The administrators of collapsed minibond scheme Asset Life plc have released their latest six monthly report.

Unfortunately there’s been little reportable progress, with the two investments that form the ashes of Asset Life plc, Kyrgyzstani gold hunter Aprelskoe and Armenian metal grubber Lori Iron and Steel, continuing to blank the administrators. The administrators continue to attempt to extract blood from both stones but say they “do not anticipate material realisations in this regard”.

There’s also been no further revelations on how Anglo Wealth plc, an “elegantly packaged scam” which shared two senior personnel in common with Asset Life plc was able to repay the investors in Anglo Wealth, despite having already spent their money: Asset Life plc chairman Martin Binks was an Anglo Wealth director (and ex London Capital and Finance director). Asset Life plc shareholder Terrence Mitchell was also an Anglo Wealth director. Unlike Mitchell, Martin Binks was not party to the criminal case against Anglo Wealth and is not accused of any wrongdoing.

Investigations remain ongoing into the marketing claims made by Asset Life to investors, the supposed insurance arrangements, and where the money went.

The administrators time costs currently stand at £188k, having long blown through the £8,000 that was in the bank on appointment, and remains the only asset to realise any value as things stand.

The administrators of collapsed cryptocurrency bond scheme Viderium have released their initial report.

According to the report, a potted history of Viderium is as follows:

Viderium raised a total of £4.1 million in its bonds starting in February 2018.

£940,000 was invested in cryptocurrency mining machines, which were mostly deployed in Riga, Latvia and Rotterdam, Netherlands in summer 2018.

What was done with the other £3 million of investors’ money is not elaborated on in the report.

Until the cryptocurrency crash in late 2018, the company was apparently making revenue of $10,000 per day. With $1 worth about 75p at the time, that would have translated into about £2.7 million a year – which is pretty much exactly what Viderium were targeting in year 1 according to its investment brochure.

However, after the cryptocurrency market crashed, revenue dropped to $1,000 a day. The administrators are presumably referring to the crash of late 2018 when Bitcoin crashed from ~£5,000 in November 2018 to ~£2,700 in December 2018. It can’t be the crash of early 2018 when Bitcoin crashed from ~£12,500 to ~£5,000, because that had already happened when Viderium raised the bulk of its funds and deployed its mining machines.

If anyone’s wondering how a halving of the Bitcoin price translates into a literal decimation of Viderium’s revenue, I assume it’s because Viderium was mining cryptos other than Bitcoin. Exactly which cryptos Viderium would mine was not specified in the investment literature.

Despite Viderium signing investors up for a three year term, and the cryptocurrency market recovering six months later (Bitcoin was back to £5,000 and higher by May 2019), this didn’t save the company’s business model. Viderium resorted to hiring out director Ross Archer and his “experience in marketing and sales” to other companies. This also failed to bring in enough money to keep the scheme afloat.

(Shame they didn’t manage to keep any of that £3 million in reserve for when the crypto markets recovered.)

In November 2019 Viderium persuaded most of its investors to agree to defer their interest to the end of the term.

In December 2019 / January 2020 Viderium attempted to raise funds on the cryptocurrency markets to resurrect its business model. This failed, in part due to the pandemic and lockdown. In March 2020 Archer threw in the towel and consulted an insolvency practitioner about a voluntary liquidation. This led to Viderium’s Security Trustee appointing Administrators.

The £940,000 used to purchase mining equipment has been written off by Archer, who states its value as “nil” on the Statement of Affairs. Most of Viderium’s mining equipment is apparently in a shipping container in Latvia, having been moved there in 2019, and turned off in 2020 after it became clear that they cost more to run than they brought in. Axia, an independent valuation agent hired by the administrators, notes that the mining machines are obsolete, having been superseded by better models. Worse, Archer “has had difficulties in obtaining contact with the shipping company” who are storing said obsolete miners. Axia are investigating.

As for cryptocurrency, Viderium now owns the sum total of… £25. With Bitcoin having rocketed from £5,000 in March 2020 (when Archer first threw in the towel) to £36,000 at time of writing, Viderium’s chronic bad timing seems to have continued to the very end.

