The administrators of collapsed West Ham sponsor Basset and Gold have released their initial report.

Around 1,800 people, described as “everyday investors” by the administrators, invested nearly £36 million into Basset & Gold after being recruited by “internet based marketing and social media campaigns”.

Despite Basset & Gold’s literature claiming that investments were “backed by assets, such as property, corporate debentures and other forms of security in order to PROTECT our investments and your capital”, virtually all of investors’ money was loaned to a payday lender called Uncle Buck.

The opening stanza of the administrators’ potted history reads bizarrely like marketing copy.

The initial target for the business was to provide everyday investors with fixed interest returns, that were easy to understand, using fixed income investments with no additional fees involved.

What this nonsense has to do with Basset & Gold, which gave its investors little chance of understanding that they were investing almost all of their money in a single payday lender, or that “no additional fees” meant 20% of investor monies would be paid to companies controlled by B&G owner Hadar Swersky as commission, is unclear.

The administrators continue:

B&G achieved its targets and provided significant growth year on year.

The only thing that was actually growing was B&G’s debts to investors, from £2m in 2016 to £36 million in 2020. B&G’s (virtually) sole debtor, Uncle Buck, made a loss in all of the four financial years up until it went bust, with its net liaibilities deteriorating from minus £1.4 million in March 2017 to minus £20 million in February 2020.

In April 2019 Basset & Gold stopped marketing its bonds as the FCA started nosing around after the collapse of London Capital & Finance.

Basset & Gold employed an independent firm to carry out a due diligence exercise into Uncle Buck.

They concluded that Uncle Buck would only repay its loans if new money continued to flow in from B&G.

It is believed that the completed independent business review concluded that UB should be able to repay the debt due on time but this was contingent on B&G continuing to fulfil its obligation to UB by virtue of continuing to fund UB’s activities as a HCSTC [payday loans] provider.

In June 2019 B&G were contacted by the FCA who raised concerns about Uncle Buck’s negative balance sheet and bad debt provision. B&G commissioned another independent review, which “portrayed a positive situation with minimal issues identified in respect of UB’s systems and processes”. This failed to mollify the FCA.

Towards the end of 2019 Uncle Buck were supposedly confident of finding £3 million a month worth of lending which would allow it to become profitable. However, in March 2020, “for reasons yet to be explained to the Administrators”, Cypriot shell company River Bloom called in the loan to Uncle Buck, which it was unable to repay, and the jig was up.

Note that as per a diagram in Appendix B, Basset & Gold = River Bloom = River Bloom UK Services = entities controlled by serial entrepreneur Hadar Swersky, which raised money from investors and loaned them to Uncle Buck, a company controlled by a Steven Murray.

While the administrators have managed to recover £2.3 million in cash, they do not expect “any material recoveries for bond holders from the Administration of Uncle Buck”.

