Caledonia Associates, which he left in 2010 according to the FCA register.

MJS Capital CEO Shaun Prince

The administrator reports that he met with Peck and MJS Capital CEO Shaun Prince in September 2018 when MJS Capital was starting to collapse under the weight of winding up petitions from aggrieved investors.

During his discussions, the administrator “grew concerned that investors’ money may have been used for purporses inconsistent with the terms on which it had been invested.”

A week later Peck expressed concerns to the administrator “that the company was being used as a conduit for the misuse of the funds invested by members of the public supposedly into MJS Capital plc”.

Despite being the sole owner of MJSC Marketing, Peck told the administrator that he was not in full control of MJSCM’s bank account, as Prince and another person acting for Prince were “moving funds into and out of the Company’s account without Mr Peck’s knowledge or consent”.

Peck also alleged that MJS Capital had been investing into companies in which Prince had a personal interest.

Peck also alleged that MJS Capital operated as a Ponzi scheme.

Mr Peck also advised me that he believed that investment monies from new investors was [sic] partly being used to pay off older investors who had been threatening MJS Capital PLC with winding up proceedings.

Shortly afterwards Peck accepted the administrator’s advice to place MJSC Marketing into administration.

According to the administrator, this was too late to prevent £300,000 disappearing via MJSC Marketing under “highly suspect” circumstances.

I quickly established that over £300,000 had recently been deposited into the accounts and that in the days preceding my appointment, all of those funds had been transferred out of the accounts at the direction of an employee of Mr Prince. These transactions finally emptied the bank accounts on the very day my appointment took effect. I view that circumstance as highly suspect but the bank was unable to reverse the transactions.

A total of £965,000 was paid from MJSC Marketing to third parties which did not meet MJS’ investment criteria, according to the administrators.

The MJSCM administrators, David Rubin & Partners, have now also been appointed administrators of MJS Capital itself, and the administrators are of the firm view that the affairs of MJSCM and MJS Capital need to be viewed together.

Nigel Peck may not be off the hook either.

No useful purpose can be served by the return of control of this Company to its sole Director, Mr Peck. It is apparent from my enquiries that the conduct of Mr Peck itself may warrant further scrutiny.

With the accounts having been emptied by Prince and his merry men, Peck paid £6,000 into the company, which paid for legal advice from Taylor Wessing and obtaining the court order to liquidate the company. The administrator’s own fees have not yet been drawn.

Krono Partners launched in 2013 and offered unregulated seven-year bonds paying interest of 8% per year, supposedly from investing in distressed real estate in the United States and Europe. It then offered another series of bonds which would supposedly be used to invest in SME bridging loans.

The company went into administration in March 2018, supposedly as a result of bank accounts operated by Jade State Wealth being frozen.

This, it has since become clear, was only the tip of Krono’s problems. Krono holds neither distressed real estate nor bridging loans. Instead over three quarters of its assets (according to the Statement of Affairs) consist of an investment registered in the Cayman Islands known as “Company X” which raises corporate finance via Exchange Traded Notes.

Throughout the period of administration, none of Krono’s investments have paid any returns which could have been used to pay investors’ returns of 8-10% per year, even if it hadn’t gone into administration.

Company X is now Company Y

Hopes of investors getting any of their money back rest largely on Company X paying commission from its fundraising to Krono, in return for the money Krono invested in it. When Smith & Williamson were appointed as administrators, Krono management claimed that investors could expect repayment in full.

The administrators have now revealed that Company X can’t actually pay any commission to Krono because of regulations in the Cayman Islands. Whoops.

Thankfully, a way around this has been found which involves a new Company Y being set up in Hong Kong, and has seemingly replaced Company X.

No commissions have yet been received from Company Y either. The administrators list five “key projects” being undertaken by Company Y which are at various stages of fundraising; none have yet reached the stage where they pay Krono (and in due course their investors) any money.

Other than cash in the bank, Krono’s other assets consist of relatively small amounts in shares and micro loans, which are also yet to return anything. A “Company B” in which Krono owns 4 million shares is due to list on the Canadian Stock Exchange by 31 December 2019.

The biggest payment the administrators have received so far is in question. £85,000 was received under “other debtors” which were “relating to the sale of an equity interest”. Subsequently the administrators were paid another £16,649. The unnamed payer is now claiming that only the £16,649 was due and the £85,000 should not have been paid.