What about the insurance?

Viderium heavily marketed its “A rated insurance”, with the words “WITH “A” RATED BOND INDEMNITY INSURANCE” emblazoned on the front cover of its investment literature.

Whether the insurer, Willis Towers Watson, will pay out is very unclear. The insurance was not a guarantee and only covered the event of “any Actual or Alleged act, Error, Misstatement, Misleading Statement, Omission, Neglect or Breach of Duty or loss” . In itself, Viderium running out of money to pay investors doesn’t qualify. The administrators have contacted the insurer and had not received a response at the time of the report.

Ross Archer estimates that the total value of Viderium’s remaining assets is only £62,000, consisting mostly of £35,000 in cash and a £25,000 to an apparently unrelated company, Mir Marketing and Management Limited. That leaves investors facing total losses unless the insurance pays out – which in terms of unregulated minibonds marketed as “insured” would be a first in my experience.

Independent Portfolio Managers facilitated two minibond investments which collapsed back in 2015 and 2016, Secured Energy Bonds and Providence Bonds, losing in the region of £8m each.

Independent Portfolio Managers was found ultimately responsible for the collapse of the unregulated investment scheme – ultimately passing the bill to the wider regulated financial industry and their customers – after the Financial Ombudsman Service found that Independent Portfolio Managers had misled investors through the literature it approved on the schemes’ behalf.

The liquidators have now issued their second progress report.

It transpires that in 2016, IPM sold its minibonds business to a third party, a half-sister company whose majority owner was The Investors Partnership Limited, which also owned IPM. There is no sign that any consideration was paid for this business.

The liquidator’s lawyers contacted the purchaser, asking them what happened to the money. The purchaser cold-shouldered them.

Letters were sent to the purchaser and IPL requesting payment of the outstanding consideration. Weightmans LLP also requested further information from the Company directors regarding the Sale. The parties did not respond substantively.

£10,000 has been raised from a litigation funder to pursue the alleged missing consideration, with any proceeds to be split 50/50 with the liquidators and the funder.

The last bit of news from the report is that the FCA was carrying out an investigation into IPM’s misleading minibond promotions and its directors. The liquidators confirm that the FCA has closed its investigation and will not be taking any further action.

While it may have been responsible for “only” £15m in investor losses, a far cry from the collapse of a London Capital and Finance or even a Blackmore, the tale of Independent Portfolio Managers is significant due to the way it opened a new door for the general public to be put on the hook for unregulated investment schemes.

Both Providence Bonds and Secured Energy Bonds were unregulated investment schemes, with neither company authorised by the FCA. They needed an FCA-authorised firm to legally be allowed to promote their bonds to the public – which was IPM. When both schemes collapsed, the Financial Ombudsman initially refused to consider claims against IPM on the grounds that IPM worked for Providence and SEB, not the investors. The investors took legal advice and persuaded the FOS to reverse its stance.

IPM was inevitably found guilty of producing misleading literature and found liable for investors’ losses. As it had no funds whatsoever to meet those claims, investors’ claims were paid by the Financial Services Compensation Scheme, i.e. the general public via the levies on the regulated financial industry.

And so the precedent was set that as long as you could get an FCA-regulated company involved somewhere, the general public could be held liable for a collapsed investment scheme even if it was otherwise entirely unregulated.

But the FCA has apparently decided that there’s nothing more to be done and no case to answer. So that’s alright then.

The administrators of the collapsed forex Ponzi Hudspiths Limited have released their first full report after being appointed.

Hudspiths launched in 2015 and promised to pay investors 5% per month while paying its introducers 2% per month. There is no evidence that it ever had any means to generate returns of 7% per month (after costs) from its capital (because there’s no such thing), meaning that Hudspiths constituted a Ponzi scheme.

It collapsed in 2018. Investors defeated an attempt by its directors to cover their tracks by putting the company into voluntary liquidation; instead the company was put into compulsory liquidation in 2019 with the aim of having a better chance of finding where the money went.

