Legend Lane has filed accounts for Legend Lane Group Limited to November 2019. Its other group company, Legend Lane Limited, has apparently been discarded; May 2020 accounts show it to be an empty shell and the company has applied to be voluntarily struck off the register.

The accounts reveal little, as the company made use of small company exemptions and did not have the accounts audited or include a profit and loss account. The balance sheet went further into the red over the year, with net liabilities rising from £14k to £186k.

£1.6 million of creditors were reported. How much of this represents investors in Legend Lane is uncertain.

Legend Lane co-owners Chris Miller and Greg Heywood have subsequently moved onto a new unregulated investment scheme, World Property Fund, reviewed here last week. In July 2019 Greg Heywood resigned as director of Legend Lane Group Limited and gave up his shares. Chris Miller is now the sole director and significant shareholder.

The FSCS has begun to rule on whether investors in LCF are eligible for compensation. As of August, it had issued 1,295 decisions, equivalent to 11% of the number of LCF investors, and paid out £20 million, equivalent to 8% of the total invested in LCF.

A back-of-the-napkin calculation would suggest that roughly three out of every four claimants are getting compensation, but that could be wildly inaccurate if, for example, the cases reviewed by the FSCS so far involve larger investments than the average.

LCF investors say that in those cases where the FSCS has turned down compensation, it is doing so on the basis of transcripts of phone calls with LCF and its marketing agent Surge that are wildly inaccurate.

FSCS have incomplete evidence resulting in arbitrary decisions. Compensation is being paid to savers who had no contact other than the website. Transcripts of calls from FSCS say: “I’ve spoken to God, ISiS & Frankie Valli during my investment period and pulled my eyes out”!

FSCS initially had calls “translated” using a computer generated programme which resulted in rubbish being produced. It is this data that they are listening to in order to base decisions. Guesswork – not science.

FSCS stopped issuing Subject Access Request info to investors as it caused more questions than answers. SARs have exposed the data irregularities leading to inconsistent awards of compensation.

@LCFBondholders on Twitter

In a more recent post, @LCFBondholders tweeted:

NO for a saver last week. Yesterday – overturn after challenge. It seems transcripts are used before calls are heard in which ISA = nicer, isis, Alistair, icer, my eyes are, oyster, older, ice is tax free etc

@LCFBondholders on Twitter

When the FSCS announced that it would compensate LCF investors for receiving advice from a company which was not an advisory firm, was not authorised to give financial advice, and employed no qualified financial advisers, it was always going to result in absurdities.

The FSCS’ 44 million pound fudge has so far managed to satisfy virtually nobody (other than the bondholders who draw a winning ticket); neither LCF bondholders as a whole, nor those who pay FSCS levies as part of the cost of running a financial business in the UK.

A judicial review is to be heard over the FSCS’ stance that LCF’s issuing of bonds was not a regulated activity. If successful it would potentially widen the number of LCF investors eligible for compensation to anyone who invested after LCF became regulated.

World Property Fund (a trading name of myriad linked companies including Mercury-Sloane Investments Limited, Tanzy Estates Property Company Ltd, Lennox Vanguard Property Investment Company Limited, Millerheywood Ltd “etc.”) is offering returns of 10% per year, paid quarterly.

The company’s investments are currently being promoted on Facebook.

Who are World Property Fund?

World Property Fund is the latest venture by owners Greg Heywood and Chris Miller.

Last time we encountered Heywood and Miller was in 2018, when they were running an investment firm called Legend Lane which initially offered all sorts of colourful investments, which included – at the time of our review – a forex investment paying 24% per year and a “Black Cat” investment paying 30% per year from… well, it was a secret. In a Bond Review comment Chris Miller described the “Black Cat” bond as “an opportunity to invest in the creditability of our brand and nothing more”.

Legend Lane’s website (legendlane.co.uk) has since been shuttered. Legend Lane ceased offering bonds in 2019 after becoming tangled up in the Hudspiths Ponzi scheme; Legend Lane invested investor monies in a company called PCIA which in turn invested in Hudspith’s Dubai office. PCIA Limited is currently in liquidation. The current status of any investments in Legend Lane is unclear.