The £85,000 / £101,000 is by far the biggest realisation made to date (the only other being £42k in a trading account and cash in the bank) so it will be a blow if it turns out that most of it has to be handed back. Total receipts in the administration to date currently stand at £143k, while the administrators’ costs so far stand at £154k.

The Financial Conduct Authority reviewed Krono Partners in 2014, shortly after launch. After four months it closed its case and took no further action.

Krono is one of a number of failed unregulated investments currently in administration with Smith & Williamson, alongside London Capital & Finance and Park First.

A meeting of victims in the collapsed Park First investment scheme to approve the administrators’ proposals has been adjourned to 25 November, after a proposal to appoint alternative administrators was not included on the agenda.

Smith & Williamson (also administering Reyker Securities and London Capital and Finance) were the choice of Park First’s directors.

US-based Safe or Scam LLC has proposed an alternative administrator, Quantuma LLP (currently attempting to gain control of collapsed care home investment scheme Carlauren Group).

Safe or Scam characterise Smith & Williamson’s proposals as amounting to the write off of £115m of debt owed by Park First group companies to the companies in administration.

The administrator’s report confirms that the four Park First companies involved in the CVAs are owed a total of £115.4m by other companies in the Park First group, but that this £115.4m “has no recoverable value”.

They are actually saying that these four Park First companies transferred £115.4m to other group companies and there is no chance of recovering that money for the investors ! There has been no explanation why this money was transferred nor any explanation as to why is cannot be recovered. The administrators are just expecting creditors to accept a loss of that magnitude because they tell them to. So….. if creditors vote FOR the CVA proposals what effect would this have ? Well, if they vote FOR the proposals they would be agreeing to the following:

To write off £115.4m where the administrator has not even told them which companies took the money, why they were paid the money and why it is not possible to recover it; and

To sign away their rights to be able to take any form of recovery action against any of the parties involved; and

To allow the existing management to continue to run the businesses without any investigation into their conduct or the possible misappropriation of funds.

I asked S&W for comment on whether this was an accurate description of their proposals a week ago, and have not received a reply.

In a subsequent blog post on Saturday 12th October, Safe or Scam accused S&W of misinforming creditors by implying that a proposed £33m cash injection from Group First companies was contingent on Smith & Williamson’s proposals (including the £115m debt write off) being accepted, and the company entering a Company Voluntary Arrangement.

In short: either take £33m or risk getting nothing.

According to SOS, this was “erroneous”; the FCA has confirmed to rival suitors Quantuma LLP that the £33m should still be available to a liquidator, whether the original proposals are accepted or not.

The meeting of creditors has been rescheduled for the 25th at City Temple Conference Centre, London.

Comment

The rescheduled meeting sets up an intriguing clash for the fate of the administration between the Park First directors’ chosen administrators and Safe or Scam’s.

The parallel between London Capital & Finance and Park First goes beyond the fact that the unrelated collapses of both are being cleaned up by Smith & Williamson.

In both cases Smith & Williamson were appointed by the directors of the unregulated investment schemes themselves.

There is of course no suggestion that S&W are failing to carry out their statutory duties to act in the interests of creditors, over the people who appointed them if necessary.

There is also no question that the first job of an administrator of a collapsed unregulated investment scheme is to win the trust of creditors – and this goes double when the administrators were appointed by the people who lost their money in the first place.

Smith & Williamson’s appointment to London Capital & Finance was followed by a series of gaffes, which included unquestionably parroting the idea that LCF investors were sophisticated and high-net-worth (which very quickly turned out to be false), and saying on national radio that it was a good thing that LCF invested in a handful of companies linked to the directors, rather than hundreds of SMEs as investors had been led to believe, because it made the administrators’ job easier.

(Which is true, but the kind of thing you should look over your shoulder before saying if you’re at the Friday night office social, and is a downright stupid thing to say on national radio in front of stricken investors.)

S&W also claimed in the same interview that “the numbers all add up” and suggested investors could hope to get their money back; only to later reveal that what the numbers added up to was 80% losses as a best case scenario.

All that has however been left in the past, and there was no serious attempt to replace S&W with completely independent administrators of LCF investors’ own choice. Nor has there been any suggestion that S&W hasn’t maximised recoveries so far.