Contrary to sex shop owner and Hudspiths director’s Karl Lubienicki, who claimed to the Daily Mail “There’s no money missing. You can’t hide £50million” and that only £7.5 million was outstanding to Hudpsiths creditors, the administrators report that £85 million of claims have been received from 153 creditors. In the original Statement of Affairs, there were only 109 creditors with debts totalling £41 million.

Some of the increase to £85 million might result from investors trying to include their imaginary Ponzi returns in their debts, but the number of creditor claims ballooning by 40% seems likely to be a factor as well.

The administrators have taken legal action against the directors (Lubienicki and Lancelot Hudspith) alleging misappropriate of funds.

We also took immediate legal action against the former directors of the company to protect the interest of creditors. The claim relates to monies which appear to have been misappropriated by the former directors and is based on the very little information we have been provided in the books and records of the company.

So how does 40 / 50 / 85 million not disappear?

The directors’ original statement of affairs detailed the following assets:

A £4.4 million investment into ATFK Training Ltd, a shell company which dissolved without filing accounts

A £1.9 million investment into an unspecified company, and £500,000 invested in various entities; however these investments were made in the name of one of the directors and not by the company itself

£580,000 in a trading account; however when the administrators opened the box, it had been cleared out

£59,600 of cash in the bank, which has been recovered

Some trivial amounts in machinery, fixtures and fittings

These of course only total £7 million odd even if they were recovered – which of course isn’t going to happen. Where the other tens of millions invested in Hudspiths has been not-hidden is currently unclear.

The administrators of Harewood Associates have released their latest report.

£2.8 million owed by another Kiely-owned company, Lansdown Investment Management, has now been fully repaid.

The administrators are however still expecting only 7p in the pound to be paid to Harewood Associate’s £32 million worth of unsecured creditors.

In further bad news for Harewood investors, those who invested in Special Purpose Vehicles (SPVs) have been told that they will not be considered creditors of the company. While the whole point of setting up an SPV is usually to keep its debts separate from the main company, Harewood investors had previously been given hope of being included in the main administration (if being added to an administration which projects 7p in the pound can be viewed as such a thing). This suggests some sort of corporate guarantee.

The idea was sufficiently strong for the administrators to hire a barrister to look into it, however having done so, they have concluded that the SPV creditors are not creditors of Harewood Associates itself.

FCA-kitemarked offshoot closes its doors via voluntary strikeoff

Harewood owners David and Peter Kiely owned another property firm, Monmouth Regent plc.

In an echo of the Harewood scheme, Monmouth Regent plc was previously offering bonds paying 8% per year on its website.

We are delighted to be able to invite you to participate in Monmouth Regent PLC’s inaugural offers for subscription of 8 percent five-year fixed rate secured loan notes.

Monmouth Regent plc website as at May 2020

In July 2020 Monmouth Regent plc was voluntarily struck off the register, suggesting that its fundraising never actually took place (or you would expect creditors to object). Its website monmouthregent.co.uk has also disappeared.

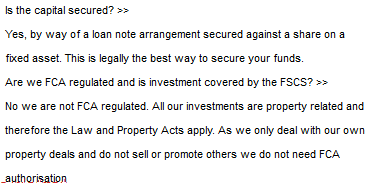

Harewood Associates illegally advertised its bonds directly to the public and claimed that its loan note offering was exempt from UK securities law because Harewood was a property company. As I’ve pointed out before, this is like me soliciting investment from the public in a fast food business and claiming securities law doesn’t apply to me because I’m regulated by the Food Standards Agency.

In contrast, Monmouth Regent plc’s website stated that its offering was approved by an FCA-regulated company, Monmouth Regent Capital Limited, as an appointed representative of Blackheath Capital Management.

The trouble with this claim is that Monmouth Regent Capital only held its appointed rep status from May 2015 to August 2016.

Given that Monmouth Regent plc apparently came and went without taking in any money, or doing anything whatsoever (it filed accounts as a dormant company until its directors struck it off the register) there’s nothing too untoward about it having out-of-date information on a moribund website. However, archive.org shows that Monmouth Regent’s website changed significantly at some point between January 2019 and May 2020, while leaving the false claim to have FCA-authorised sign-off for its ads.

