Braxton Knight describe themselves as a wealth management firm offering “investment models to suit all levels”.

Under the “Investment Models” webpage, Braxton Knight offer unregulated securities paying a fixed return of at least 5% per month, although returns are also described as potentially greater, up to 15% per month or even higher. The return depends on how much investors invest, as follows:

Under the “Investment Models” webpage, Braxton Knight offer unregulated securities paying a fixed return of at least 5% per month, although returns are also described as potentially greater, up to 15% per month or even higher. The return depends on how much investors invest, as follows:

- Bronze – Fixed return of 1% per month (£1k – £15k) or 1.5% per month (£15k – £40k) – and “between 3-6% capital growth per month with a capital risk of less than 5%”

- Silver – Fixed return of 2% per month (£40k – £75k) or 2.5% per month (£75k – £150k) and “between 6-9% capital growth per month with a capital risk of less than 5%”

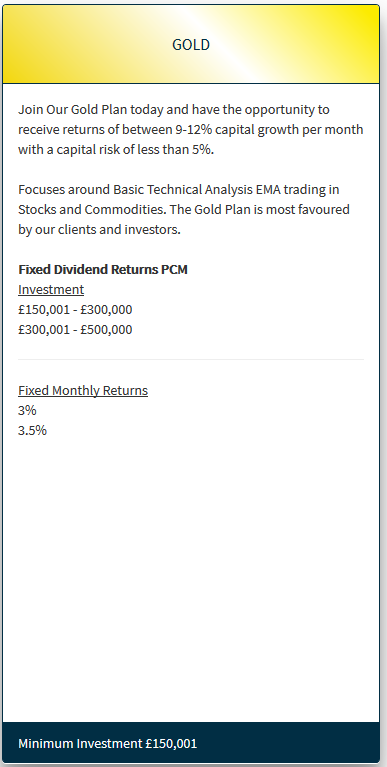

- Gold – Fixed return of 3% per month (£150k – £300k) or 3.5% per month (£300k – £500k) and “between 9-12% capital growth per month with a capital risk of less than 5%”

- Diamond – Fixed return of 4% per month (£500k – £750k) or 4.5% per month (£750k – £1 million) and “between 12-15% capital growth per month with a capital risk of less than 5%”

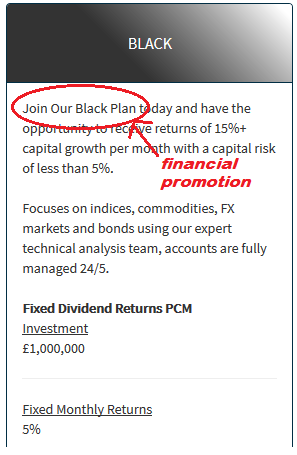

- Black – Fixed return of 5% per month and “15%+ capital growth per month with a capital risk of less than 5%”

Who are Braxton Knight?

There is no information on Braxton Knight’s website as to who is behind the business. Companies House shows that Braxton Knight is wholly owned by Mark McHale, who is also the sole director.

Braxton Knight Ltd was incorporated in 2011, and Mark McHale took ownership in April 2013. Prior to that it appears to have been owned by an accountant dealing in company formations. The last accounts were filed in 31 March 2017 and were “micro-entity” accounts, meaning that the company was small enough to be exempt from audit and providing a profit and loss account. Net assets were £2.9m, of which around £1m was “cash at bank and in hand” and the other £1.9m “tangible assets”.

Braxton Knight’s website, braxtonknight.com, was only registered in February 2017. The registrant’s details are private.

Is Braxton Knight safe?

These are unregulated investments and investors run a very high risk of losing 100% of their money.

Braxton Knight’s description of their “Investment Models” raises red flags at every turn.

Braxton Knight claims that every investment model has “capital risk of less than 5%”, yet the underlying investments are variously described as “Stocks and Commodities” (Gold plan), “indices, commodities, FX markets and bonds” (Diamond/Black) or unspecified “trading” (Silver). These investments all carry risk of losses considerably in excess of 5%.

Furthermore Braxton Knight’s disclaimer at the bottom of every page states “This is a leveraged service which increases the level of risk and return”. Using leverage (i.e. investing with borrowed money) considerably heightens the risk, as the disclaimer says, and makes Braxton Knight’s claim that the maximum loss is 5% even more confusing.