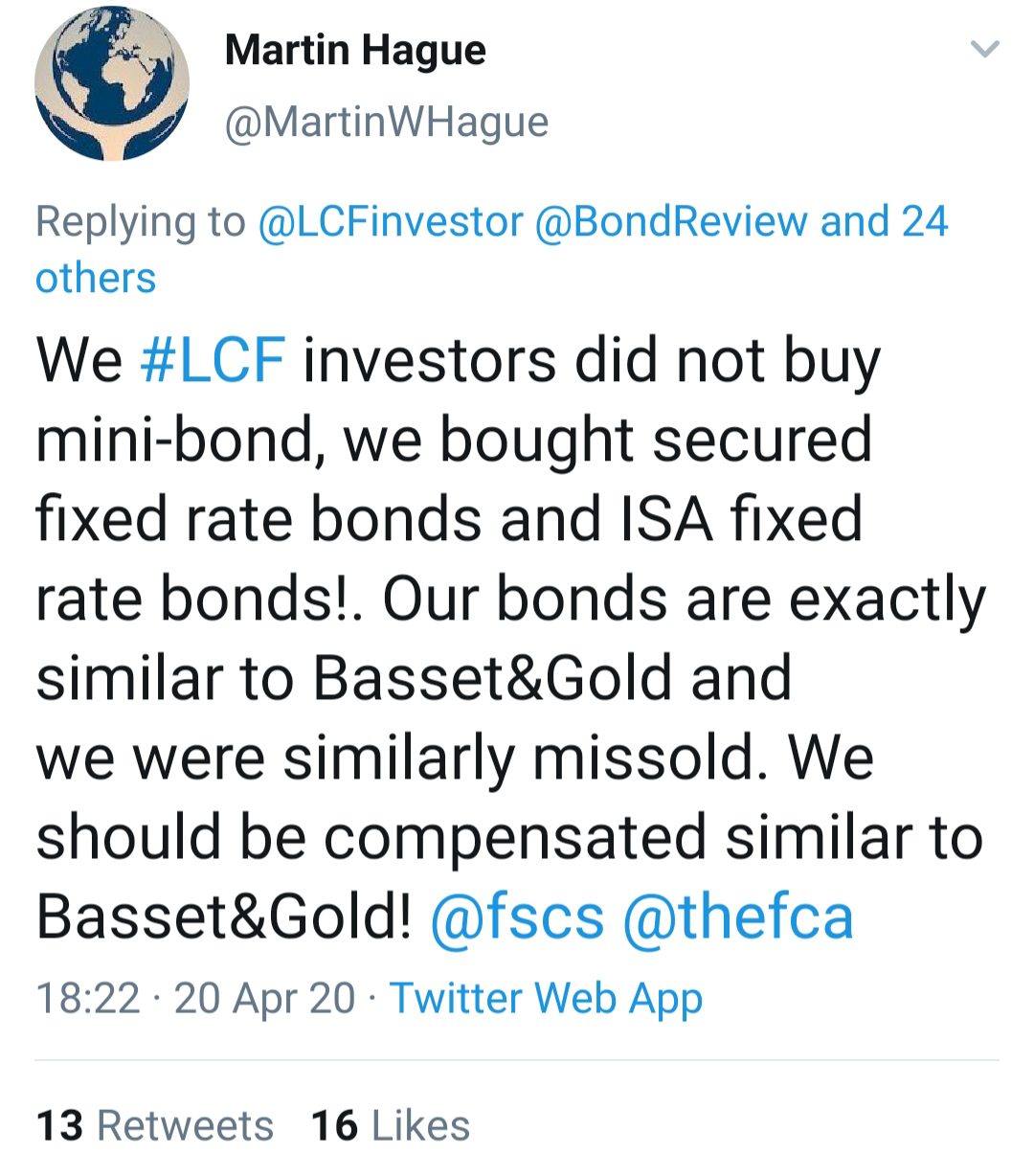

Investors hopes for recovery rest largely on the FSCS. Despite minibonds not being covered by the FSCS, Basset & Gold representatives marketed their bonds specifically on the possibility of FSCS compensation if things went south.

Back in 2018, an investor was told by Basset & Gold’s official Facebook channel:

May I add that we are covered by the FSCS in the unlikely eventually of a mis-selling of one of our products. We to date have a 100% payment track record, and have a 98% recommended service rating from almost 200 of our investors. Lastly all our investments are 100% asset backed. Hope this provides more context.

Given Basset & Gold’s systematic use of misleading literature, which banged on about its irrelevant “100% payment track record” and compared its investments to cash deposits, all identified by the FCA as misleading practice, you’ll struggle to find a Basset & Gold “everyday investor” who won’t claim they were missold.

Still, it’s not all bad – thanks in part to sponsorship money funded by Basset & Gold investors, West Ham FC have successfully kept themselves in the Premier League to entertain us all next season. Which, if claims on the FSCS are successful en masse, will be converted into another load of subsidy from the general public. Up the Sc… I mean Hammers!

{kind=link}