Harewood Associates website in 2016

The shuttering of Monmouth Regent leaves one enduring mystery: why Kiely 1 and Kiely 2 went to the bother of (very briefly) securing FCA authorisation via Blackheath in order to promote their new 5 year bonds, when in their world, property companies are exempt from UK securities legislation.

Despite promoting its investments directly to the public from at least 2013 until its collapse, resulting in at least £32m of investor losses, no enforcement action has been taken against Harewood that is in the public domain.

Liquidators have been appointed to Quinshaw Finance, whose bonds were reviewed here in September 2019.

Quinshaw claimed to offer “secure property high yield bonds” and that “investor protection is our number 1 priority”.

Posts to reviews.co.uk suggest the scheme stopped paying investors around the middle of 2020. Prior to collapsing Quinshaw had over 120 universally positive reviews.

After it collapsed a company calling itself “GDS Consulting” claimed to have been appointed as liquidators and ran a recovery scam on Quinshaw’s victims. It is likely that “GDS Consulting” was in reality someone behind, or within Quinshaw who had access to investors’ details.

The new liquidation is likely to be genuine, based on the filing with Companies House.

Quinshaw was supposedly run by a Paul Hopeton Daye but I have seen no evidence he actually exists. Companies House runs no meaningful checks on those who open UK limited companies.

How do I get my money back from Quinshaw?

Quinshaw’s investor list has already made its way into the hands of recovery scammers, who have contacted investors already knowing about their bonds. Anyone who cold-calls you claiming they can get your money back from Quinshaw or want to buy your bonds is a scammer.

If you were advised to invest in Quinshaw by an FCA-regulated company, you may have recourse to the Financial Ombudsman and Financial Services Compensation Scheme. Unfortunately for investors, as yet I’m not aware that any FCA-regulated companies did promote Quinshaw.

The standard procedure when an unregulated investment goes into administration is to write off the investment and treat any return as a bonus.

Cryptocurrency minibond scheme Viderium has collapsed and gone into administration. MHA MacIntyre Hudson LLP have been appointed as administrators.

Viderium raised £3.9 million (as at December 2018) from bonds paying 9.8% per year for a three year term, claiming “A Rated Indemnity Insurance” on the front page of its brochure.

Whether anything has happened to trigger that insurance is unknown, but I wouldn’t bet on it, given that the insurance covered “any Actual or Alleged act, Error, Misstatement, Misleading Statement, Omission, Neglect or Breach of Duty or loss” and running out of money to pay bondholder returns doesn’t fall under any of those things.

The company continued posting regurgitated content to its Facebook page until August 2020. Its Twitter page has, like its Feefo page, been scrubbed.

In August 2018 Viderium wasted investors’ money attempting to legally intimidate WordPress into removing my review. Viderium made no attempt to complain to me directly, effectively an admission that it knew its complaint was groundless.

Viderium complained that my review “made a number of false statements, unauthorised financial advisory statements, inflammatory and defamatory statements and remarks”. It failed to point out anything in my review that was inaccurate, which simply noted the inherently high risk nature of Viderium’s bonds. It also inaccurately complained that I had republished “confidential and sensitive documents”, when in fact my review was based on Viderium’s own investment material which it freely supplied to the public on request.

Astonishingly, Viderium’s complaint also claimed that their investors could not lose their money.

[Quoting my review] These investments are unregulated corporate loans and if Viderium defaults you risk losing up to 100% of your money.

[Viderium’s complaint] This is false and misleading information not based upon fact. The publisher has provided incorrect information as advice to the general public.

[Quoting my review] If Viderium fails to make sufficient returns from its cryptocurrency mining… there is a risk that they may default on payments of capital and interest to investors.

[Viderium’s complaint] This is false and incorrect information provided deliberately out of context in order to purposefully provide a negative view of the company and the prospect of investment into the company.

Viderium’s collapse illustrates that I was right and that unregulated corporate loan notes are in fact high risk.

In another complaint to Google, Viderium claimed that its “investment bond is regulated by the Financial Conduct Authority”. This was also false. While Viderium’s literature was approved by Bluewater Capital, the investment itself was unregulated.

