The administrators of Buy2LetCars (comprising Raedex Consortium aka Wheels4Sure, Buy 2 Let Cars and Rent 2 Own Cars) have released their initial report.

The report reveals that of out of every 6 cars invested in by Buy2LetCars investors, 5 didn’t exist.

The total number of known loan agreements is 3,609, relating to 834 investors.. However, the number of vehicles held by the Group is 596, i.e. there are more loans than vehicles.

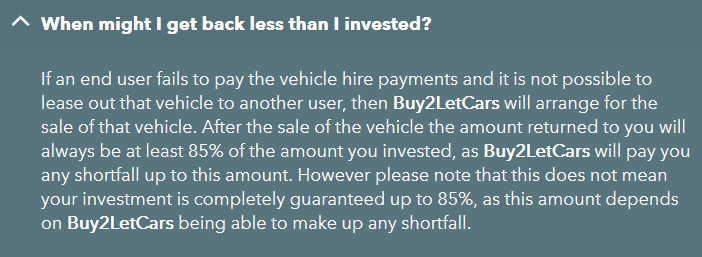

The prospect held out by Buy2LetCars was always that each investor would be investing in an individual car which would be leased out and used to pay their return, and could be sold if the lessee stopped paying.

A funder will simply loan us a lump sum of capital, and with that money we will purchase a brand new car and then lease it out through our sister company Wheels4Sure.

We also ensure your asset is protected by using state of the art tracking and immobilisation technology inside every car.

Buy2LetCars website in January 2021

According to the administrators, it seems that some cars were allocated to more than one investor. Other investors had no car allocated to them at all.

The Joint Administrators are undertaking an exercise to review B2L’s records and allocate each investment to a category based on the signed documentation within the records. This exercise has also revealed that some vehicle registration numbers have been referred to in more than one loan agreement.

Significant amounts of time have been spent on this exercise and it is clear therefore that a large proportion of investors do not have a vehicle allocated to their investment.

Investors who were unlucky enough to hand their money to Buy2LetCars after the FCA had already effectively shut down the scheme by removing their permission to lease new vehicles (although it turns out that this was only a symbolic gesture, as Buy2LetCars wasn’t leasing new vehicles for 5 out of 6 investments anyway) have “queried the treatment of those receipts” (i.e. asked if their money is ringfenced or lumped in with everyone else’s). The administrators will be taking legal advice on this point.

Recovery prospects

A total of £48 million was taken in from Buy2LetCars investors. (A small amount is also owed by B2L to the taxpayer and associated companies.)

£902,000 in cash has been recovered so far. The administrators expect to realise £4.2 million from selling the vehicles and around £400k from the lessees.

The B2L entity to which investors loaned money is in turn owed £31.3 million by Rent 2 Own Cars, also part of the administration. £24m is in turn owed by Raedex to Rent 2 Own Cars. (The administrators’ statements of affairs contain a typo in which R2O is said to be owed £24m by itself. The earlier summary states the correct position.) Prospects of a return from these intercompany debts are currently unclear.

The directors of Buy2LetCars (Reginald Larry-Cole and Scott Martin) owe a total of £804,000 to the group in directors’ loans. The administrators say it is unclear how much will be recovered.

The administrators are also trying to establish who owns a Rolls-Royce that somebody was apparently swanking around in. Even though a business with a couple of million in turnover at most and continual losses doesn’t exactly scream “Rolls Royce lifestyle”.

No figure has yet been put by the administrators on potential recoveries for investors.

Although the investment scheme was unregulated, Raedex was regulated by the FCA, as it had to be in order to lease vehicles to customers. The Financial Services Compensation Scheme is remaining tight-lipped on whether this is enough to dump yet another bill on the general public for the UK regulatory system’s failure to stop unregulated investment schemes being promoted to them. Following the recent bills for London Capital and Finance, Basset & Gold etc etc etc.

As at the date of the 2020 balance sheet, £40.4 million had been lent by investors, on which Buy2LetCars committed to pay 7 – 11%. That required B2LC to generate at least £2.8 million in annual earnings on top of the cost of running the business and bad debts, if it was to meet its obligations.

In that year, Raedex, which was the company responsible for leasing out the vehicles, generated a turnover of just £1.5 million (before any costs had been deducted). But this is hardly a surprise at this point given Buy2LetCars had only 596 cars across 3,609 investors.

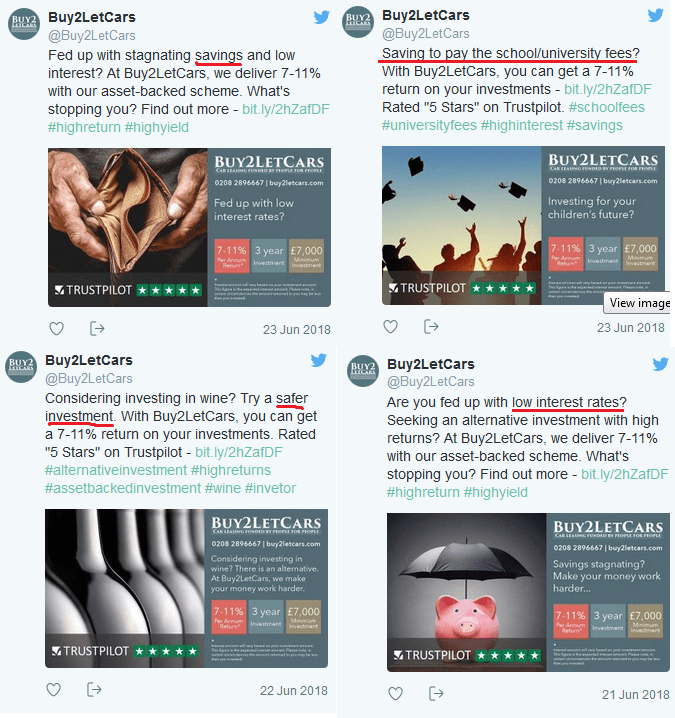

This was naturally not disclosed to investors. Despite running an investment scheme promoted extensively to the public, and claiming “we are fully transparent about our business” on its website pitch to investors, UK company law allowed Buy2LetCars to withhold its profit and loss accounts from Companies House using “small company” exemptions. They have only now been published in the administrators’ report.

The administrators note that a Serious Fraud Office investigation is underway but that this is separate to their own attempts to maximise returns for creditors.