Acorn Property Bonds (a trading name of RST Group Holdings Limited) offers unregulated bonds paying up to 12% per year as follows:

- 8.5% per year for a 3 year investment with income paid out

- 10% per year for a 3 year investment with interest paid at the end of the term

- 10.5% per year for a 5 year investment with income paid out

- 12% per year for a 5 year investment with interest paid at the end of the term

Note that the above interest rates are simple interest for the rolled-up bonds. On a compound interest basis the 3 year roll-up bond returns 9.1%pa and the 5 year bond returns 9.9%pa.

And yes, this means that the 5-year “capital growth” bond pays you a lower rate of return than the 5-year “quarterly return” bond despite being higher risk. It is a lower rate of return, despite the higher headline rate, because you can reinvest the income you receive from the “quarterly income” bond. This is why compound interest is universally used to compare two investments rather than simple interest.

The “capital growth” bond is higher risk because if we imagine (purely hypothetically) that Acorn defaults after three years, 5 year quarterly return investors will at least have 31.5% of their stake safely in their pocket, while 5 year “capital growth” investors will be contemplating total loss.

Who are Acorn Property Group?

The bonds are issued by RST South West Investments Limited with a “Corporate Guarantee” from RST Group Holdings Limited.

RST South West Investments Limited was incorporated in April 2019. It is yet to file its first accounts (which thanks to Covid are not due until April 2021).

RST Group Holdings Limited was incorporated in April 2017. Its last accounts to September 2018 showed net assets of £24.5 million. (Clearly it wasn’t guaranteeing a £10 million bond issue at the time as its total creditors were only about £790k. Its assets consisted entirely of money loaned to other companies in the group.)

RST Group Holdings Limited’s parent company, RST Residential Investments Limited, is considerably larger (though still a micro-cap company with £13k in net assets according to its September 2018 accounts). Note however that it’s the companies issuing and backing the bonds that we’re interested in here. That does not include RST Residential Investments Limited as far as I can see.

Acorn fails to disclose who ultimately control the business. RST Group Holdings Limited is owned by RST Residential Investments Limited (incorporated 2008), which stated to Companies House in 2016 that there is no registrable entity who controls the business. An annual return that year stated that RST Residential Investments Limited was owned by RST Highgate Investment Trust.

There’s no UK company by that name and a search for RST Highgate Investment Trust on opencorporates.com and the global LEI database turned up nothing.

While the directors of Acorn Property Group may be known, on whose behalf they run the company is not. All that is disclosed publicly is that it’s something called RST Highgate Investment Trust. As to what that is, whose benefit it’s run for and where it’s even located, I’ve drawn a blank.

How safe is the investment?

In an advertorial posted on Business Cornwall, Acorn claims that they offer “another way” compared to the “gamble” of buy-to-let and the “homework” required for regulated property funds.

Buy-to-let can be a gamble while fewer tax breaks, strict health and safety and environmental rules, maintenance and rogue tenants can make managing a buy-to-let complicated – not to mention time consuming. As for real estate investment trusts (REITs), well, you’ll need to do your homework to find the right fund for you.

Of course – there is another way.

In reality, as with any loan to an unregulated individual company, Acorn Property Bonds are an inherently high risk investment with a risk of up to 100% loss.

Acorn’s implication that unregulated loans with a risk of up to 100% loss are not “a gamble” and do not require “homework” is nonsense. Loans to unlisted, unregulated companies require if anything more homework than regulated REITS.

Secured lending is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

This is not in any sense to imply that the same will happen to investors in Acorn Property Bonds, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not Acorn) to confirm that in the event of a default, the assets of Acorn swould be valuable and liquid enough to compensate all investors. Investors should not simply rely on what Acorn tells them about their assets.

Acorn itself says in its own brochure “SPVs (Special Purpose Vehicles) are legal entities set up for a specific purpose to isolate risk. They are designed to prevent adverse risk being transferred to or from the owners of the SPV.”

What Acorn are referring to here is that setting up new companies to issue the bonds, which then lend to special purpose vehicles, means that if those SPVs fail, and the company issuing the bond fails in turn, investors will not have any claim on the assets of Acorn’s owners outside those entities. It is not the investors being isolated from risk by setting up SPVs but Acorn’s owners.