Both Greg Heywood and Chris Miller were previously directors of The Step Properties Holdings plc, which ceased operating in 2008 and was dissolved in 2010. A related company owned by Heywood, Heywood Property Investments, collapsed as a consequence owing £3.6 million to HSBC Bank. Only £1.27 million was recovered from that company.

WPF’s website makes a big deal of Heywood and Miller’s trading history but bizarrely makes no mention of their most recent venture.

Their website claims Heywood and Miller built the “largest mid-cap corporation in the UK” (which is like claiming to be the UK’s tallest medium-sized man) and provides a link to audited accounts for the Heywood Group from 2006. How this ancient history is relevant to WPF is unclear.

How safe is the investment?

World Property Fund claims in its brochure to offer “Exceptional security”.

In reality, as with any loan to an unregulated individual company, World Property Fund is an inherently high risk investment with a risk of up to 100% loss.

Secured lending is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

This is not in any sense to imply that the same will happen to investors in World Property Fund, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not WPF) to confirm that in the event of a default, the assets of WPF swould be valuable and liquid enough to compensate all investors. Investors should not simply rely on what WPF tells them about their assets.

World Property Fund describes itself as a “property hedge fund”. Running a hedge fund in the UK requires authorisation from the FCA. World Property Fund has no authorisation from the FCA to run a hedge fund or any other kind of collective investment scheme.

Should I invest in World Property Fund?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted startup company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment paying up to 10% per year is inherently extremely high risk. As an individual, illiquid security with a risk of total and permanent loss, lending money to World Property Fund is much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “secure” investment, you should not invest in unregulated loans with an inherent risk of 100% loss.

A joint announcement by the FCA, FOS and FSCS has confirmed that Dolphin Trust (which recently renamed itself to Generic, I mean German Property Group) has entered preliminary bankruptcy proceedings in Germany.

The F-pack encourages investors who invested in Dolphin via an FCA-regulated SIPP or financial adviser to make formal complaints.

Dolphin Trust bonds were extensively flogged to UK investors via a cast of dubious characters including unregulated introducers and pension liberation fraud schemes such as London Quantum. Dolphin Trust paid out up to 20% of investor funds as commission, according to the BBC.

The unregulated investments were also sold to investors in Ireland and South Korea, where the scandal claimed the head of a prominent bank CEO.

How do I get my money back from Dolphin Trust / German Property Group?

As the FCA has indicated, if you were advised to invest in Dolphin by an FCA-regulated company, or invested via an FCA-regulated pension provider, you may be able to recover your money by making a formal complaint to them.

If the company refuses to provide compensation, the complaint can be taken to the Financial Ombudsman, which can order compensation up to a defined limit. If the company is unable to pay, you would be covered by the Financial Services Compensation Scheme up to £85,000 per person.

Investors should avoid Claims Management Companies (CMCs) as they are unnecessary, often have a lower success rate than direct complaints, and charge eye-watering fees. The FOS and FSCS process is slow but straightforward.

Otherwise the standard procedure is to write off the investment and treat any recovery as a bonus.

If anyone contacts you claiming they can get your money back from Dolphin / GPG (other than via the above channels), it is a scam.