By contast, in the case of Park First Safe or Scam are accusing Smith & Williamson of being far too quick to effectively write off £115m of intercompany loans by proposing a Company Voluntary Arrangement.

Whichever choice the investors make, no-one can deny that more scrutiny over where the money went and whether it can be recovered is sorely needed.

Park First investors sue Park First and its directors for “fraudulent misrepresentation”

In other Park First news, a group of Park First investors are suing both Park First itself and Park First owner Toby Whittaker personally, alongside others including Park First director Ruth Almond, the Evening Standard reveals.

The investors are seeking £6 million which suggests that they represent a relatively small percentage of Park First investors.

A key part of the scheme was that the Park companies would sub-lease the plots back from the investors, offering a guaranteed return of 8%. The company said “projected returns” would rise to 10% in years three and four and 12% in the two following years.

In fact, the claim says, the sub-leases only lasted for two years, after which Park broke them and failed to provide subsequent services, leaving the plots impossible to sell. The investors also claim Whittaker’s companies misled them that they would easily be able to sell their spaces if they wanted to. There was no secondary market to buy them, which Whittaker knew, the case alleges.

The claim says some of the car parks in Glasgow were fenced off, making it impossible for them to return the kinds of profits being promised.

Park First director Ruth Almond said “The action will continue to be defended. We believe investors would be better served by pursuing options set out by the administrators.” That would be the option which apparently involves writing off most of the liability owed by Park First discussed above, then.

In general it takes exceptional circumstances for directors to be held personally liable for the failings of their companies; limited liability companies are called that as a reason.

Whether such circumstances exist remains to be proved in court.

Sadly, people investing lots of money in obscure micro-cap unregulated investments and losing all their money is not in itself an exceptional circumstance.

The FCA’s action alleges that Park First was an illegal collective investment scheme, which we already knew as that was why it was originally shut down in late 2017 (not 2016 as the Standard says).

More seriously, the FCA alleges that Park First’s directors claimed the parking spaces were being sold at a 25% discount, based on independent valuations, but were “aware that the valuations were based on unrealistic returns”.

The FCA is suing Park First owner Toby Whittaker, director John Slater, Park First and numerous other connected firms, demanding the defendants repay a “just sum” to be distributed to victims.

The FCA has justified its lack of previous action, which allowed Park First to remain in control of the scheme’s assets, and its attempts to return the money to Park First investors, on the basis that if it had wound up the companies earlier, it might have made it less likely that investors got their money back.

Whether leaving Park First and its directors in overall charge of the money for another one-and-a-half years succeeded in increasing recoveries for investors remains to be seen.

In the original settlement in late 2017, the FCA secured a “promise” from Park First not to dispose of their assets, and ringfenced the sale proceeds of a car park at Luton Airport plus a further £1 million – £33m in total – to meet buyback payments for investors. This is the payment at the centre of the dispute above.

Last month it was revealed that the Financial Services Compensation Scheme has compensated investors in Providence Bonds and Secured Energy Bonds in full (up to £50,000), paying out a total of £10 million (£5 million for each).

Providence and Secured Energy Bonds paid interest of 8.25% and 6.5% per year. Both collapsed with total losses to investors.

Investors brought Financial Ombudsman claims against Independent Portfolio Managers, who approved the schemes’ literature, enabling the investments to be promoted to retail investors. These complaints were initially rejected on the basis that they were not customers of Independent Portfolio Managers, Providence / SEB was.

The investors took legal advice, and before the matter went to court, the FOS changed its mind and began looking into complaints against IPM. An Ombudsman found against IPM in three published cases. IPM went bust shortly after, over an unpaid regulatory fee.

Those FOS decisions against IPM allowed the investors to claim on the FSCS.

Last year I poured cold water on the hope that investors would be compensated, saying that if the FSCS did so, it would effectively make all unregulated investments risk-free, provided the investment wasn’t too lazy to jump through the hope of finding an FCA-regulated company – any FCA- regulated company – to approve its literature.

Naturally I am delighted for the investors that I have been proved wrong. And in fairness, I was in good company. The FOS also initially rejected investors’ complaints. And back when Secured Energy Bonds and Providence Bonds were being promoted to investors, nobody told them that the investments were in fact 100% risk-free (up to £50,000) by virtue of the fact that the literature was misleading and approved by the investment’s Corporate Director.