No matter how much time Acorn spend in their literature banging on about the successful history of the wider development business, it’s of limited relevance to investors if that wider business has no liability to repay their loans. This is the kind of issue investors need to be very aware of in their due diligence.

Should I invest in Acorn?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted startup company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment paying up to 12% per year is inherently extremely high risk. As an individual, illiquid security with a risk of total and permanent loss, lending money to Acorn is much higher risk than a mainstream diversified stockmarket fund (including REITS).

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

- Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “secure” investment, you should not invest in unregulated loans with an inherent risk of 100% loss.

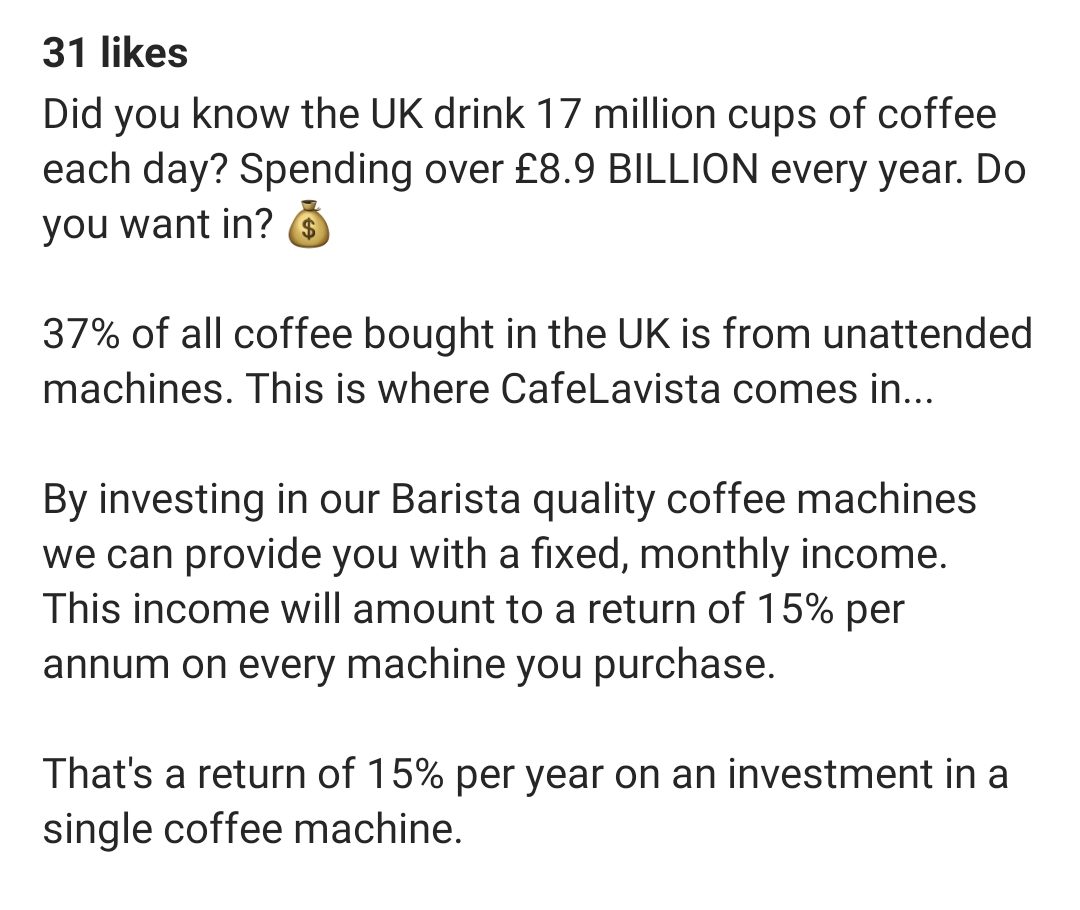

Cafelavista Limited is run by founder Antony Spear.

Cafelavista Limited is run by founder Antony Spear. Cafelavista solicits investment directly from investors via Facebook and Instagram adverts.

Cafelavista solicits investment directly from investors via Facebook and Instagram adverts.