The wildly differing returns offered under the “Bronze/Silver/Gold/Diamond/Black” models make little sense. In general the returns should depend on the underlying assets, not on how much the investor invests.

Investing more money may make different asset classes or funds available to an investor, but this should not be a problem for an investment firm which can pool its clients’ money. More money may also mean more bespoke management and attention from the firm’s investment professionals, but this does not guarantee higher returns – certainly not to the extent that a person investing £1 million would expect returns 5x higher than one investing £15k.

Braxton Knight’s offering of dramatically higher returns to investors who invest higher amounts only makes sense as a way to tempt investors into handing them more of their money.

Long term equity returns have over the last few decades generally been around 8-10% per annum for a diversified portfolio, and the FCA considers 5% per annum to be a reasonable “medium” projected rate of return.

Braxton Knight claim to guarantee returns of 80% a year (a fixed return of 5% a month compounded for a year = 80%) and that returns may potentially be up to 435% a year or more (15% a month compounded = 435%pa).

It is possible to generate a return of 5%-15% in any given month through short-term trading – as it is through online poker or any other form of gambling. However, short term trading is a zero sum game and the expected long term return is nil, minus costs.

Braxton Knight provides no fund factsheets, audited accounts, details of fund custodians or any other proof of being able to consistently generate sufficient returns to pay investors a fixed return of up to 5% a month from returns on trading.

The reality is that the only way to pay fixed returns of 80% a year without exposing investors to losses greater than 5% is to pay existing investors using new investors’ money.

The use of new investors’ money to pay existing investors makes Braxton Knight’s investment service a Ponzi scheme.

The inevitable result of any Ponzi scheme is that eventually the scheme runs out of new investors’ money to pay existing investors, and the scheme collapses. At this point the organisers disappear with any remaining money. A few early investors may see a return. The majority of investors will lose money.

While returns of 5% per month are only promised to investors who invest over £1 million, Braxton Knight describes its Gold plan as its most popular, which pays either 3% or 3.5% per month – i.e. up to 51% per annum.

It is no more possible to consistently generate returns over 51%pa, in order to make fixed payments to investors of 3.5% per month, than it is to generate returns of 80%pa.

Independent advice and financial promotion without authorisation

Braxton Knight’s FAQ refers to “our dedicated financial advice” and states “We offer completely independent advice.”

Offering financial advice in the UK requires authorisation from the Financial Conduct Authority (or authorisation in another European Union member state under “passporting in”).

The website also includes clear inducements to engage in investment activity – e.g. “Join our Gold plan and have the opportunity to receive returns of 15%+”. This constitutes a financial promotion under the Financial Services and Markets Act, which also requires FCA authorisation.

However a search for Braxton Knight on the FCA Register reveals no results. Nor did a search for the owner Mark McHale. Braxton Knight does not claim any regulatory authorisation on their website. It is therefore clear that Braxton Knight are both offering financial advice and financial promotions without FCA authorisation.

Update 02/02/18: On 31/01/18 (the day after this article went to press) the FCA issued a warning about Braxton Knight, confirming “This firm is not authorised by us and is targeting people in the UK. Based upon information we hold, we believe it is carrying on regulated activities which require authorisation.” The firm now appears on the FCA Register as an unauthorised company.

By offering financial advice and financial promotions without authorisation, Braxton Knight is committing criminal offences.

Should I invest with Braxton Knight?

This blog does not provide financial advice. The following are statements of fact based on publicly available information, or near-universally accepted investment principles; they are not personalised recommendations. Investors should consult a regulated independent financial adviser if they are in any doubt.

Braxton Knight’s claim to be able to pay fixed returns of 80% per annum with minimal capital loss bears all the hallmarks of a Ponzi scheme.

Furthermore, the firm is committing criminal offences under the Financial Services and Markets Act by offering financial advice and financial promotions without regulatory authorisation.

Update: On 31/01/18 (after this article went to press) the FCA issued a warning that Braxton Knight is believed to be carrying on regulated activities without authorisation.

Do not invest unless you are prepared to risk 100% losses.

Under the

Under the  Braxton Knight’s FAQ refers to “our dedicated financial advice” and states “We offer completely independent advice.”

Braxton Knight’s FAQ refers to “our dedicated financial advice” and states “We offer completely independent advice.”