(undermisselling (n.) – The act of an FCA-regulated company selling a supposedly guaranteed investment that is too good to be true, and by thus misselling it, making it actually true, but not making it clear that it is too too good to be true to not be true.)

I have previously asked: if investors are compensated on the basis that IPM was personally liable to them for misleading literature, does this mean any investment with Section-21-approved misleading literature is risk-free?

Independent Portfolio Managers was specifically sanctioned by the FOS for promoting security features of the investment (the fact that the bonds were secured loans and the existence of a Security Trustee) without equally prominently highlighting the risks (the fact that secured loans can still lose all your money and the Security Trustee, which was none other than IPM, was as much use as a chocolate fireguard).

The FOS found IPM was liable directly to investors because it not only approved the literature, but acted as Corporate Director and Security Trustee to the bonds.

Part of the reason IPM’s expertise is relevant over and above their ability to review the materials is that it had an ongoing role in the investment scheme, approving new documents as they are created.

The expertise is relevant to IPM’s status as Corporate Director which was a non-contingent role that was promoted as part of the security of the bond. And IPM’s expertise was relevant to its contingent but nevertheless prominently proclaimed status and role as Security Trustee by which it might have to intervene to manage the investor’s asset. IPM was in effect being advertised as a manager of the investor’s assets upon a condition being met: this is an active (albeit contingent) managerial role,to which IPM’s expertise is relevant.

[…] The purpose of IPM’s involvement in the arrangements was to bring about the investment.

I can think of many unregulated bonds with literature approved by an FCA-regulated third party, but none of the top of my head where the same third party acted as Security Trustee or Corporate Director, that are still in business.

The FOS might still find the company that signed off the literature liable for “bringing about the investments” – anything’s possible – but its decisions against IPM are not a precedent.

(I’m using precedent in a general sense – FOS decisions do not set legal precedent in the same way a court case does.)

Good news for payers of FSCS levies that the practice of FCA-regulated companies misselling bonds and also acting as Security Trustee, in doing so making them FSCS-eligible, appears to have ended.

If only the same was true of the practice of FCA-regulated companies misselling unregulated bonds at all.

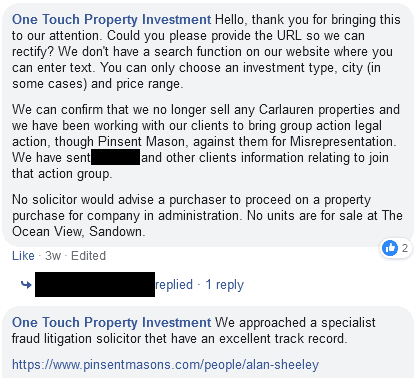

On the public Facebook group Sandown Hub, a resident of Sandown noticed that one of its former introducers, One Touch Property Investment (officially One Touch Solution Ltd), was apparently continuing to sell units in its care home.

One Touch clarified that it was no longer selling Carlauren investments. In the ensuing thread, it revealed that it has approached a “fraud litigation solicitor” on behalf of investors to pursue Carlauren over “misrepresentation”.

(The conversation below took place in the public domain, in a public Facebook group, but personal names have been blanked as a courtesy.)

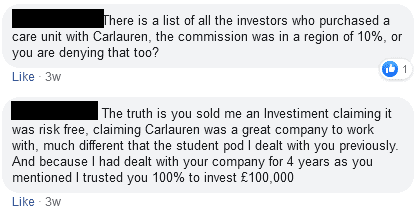

Angry clients of One Touch queried One Touch’s own role, accusing it of taking 10% of Carlauren investors’ money in commission.

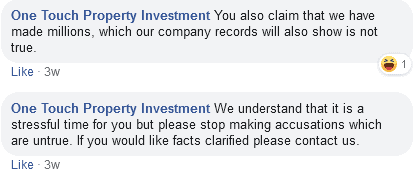

One Touch did not deny taking 10% in commission, though it did dispute a supposed accusation that it made “millions” (no investor actually mentions “millions” in the thread).

What One Touch’s company records actually show is: not a lot. The company has consistently used small company exemptions and does not publish its profit and loss account via Companies House, meaning that how much One Touch received for selling Carlauren investments is unknown.

Several investors suggested One Touch should refund to investors the commission it made from selling Carlauren investments. One Touch did not respond to these requests.

