Link: All our Store First and Park First articles

Group First, the parent company of the Store First and Park First investment opportunities, has recently filed its accounts for the year ending June 2018, as have its subsidiaries.

Last year Group First posted a net loss of £43.9m and net liabilities of £32.4m. By far the most significant contributor to its £32.4m worth of red ink was a £62 million provision for making repayments to investors in Park First.

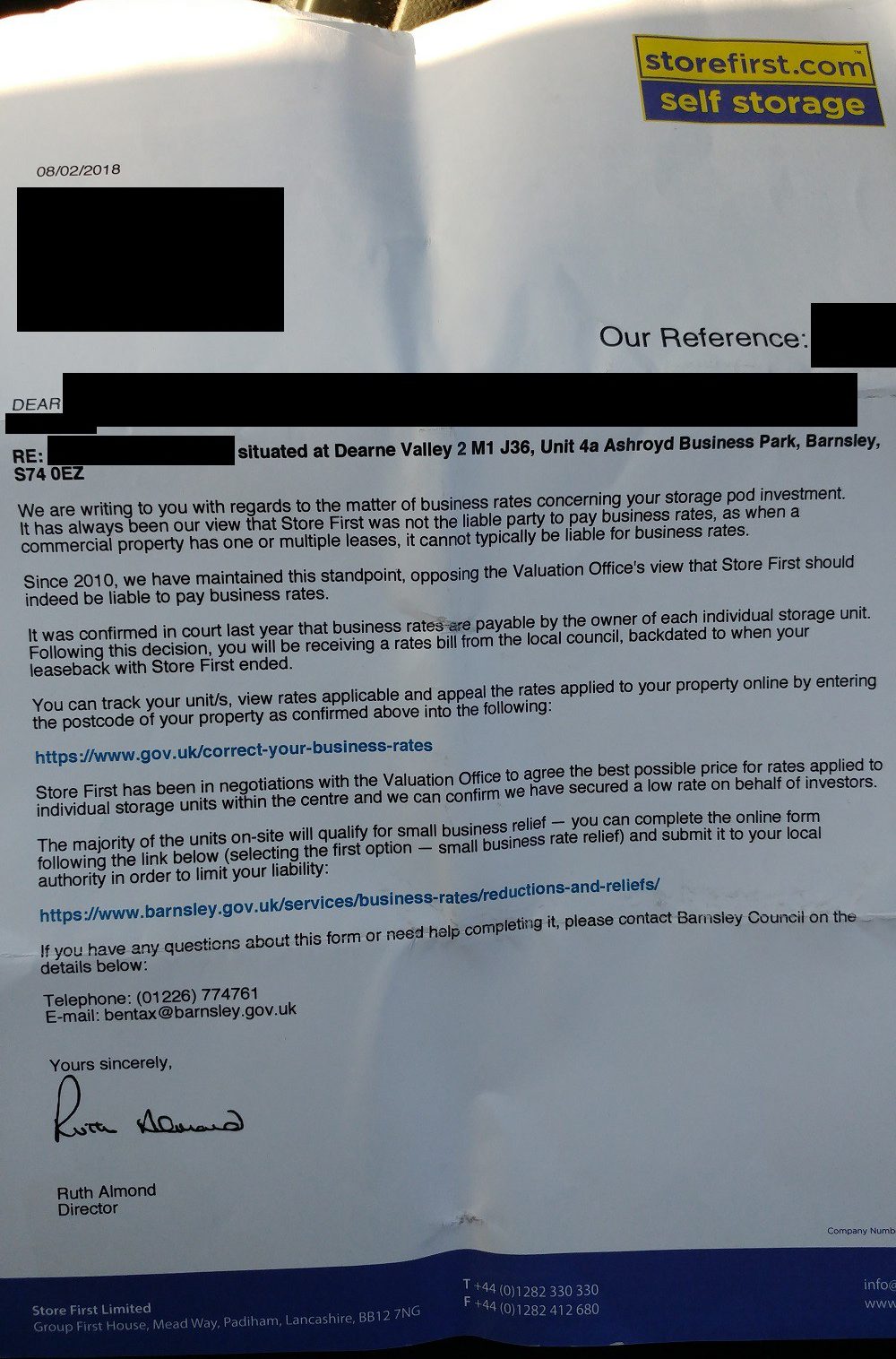

Park First in its original form, which offered investors a “guaranteed yield” of 8% in the first two years, rising to “projected yields” of 10% and 12% in the following four years, was deemed to be an illegal unauthorised collective investment scheme by the FCA in December 2017.

Investors who had already handed over money were given two options: switch to a new “lifetime leaseback” scheme in which they would receive only 2% a year plus variable dividends, or hand back their parking space and get their money back, minus any yield already received.

The provision for repaying Park First investors has now increased from £62 million to £111 million.

Despite this, Group First’s net liabilities has remained almost unchanged, increasing by only £11,475 and remaining £32.4 million.

Amongst many minor shifts in Group First’s various other assets and liabilities, there are two increases in assets which stand out, to balance the £49 million increase in the Park First provision. The first is £27.3 million which has appeared on the balance sheet (nil in 2017). The second is a £30.6 million increase in “Investment properties”.