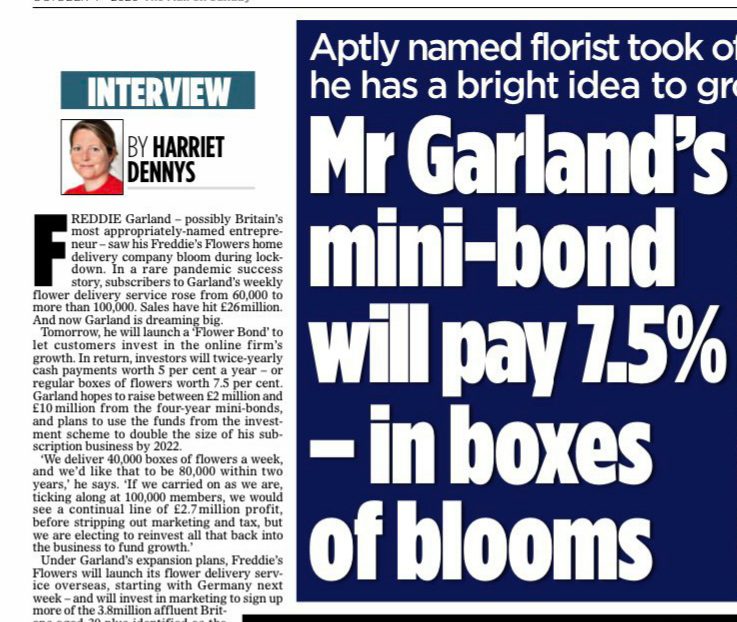

In an annus horribilis like 2020, we all like to hark back to simpler and happier times.

Perhaps it’s in that spirit that the Daily Mail is pretending it’s still 2012, a simpler time when the Olympics was on, the world had almost emerged from the wreckage of the credit crisis, and charming little companies were raising funds in an innovative investment called minibonds.

Let’s be clear – there is nothing illegal or arguably even misleading about the Daily Mail’s interview. Although by highlighting the investment return in its headline and opening paragraphs, it comes as close to an inducement to invest as is feasibly possible, without actually qualifying as a financial promotion.

It is however spectacularly ill-timed as the damage caused by unregulated minibonds from London Capital & Finance to Blackmore Bond to MJS Capital continues to mount. No risk warnings were included in the original print article pictured, although there is a big box about the risks of minibonds in the current online version.

Reaction to the Mail’s intervitorial was near universally negative, and probably not what FF were hoping for.

This is no longer the innocent era when novelty minibonds were a regular feature of Saturday newspapers.

Novelty minibonds were targeted at people willing to commit a few thousand pounds of their capital to signal their brand loyalty, and receive interest paid in anything from chocolate to “craft” beer to burritos to annual colonic irrigation (one of those I may have made up).

Like BrewDog and Chilango, Freddie Garland’s “Flower Bonds” are unlikely to be reviewed here because a) the company hasn’t tried to conceal the risks or tout them as an alternative to bank accounts, b) no-one is likely to invest their inheritance or pension lump sum in a florist. (If they do, I can’t help them.)

Nonetheless, novelty minibonds exist at the fringes of much darker waters labelled “Here Be Krakens”. Once it has been established that you can flog high-risk unregulated investments to the public because, hey man, it’s only flowers, what’s the big deal, the minibonds promising ethical investment and sure-fire returns follow in their wake.

The minibond is facilitated by Bluewater Capital, a name which may be familiar to Bond Review readers as it also worked on fundraising by Viderium, Solidus, Bentley Global and Godwin Capital.

Should I invest in Freddie’s Flowers?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

If you’re happy to risk 100% loss of your money to be paid in flowers for four years then why not, knock yourself out.

The offered return of 5% for monetary returns is a very low percentage for investing in a tiny startup company, with no EIS or VCT reliefs available, and potentially insulting given the company has been tipped as a possible billion-pound startup by PwC. If that happens, the equity investors will see a spectacular increase to the value of their shares, while the bond investors who funded it get a comparably lousy 5%. And it comes with the same risk of 100% loss.

Case To Answer offers an unregulated investment in litigation “invoice financing” paying interest of 12% per year for an investment of 12 months.

Unregulated third-party introducers promoting Case To Answer’s investment claim it represents an opportunity to invest in “one of the most secure investment sectors in the UK” and “low-level risks”.

Case To Answer investors loan money to Case To Answer, who then use it to source leads to provide to solicitors looking for clients. Case To Answer then invoice the solicitor who buys the lead, who becomes the creditor of the investor.

Who are Case to Answer?

Case To Answer was incorporated in October 2018 and is wholly owned by managing director Francisco Xavier (aka Javier) Rodriguez-Purcet. Rodriguez-Purcet took over the company in October 2019; for the year before that it was owned by Andrew Neal.