L: Ross Archer, Viderium CEO. R: Alexander Johnson, Viderium chairman and 95% shareholder.

Three of Viderium’s leading staff members, Alexander Johnson, Ross Archer and Russell Spratley, divided their time between Viderium and a new venture launched in 2019, Whiskey Cask Company, which claims endorsement from rugby legend Chris Robshaw.

Perhaps trying to run two unregulated investment schemes simultaneously caused Johnson, Archer and co to take their eye off the ball at Viderium. As and when more details are published by the administrators, it’ll be covered here.

[Hat tip to readers Tony and Terry who separately flagged up the administration.]

How do I get my money back from Viderium?

Anyone who cold-calls you claiming they can get your money back from Viderium or want to buy your bonds is a scammer.

If you were advised to invest in Viderium by an FCA-regulated company, you may have recourse to the Financial Ombudsman and Financial Services Compensation Scheme. Unfortunately for investors, as yet I’m not aware that any FCA-regulated companies did promote Viderium.

The standard procedure when an unregulated investment goes into administration is to write off the investment and treat any return as a bonus.

The administrators of Carlauren Group have released their latest regular report.

There’s little of interest to report on the realisation of Carlauren’s property assets or hotel business. Nor is there any real further news on the personal bankruptcy of Sean Murray. Murray has had a £40 million asset freezing order imposed (which does not necessarily reflect the value of any assets held by him) but the administrators remain tight-lipped on whether any recoveries are expected from that quarter.

The administrators have managed to sell a private jet, a boat and a car, raising a net amount of £120,000 after accounting for fees and a loan secured on the jet.

While Covid had nothing to do with Carlauren’s collapse, which unravelled in 2019, it has complicated the administration (and not just in the “interminable Zoom meetings” sense).

Carlauren’s jet (tastefully call-signed M-URRY; investors are unlikely to recover the cost of putting a vanity licence plate on a private plane) originally found a buyer for $420k. That fell through when Covid made it impossible to transport the plane to its new owner in Nigeria. The other bidders were mostly interested in breaking the plane up for parts. Eventually the plane was sold for £292,000 but virtually all of this was swallowed up by agents fees of £62k and a secured loan on the aircraft for £217k.

And there you have the administration of a collapsed investment scheme in a nutshell (or a fuselage).

The sale of Carlauren’s boat Adamo – a “luxury motor cruiser” – originally found a bidder for €700k, but they pulled out after an inspection. The pandemic reduced interest in the boat and it was eventually sold for £396k, although port fees and other fees came in at £296k.

It’s not exactly a good time to try to sell a hotel business either.

It remains unclear whether any returns will be paid to Carlauren’s investors. Legal costs currently stand at £956,000 and the administrators own fees’ stand at £2 million to date.

Taking into account the various channels through which people affected can seek compensation, the government will… set up a scheme to assess whether there is a justification for further one-off compensation payments in certain circumstances for some LCF bondholders.

John Glen, Economic Secretary to the Treasury

“Various channels” is a reference to the essentially random basis on which the Government has paid out compensation to LCF investors so far.

Investors who have managed to secure compensation far include people who transferred stocks & shares ISAs to LCF, but not cash ISAs (because there were too many of the latter because of some random nonsense about “regulated investments” being different from “designated investments”). It also includes people who managed to persuade the FSCS that LCF gave them advice (despite not being a financial advice company, not being authorised to provide advice, and employing no financial advisers).

The LCF investors who were told by the Financial Conduct Authority’s call handlers that LCF was legit and FSCS-protected also appear to have a decent chance of being compensated individually by the FCA. Although the Gloster report mentions several cases, this is likely to be only a handful of LCF’s 11,600-odd.

The FSCS has paid out about £50 million so far, representing just over a fifth of the amount lost in LCF.

How much the Treasury’s new scheme will pay out is unclear. Based on what little has been announced so far, it could be anything from zero, if the Treasury decides enough has already been done (although that would make the Treasury’s announcement, and the raising of investor hopes, rather pointless), to full compensation along the lines of the FSCS, perhaps with a cap. More details are expected in the New Year.