Administration update

Three Carlauren entities are already in administration, with Quantuma LLP appointed as administrators: Carlauren Lifestyle Resorts, Carlauren Care and Accordiant. The latter was responsible for the committment to pay returns of 10% per year to investors.

Quantuma recently revealed, in their initial report into Accordiant, that they have applied for the wider Carlauren group into administration. As at September 2019 an initial hearing had been adjourned, and the Administrators are awaiting a hearing date.

In the meantime, director Sean Murray has been required “to give undertakings to the Court that each of the respondent companies’ assets will not be disposed of or dealt with in any way other than the ordinary course of business”.

Carlauren’s directors are opposing their application to put the wider Carlauren Group into administration and have challenged the validity of the current Administration.

Carlauren itself is adopting either an ostrich or “lights are on but nobody’s home” approach to the administration. Carlaurengroup.com now redirects to carlaurenlifestyle.com, which makes no mention of the administration.

The administrators of Asset Life have released their initial report.

Asset Life plc, reviewed here in January 2018, raised £8.9 million from investors in three unregulated minibond issues (A, B and C). At the time of my review they were offering 8.75% per year for a three year term.

When the A and B investors were due to be repaid, Asset Life failed to do so. Asset Life plc asked for 12 months’ grace, which some gave, but others refused. Asset Life was unable to repay those investors who insisted on getting their money back. Interest payments stopped in November 2018.

What regulated activities the FCA thought Asset Life plc might be up to is still unclear (even the administrators say they are still in the dark on this point). Raising funds in unregulated minibonds is not a regulated activity, nor is investing them in random mines in Elbonia.

Nonetheless the warning had the effect of preventing Asset Life plc from taking new money in from its Series C bonds, “leaving it with insufficient working capital to meet its existing obligations” (which glosses over the fact that Asset Life plc hadn’t had enough money to meet its existing obligations since it defaulted on the Series A and B investors and stopped paying interest in November 2018).

Asset Life went into administration three months later in August 2019.

The investment

Investors’ funds were to be used to invest in companies with significant growth potential.

Only two such companies remain: Aprelskoe, which is not a virulent Swedish liqueur but a Kyrgyzstani gold exploration company, and Lori Iron and Steel, an Armenian iron ore extraction company.

According to Asset Life plc’s directors, neither is capable of returning any funds without throwing good money after further investment.

The administrators have been advised that there is no realistic prospect of selling Asset Life plc’s shares in Aprelskoe or Lori except to the companies themselves or a connected party.

The administrators therefore intend to continue holding the investments while they continue discussing with other shareholders.

According to the administrators, all of Asset Life plc’s other investments resulted in total losses.

With wearisome predictability, the Asset Life plc directors blamed Brexit for the company’s collapse.

The directors explained to bondholders that there were various reasons for the delay in repayment of the loans, including poor market conditions as a result of the UK’s current political situation, and the uncertainty of Brexit hampering investment decisions.

How specifically Brexit is to blame for Asset Life plc’s failure is unclear. The fall in Sterling after the 2016 referendum should have made it easier to pay back investors’ money in Sterling using revenue earned overseas in obscure ex-Soviet satellite states, not harder.

Prospects for return

Series C bond investors are being treated as secured creditors while Series A and B bond investors are being treated as unsecured.

A Security Trustee was initially in place for the Series A investors but the Trustee company was dissolved shortly after funds were raised.

The fact that Asset Life plc’s old investors are outranked by their new ones could come as a kick in the teeth, if of course Asset Life plc does actually manage to realise any returns for bondholders at all after paying the administrators’ fees. This would appear to be extremely uncertain.

Director Martin Binks failed to provide a proper Statement of Affairs, instead submitting only previously published accounts and a schedule of bondholders (not a full list of creditors), plus “various items of loose paperwork”.

The administrators have done their best to provide their own schedule, but their list of assets has £8,000 of cash in the bank as the only asset with any known value, with all other assets listed as “nil” or “uncertain”.

What happened to the Lenders Guarantee and insurance?

As late as July 2017, Asset Life plc claimed on its website that funds were guaranteed up to £250,000. In October 2016, this guarantee was supposedly provided by GEF Guarantee Equity Fund Limited.