Goodwill

The £27.3 million of new goodwill represents, according to the accounts,

the excess of the cost of acquisition of a business over the fair value of net assets acquired. It is initially recognised as an asset at cost and is subsequently measured at cost less accumulated amortisation and accumulated impairment losses. Goodwill is considered to have a finite useful life and is amortised on a systematic basis over its expected life, which is 10 years.

Translation for non-accountants: when you buy a business, you put the sum of its parts (its buildings, machinery, etc) on the balance sheet in the usual places, and the rest of the price you paid to buy the business (because businesses are usually worth more than the sum of their parts) goes down as “Goodwill”.

So which businesses has Group First acquired? This can be found by looking at the list of subsidiaries and comparing with the same list from last year. The following subsidiaries have been acquired since the 2017 accounts were filed:

- Store First St Helens Limited

- Harley Scott Holdings Limited

- Store First Midlands Limited

- Park First Glasgow Limited

- Store First Blackburn Limited

Three other subsidiaries, Park First Glasgow Rentals Limited, Park First Gatwick Rentals Limited, and Park First Freeholds Limited, were incorporated directly under Group First Global’s ownership rather than acquired.

The five acquired businesses reported net liabilities of £30.3 million in their June 2018 accounts. Due to their small size they did not file profit and loss accounts. £19.3 million of this deficit comes from Park First Glasgow’s share of the provision for repaying Park First investors. The Goodwill line essentially balances out bringing these liabilities under the Group First Global Limited umbrella.

Harley Scott Holdings was a business run by Toby Whittaker before the advent of Store First and Group First.

In 2011 a subsidiary of Harley Scott Holdings (which was formerly named Dylan Harvey Land Investments) was investigated by the FSA (the predecessor of the FCA) over concerns it may have been operating a collective investment scheme. This investigation appears to have come to nothing.

Another Dylan Harvey business, Dylan Harvey Residential, collapsed in 2009 after taking around £6.5 million in deposits from investors in off-plan property.

Some of Group First’s subsidiaries were previously Harley Scott subsidiaries, and have been repurposed as Store First or Park First subsidiaries even before the 2017 takeover. For example, Store First Midlands Limited was Harley Scott Commercial Limited until 2014, and prior to that Dylan Harvey Commercial Limited until 2010. Park First Glasgow was previously Harley Scott Residential Limited.

Investment properties

Group First Global’s “Investment properties” line increased from £13.4m in June 2017 to £44.1 million in 2018, according to the group balance sheet.

However, note 14, which expands on this line, says that the group’s property at fair value on 1 July 2017 was £31.6 million, not £13.4 million.

Added to this was £1.1 million of property acquired externally, and an £11.3 million uplift to the value of existing property, giving the final value of £44.1 million on the balance sheet.

But the contradiction over the value of the investment property at the start of the year – £13.4 million on 30 June 2017 according to the balance sheet and £31.6 million on 1 July 2017 according to note 14 – calls this into question.

Group First’s net liabilities position will be of crucial interest to Park First investors who opted for the buyback option. Park First gave itself 12 months to repay – after the title for the parking spaces is transferred back to them. Investors have reported that legal delays prevented them from starting the 12 month clock ticking. Nonetheless, with the original illegal collective investment scheme shut down 16 months ago, these deadlines must now be imminent for most investors.

The deadlines are of course irrelevant if Park First’s significant net liabilities indicate it no longer has the money to repay them.

Profits, going concern and dividends

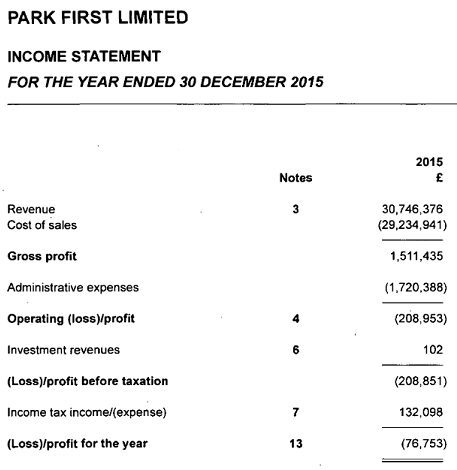

Group First’s turnover has collapsed compared to 2017, with a 91% decrease in turnover from £167 million in 2017 to only £15 million in 2018.

The overall group made a £238k profit, according to the profit and loss account, a marked improvement from a £43.9 million loss in 2017.

However, this profit includes £11.3 million from revaluing the investment properties, over which Group First’s figures seem to contradict each other.

The accounts state that the company is expected to continue as a going concern.

As in 2017, a dividend of £250,000 was paid to Group First Global’s sole director, Toby Whittaker.

Winding up hearing

Store First Limited and four other Store First companies are due to face a winding up hearing on Monday 15 April.

Investors in Store First pods and Park First spaces have been targeted over recent months by a number of scams which offer to pay them outlandish sums for their storage pod or car park space (e.g. around 1.4x what they paid for it). Among the names they have used are GRL and Herschel Escrow.

Investors who contact them will be told they have to pay legal fees or other spurious fees, which they will never see again. (If someone actually wanted to buy their storage pod / parking space, they would deduct their costs from the amount they paid the investor.)