If we assume the Treasury’s scheme isn’t pointless, then of the three options available to the Government to justify paying compensation I outlined in an article a year and a half ago, it appears that we are staggering towards a mish-mash of all three. (1. Compensation for bad advice, 2. Compensation on a novel re-interpretation of what the FSCS covers a la Providence Bonds and Secured Energy Bonds, and 3. An ad-hoc, one-off compensation scheme in recognition of regulatory failure.)

Whether compensation is paid by the FSCS, the FCA or the Treasury is of academic interest, as fundamentally the bill lands on the kitchen table of the general public either way. (The category of FSCS levy payers, i.e. anyone who uses financial services, is indistinguishable from the category of taxpayers, although IFAs and others who get billed by the FSCS personally will have a different perspective.)

Whether the Four Horsemen of LCF or the nine other executives sued by LCF’s administrators will be repaying any of the investors’ money is as yet unknown. The lawsuit was launched in September and there’s been little further news since.

Regardless of what legal justifications are found, fundamentally the rationale for bailing out LCF investors is the same old rule: if enough people believe that an investment is risk-free, the Government has to spend everyone else’s money to make it so. See also final salary pension schemes, Barlow Clowes, Equitable Life, IceSave, etc etc.

2021 may be the year that LCF joins that list, depending on how far the Treasury decides to go.

Much of the report is devoted to an update on the running of Signature Living’s hotel properties and the sale of assets, but the expected outcome for retail investors and all other unsecured creditors of the company remains total losses.

Based on current information it is anticipated that there will not be sufficient realisations to enable a dividend to unsecured creditors. […] This position may change dependent on future realisations, quantum of claims from secured and preferential creditors and the costs of the Administration.

Retail investors initially loaned money to other Signature Capital entities, which fall outside the scope of the administration, but with a guarantee provided by Signature Living Hotel, which is the company in administration. The administrators advise retail investors to seek repayment from the Signature entity their contract is with in the first instance.

The administrators reveal that an attempt was made to transfer all the assets of Signature Living Hotel and its subsidiary companies to a new legal entity. This has now been reversed following legal and tax advice. When this was done is not stated, but it must have been between January 2020 (when Signature Living Hotel filed a confirmation statement declaring no change of ownership) and April 2020 (when the company collapsed into administration).

As part of the initial review it was found that the shares in both the Company and all the subsidiary companies had been transferred to a new legal entity that had been set up by the Director to replace the Company as the ultimate parent of the wider Group.

After discussions with the Director, and following legal and tax advice, these transfers were reversed, and the Company has resumed its role as the ultimate shareholder of the majority of the entities in the wider Signature group.

The rationale behind the aborted transfer of the group’s assets is not revealed by the administrators.

When totting up Signature Living Hotel’s unsecured creditors, the administrators originally included a £10 million contingency for claims by retail investors on Signature Living Hotel’s corporate guarantee. So far, claims of more than double this (£20 million) have been received from retail investors.

The administrators note that a group of retail investors is in discussions with Signature owner Lawrence Kenwright in an attempt to formulate a restructuring plan. The administrators comment that they have received no details as yet and cannot comment on the viability of any such plan.

Signature continues to secure positive coverage for itself in the trade press despite losing tens of millions worth of investors’ money. A recent article in Boutique Hotelier claimed that the opening of a new hotel in the Signature Group, Rainhill Hall, represented “a bid to transform its fortunes after a difficult year”. Signature owner Lawrence Kenright claims “it’s an exciting time for Signature Living”.

While the article waxes lyrical about Signature’s “Grade-II listed country house following a renovation project that has seen 14 new bedrooms installed, plus a new spa and a handful of ‘fairytale’ treehouses built in its 18 acres of grounds”, it seems unlikely that a hotel in St Helens is going to change the picture for Signature Living’s investors. Rainhill Hall is not subject to the Signature Living Hotel administration.

Despite Signature having promoted its investments directly to investors without FCA authorisation via emails and its website, which claimed that its high-risk unregulated loans represented “a fantastic return in a secure environment”, no action has been taken by the Financial Conduct Authority against the Signature scheme that is in the public domain.

The administrators’ costs currently stand at £446,000 plus £14,000 of expenses.