[Our Fixed Interest Plan] offers an inclusive Lenders Guarantee by GEF Guarantee Equity Fund Limited which protects both the deposit and interest promised to our clients at Asset Life.

GEF Guarantee Equity Fund Limited was a company in Israel owned by a UK company, GEF Guarantee Equity UK Limited. In October 2016, the UK parent had already been in liquidation for half a year.

At some point between then and July 2017, Asset Life plc replaced this with a similar Lenders Guarantee – still with “Capital deposit and interest protected up to £250,000” – this time covered by Klapton Insurance, headquartered in Anjouan, a small island in the Indian Ocean.

However in February 2018 the claim that the insurance guaranteed investors’ capital was removed and replaced by the more vague “an active form of indemnity insurance to cover the Loan”. The insurer was not named except as “underwritten by A rated (AM Best) Rated insurers, either Lloyd’s of London or Company markets”.

Of these various insurance policies there is no mention in the administrators’ report.

Around February 2018, the FCA-regulated company responsible for signing off Asset Life plc’s website switched from Opus Capital to Equity For Growth (Securities) Limited.

Asset Life plc Chairman Martin Binks is well-experienced in the unregulated minibond sector.

Binks was a director of collapsed minibond firm London Capital & Finance from October 2015 to August 2016.

Since May 2014 Martin Binks has been a director of another former minibond firm, Anglo Wealth Limited.

In December 2018 Anglo Wealth Limited was described as an “elegantly packaged scam” by a Southwark Crown Court judge, who sentenced two other Anglo Wealth directors, Terrence Mitchell and Andrew Meikle to suspended prison sentences and disqualification as directors.

According to the administrator’s report, Mitchell remains Asset Life plc’s joint-largest shareholders with a 10% share (banned directors are not banned from being shareholders).

Binks was not part of the criminal case and has not been accused of any wrongdoing in relation to his ongoing role at Anglo Wealth.

Despite the fact that the bulk of the Anglo Wealth funds were “dissipated on supporting the defendants’ lifestyles”, according to lawyers advising the CPS, Anglo Wealth investors were repaid in full.

The connections between Asset Life plc and Anglo Wealth are identified as an “area of specific concern” by the administrators.

We are aware that certain individuals previously involved in managing Asset Life plc were disqualified in acting in the promotion, formation and management of any company following criminal proceedings relating to a predecessor company, Anglo Wealth Limited (AWL). The Company’s audited accounts show that Asset Life plc acquired a number of its holdings from AWL in consideration for writing off an intercompany debt. We are therefore investigating the relationship between AWL and Asset Life plc, and the nature and extent of the intercompany transactions.

So, just to make sure everyone is following along:

Anglo Wealth raised just over £1 million from investors (according to its 2017 accounts, the last filed before it repaid investors).

Anglo Wealth was, according to the judge that sentenced Meikle and Mitchell, an “elegantly packaged scam”.

According to lawyers assisting with the prosecution, “Unusually for a prosecution of this type, the investors were re-paid in full (albeit only after the pair knew they faced criminal investigation)”.

Anglo Wealth managed to find money to repay the investors despite the fact that the investors’ money was already gone, Anglo Wealth having “dissipated the bulk of the funds on supporting the defendants’ lifestyles.”

In part due to the fact that Anglo Wealth managed to repay its investors with other money from sources unknown, Mitchell and Meikle did not see the inside of a prison cell, receiving only suspended sentences plus fines totalling £250,000 (less than a quarter of the amount they scammed from investor).

Asset Life plc, described by the administrators as Anglo Wealth’s successor company, raised a total of £9 million from investors between 2014 and 2019.

Anglo Wealth borrowed money from Asset Life plc (this is the intercompany debt referred to in the administrators report).

This intercompany debt was settled by Anglo Wealth passing holdings to Asset Life plc.

All these holdings received from Anglo Wealth to settle this debt to Asset Life have either gone bust with total losses, are of uncertain value, or were realised before the company defaulted on its investors and entered administration.

The administrators’ investigations continue.

…The lack of accounting records and the involvement of numerous third party payment agents has made the task of reconciling the Company’s financial affairs extremely challenging.

Due to the lack of transparent information on the trading transactions of this Company, we anticipate that these investigations may take some time. In addition, our investigations are likely to require the use of Insolvency Act 1986 powers to compel the provision of information from third parties.