In an annus horribilis like 2020, we all like to hark back to simpler and happier times.

Perhaps it’s in that spirit that the Daily Mail is pretending it’s still 2012, a simpler time when the Olympics was on, the world had almost emerged from the wreckage of the credit crisis, and charming little companies were raising funds in an innovative investment called minibonds.

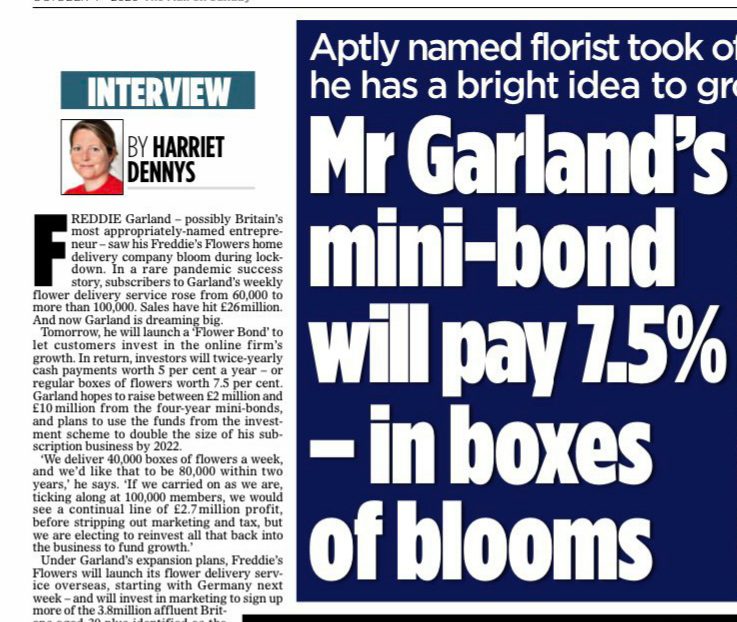

Let’s be clear – there is nothing illegal or arguably even misleading about the Daily Mail’s interview. Although by highlighting the investment return in its headline and opening paragraphs, it comes as close to an inducement to invest as is feasibly possible, without actually qualifying as a financial promotion.

It is however spectacularly ill-timed as the damage caused by unregulated minibonds from London Capital & Finance to Blackmore Bond to MJS Capital continues to mount. No risk warnings were included in the original print article pictured, although there is a big box about the risks of minibonds in the current online version.

Reaction to the Mail’s intervitorial was near universally negative, and probably not what FF were hoping for.

This is no longer the innocent era when novelty minibonds were a regular feature of Saturday newspapers.

Novelty minibonds were targeted at people willing to commit a few thousand pounds of their capital to signal their brand loyalty, and receive interest paid in anything from chocolate to “craft” beer to burritos to annual colonic irrigation (one of those I may have made up).

Like BrewDog and Chilango, Freddie Garland’s “Flower Bonds” are unlikely to be reviewed here because a) the company hasn’t tried to conceal the risks or tout them as an alternative to bank accounts, b) no-one is likely to invest their inheritance or pension lump sum in a florist. (If they do, I can’t help them.)

Nonetheless, novelty minibonds exist at the fringes of much darker waters labelled “Here Be Krakens”. Once it has been established that you can flog high-risk unregulated investments to the public because, hey man, it’s only flowers, what’s the big deal, the minibonds promising ethical investment and sure-fire returns follow in their wake.

The minibond is facilitated by Bluewater Capital, a name which may be familiar to Bond Review readers as it also worked on fundraising by Viderium, Solidus, Bentley Global and Godwin Capital.

Should I invest in Freddie’s Flowers?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

If you’re happy to risk 100% loss of your money to be paid in flowers for four years then why not, knock yourself out.

The offered return of 5% for monetary returns is a very low percentage for investing in a tiny startup company, with no EIS or VCT reliefs available, and potentially insulting given the company has been tipped as a possible billion-pound startup by PwC. If that happens, the equity investors will see a spectacular increase to the value of their shares, while the bond investors who funded it get a comparably lousy 5%. And it comes with the same risk of 100% loss.

1. Like you, I couldn’t believe the breathless article. No mention of the current unregulated bond scandals.

2. One thing, though: it was in The Mail on Sunday (4 October 2020), not Daily Mail. They’re separate newspapers.

1. More on the Freddie’s Flowers mini-bond.

2. Please see “Why the Freddie’s Flowers mini-bond deserves scrutiny”: https://dralexmay.wordpress.com/2021/01/05/why-the-freddies-flowers-mini-bond-deserves-scrutiny/.