Case To Answer MD Xavier Rodriguez-Purcet

Rodriguez-Purcet was formerly head of marketing at Tandem Law, which received money from the Axiom Legal Financing Fund. Rodriguez-Purcet was cleared by the Solicitors Disciplinary Tribunal of receiving improper payments in 2019, who overturned a ban imposed in March 2018, at a hearing at which he was not present.

As of 2018, Rodriguez-Purcet has suffered from bipolar disorder since the age of 20. The Disciplinary Tribunal’s March 2018 ban was overturned in October 2018 because they declined to postpone the hearing, after Rodriguez-Purcet’s solicitor rang the Tribunal the day of the hearing and asked for a postponement on medical grounds. The Tribunal refused and went ahead with the hearing in his absence. The High Court ruled that they should have adjourned and ordered the March 2018 ruling to be set aside. At the replay in 2019, Rodriguez-Purcet succeeded in overturning his ban.

Another interesting name behind Case To Answer is Lord Razzall, who is a director of C2A’s sister company, Lawthority. Lord Razzall was a non-executive director of MJS Capital, which collapsed in 2018 owing over £40 million to investors in its bonds. Lord Razzall jumped ship from MJS Capital in March 2018, a few months before investor complaints began to surface, and is not accused of any wrongdoing.

How safe is the investment?

Unregulated introducers claim Case To Answer provides an opportunity to invest in “one of the most secure investment sectors in the UK” and “low-level risks”.

Case To Answer itself claims in its literature that its investment offers “numerous security features that give peace of mind”. These features rely heavily Case To Answer deploying investor funds to generating leads which are sold to solicitors, resulting in an SRA-regulated solicitor becoming the creditor.

Nonetheless, like any unregulated investment paying 12% per year, this is an inherently high risk investment with a risk of total loss. In the first instance, investors are handing their money to Case To Answer, and if for whatever reason Case To Answer fails to generate enough leads to sell to solicitors, and cannot make good on the promise to return investor’s money plus 12% after twelve months, investors may lose up to 100% of their money.

If the liability for returning to investor’s money is taken on by a solicitor, loans to solicitors are not “low-level risk” either, regardless of what assurances may be given about the likelihood of their success in winning cases.

It is not enough for the solicitors to win their cases, or failing that claim “After The Event” insurance: to return investors’ money, Case To Answer and/or the participating solicitor have to generate sufficient returns to pay investors their 12% per year, after their own costs.

A particularly eye-catching claim in Case To Answer’s literature is that “Investors are eligible to claim for compensation from the UK legal industry watchdog if the solicitor defaults”.

As far as I can tell this is not the case. The Solicitors Regulation Authority’s compensation scheme is designed to cover those who lose out from fraud or mismanagement committed by a solicitor, or lack of PI Insurance. Trading debts and liabilities – which would seem to cover paying lead generation firms to find clients – are specifically listed as an example of what is not covered.

I have asked the SRA to comment. However, as a rule, compensation schemes usually decline to give assurances over whether something would be covered or not until a claim arises – by which point it is too late for an investor to pull out.

Should I invest in Case To Answer?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any investment in an unlisted micro-cap company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of up to 12% per year is inherently very high risk. As an individual, illiquid security with a risk of total and permanent loss, Case To Answer’s 12 month loans are much higher risk than a mainstream diversified stockmarket fund, let alone cash accounts.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for a “low-level risk” investment, you should not invest in loans to unregulated companies with a risk of 100% loss, or rely on novel interpretations of the SRA compensation rules.

Wellesley has become the latest minibond issuer to default on investors. Income payments were suspended last week and the company announced on Tuesday that it would attempt to persuade investors to approve a Company Voluntary Arrangement.

According to The Times, investors in property-backed minibonds are facing a write-off of 22% or more, while investors in non-property minibonds face total losses.

I’ve been asked more than once why Wellesley was never reviewed here. The answer is that by the time Bond Review was launched in December 2017, the company had mostly cleaned up its act as far as its adverts were concerned, and (unlike the likes of London Capital and Finance) made it pretty clear that investors were investing in loans to a company and capital was at risk. I don’t write a review just to tell investors what the company has already told them.

Historic Wellesley advertising contained a number of familiar tropes that have since been identified as misleading by the regulator.

Wellesley advertising in 2016.

Regardless of the extent to which Wellesley investors can be blamed for investing in an inherently high-risk investment, the collapse of Wellesley is another blow to the concept of advertising high-risk unregulated and pseudo-regulated investment securities directly to ordinary retail investors.

The adinistrators of Asset Life plc, which collapsed in August 2019 owing £8 million to bond investors, have released their latest update.

Unfortunately there’s not much to report as both of the investments that constitute what is left of Asset Life plc have gone dark on the administrators. Prospects for recoveries from either still look bleak.

We have not identified a realisation strategy for the Company’s investments in Aprelskoe Limited and Lori Iron and Steel Limited that would result in a tangible return to the Company’s debenture holders. Aprelskoe’s two remaining UK-based directors resigned on 5 December 2019 and the company has not responded to any communication from the Joint Administrators. A new Moscow-based director, Mr Sergei Bezborodov, was appointed on 6 July 2020.

[…] Lori has not responded to any communication from the Joint Administrators.

Little is disclosed regarding either the “potential alternative avenues for recovery” being explored by the administrators and their lawyers, or in respect of the insurance policy that supposedly covered Series C bondholders.

In the six months to July 2020, £592 was recovered from a residual balance owed by Keystone Law, plus £7 in interest. Time costs incurred by the administrators over the same period amounted to £21,360.

When I reviewed the Imperial Investments Ponzi scheme I questioned whether co-founder Scott Wood actually existed. Unlike co-founder and habitual Red Bull drinker Dan Pugh, who fronts all Imperial’s Facebook videos, Scott Wood kept in the background, with no public image other than a photo of some baby.

Thanks to reader “CG”, I can reveal that Scott Wood does exist and is a convicted cannabis producer.

CG also managed to find a Maidstone local news article which covered Scott Wood’s appearance in magistrates’ court on charges of producing cannabis. On 21 May 2015 Wood was convicted in Maidstone Crown Court of one charge of producing cannabis, one charge of supplying cannabis and one charge of abstracting electricity.

He was sentenced to a 12-month community order, supervision and mandatory drug rehab. Wood now resides in Malaysia.

Imperial Investments co-founder Scott Wood

A photo posted by Wood at a poker event in Malaysia in January 2020, wearing a hoodie with the Adidas logo reimagined as a cannabis leaf, suggests that the mandatory rehab failed to diminish his fondness for waccy baccy.

Other photos posted by Wood show off a gaudily-painted Audi, and a study full of trainers, a Louis Vuitton bag, and yet more cannabis-based merchandise.

Clockwise from top right: Simon Hume-Kendall, Andy Thomson, Spencer Golding and Elten Barker.

The Four Horsemen Of LCF, the four directors of London Capital and Finance or connected companies to whom LCF on-lent money, who were arrested by the Serious Fraud Office and shortly thereafter released without any charge: Simon-Hume Kendall, CEO Andy Thomson, Elten Barker and Spencer Golding.

Hume-Kendall’s wife Helen.

Paul Careless, CEO of Surge Group which received a total of £60 million in commission for promoting London Capital & Finance.

Former Tory Energy Minister Charles Hendry, who is one of five defendants accused of not doing enough to identify the fraud while serving on the board of LCF-linked companies.

The other six defendants have not been named by the FT.

The lawsuit alleges that LCF’s purpose was to defaud bondholders. According to the lawsuit,

nearly 60 per cent of all of the investors’ cash — about £136m — was channelled to its executives either directly or via loans to companies they controlled or were connected to.

Add the £60m paid to Surge, and you only have at most £1 in every £5 invested by investors going into assets which might pay them a return, according to the administrators.

Although there is not a long history in the UK of the perpetrators of collapsed unregulated investment schemes having to give the money back, one wonders how many directors of unregulated investment schemes that have recently collapsed, or are in the process of collapsing, might be sleeping a little less easy in their beds.

It remains to be seen, probably over the next few years at a minimum, a) whether the administrators are successful in making the allegations stick against the defendants (who universally either vigorously denied wrongdoing or did not make any comment) and b) whether, if so, they can recover any assets.