Grove Developments offers unregulated corporate bonds paying 10.9% for a 1 year term (rolled up and paid out), 10.3%pa for a 2 year term (income paid twice yearly) or 10.9%pa compounded for a 4 year term (interest rolled up and paid out at the end of 4 years).

Grove’s literature describes the first option as 10.9% per annum but under “Returns to Investors Explained” it shows investors who invest £5,000 as receiving £6,090 on maturity, £10,000 as receiving £12,180, and so on all the way down the table. This of course equates to a 21.8% return over the year.

It can safely be assumed that the table is wrong and that a 10.9% return is being offered, given that the investment literature repeatedly refers to the return as 10.9%, and that there would be no reason to invest in Grove’s other two options if the first one paid double the interest.

The third option is described as 12.8% per annum but this turns out to mean simple interest, with the table of returns – assuming that it’s accurate – showing a total return on investment of £15,120 for a £10,000 investment. As interest is only paid out on maturity, this works out as a 10.89% per annum return on a Compound Annual Growth Rate basis.

It is unclear why investors would want to invest in the third option when they could receive the same annual return with more flexibility by investing in the one year bond and reinvesting at the end of each year.

Status

Open to new investment.

Who are Grove Developments?

Grove Developments Limited (the literature refers to Grove Developments plc, but no such company appears to exist) was incorporated in December 2010 as a property development company.

According to its latest Companies House filings, Grove Developments Limited is 100% owned by AMSL Investments Limited, a Jersey-based offshore company. Grove Developments is part of the Arora Group of companies, a trading name of Arora Holdings Limited.

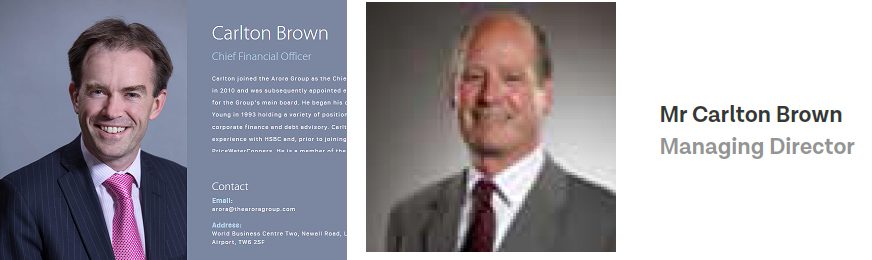

The managing director according to the literature is Carlton Brown. The accompanying photo for Carlton Brown appears to be of a completely different person to the one shown on the Arora Group website.

The other directors according to Companies House are (job titles taken from thearoragroup.com): Surinder Arora (Arora Group founder and chairman), Sinead Hughes (Grove Developments Director) and Athos Yiannis (Arora Group Tax Director / Company Secretary).

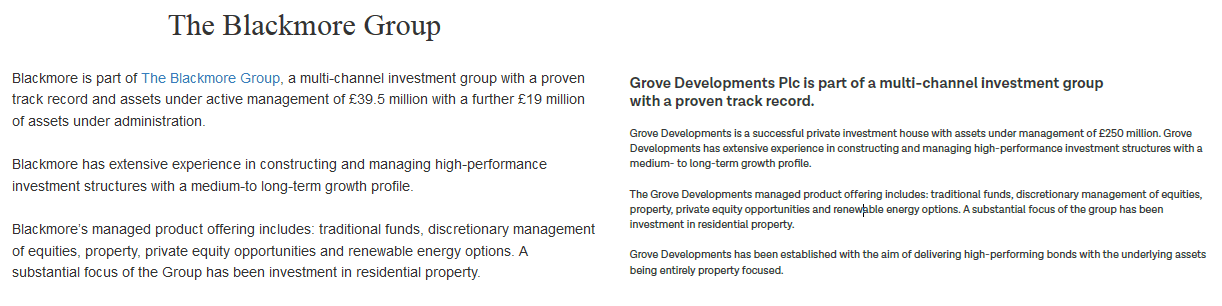

Parts of the literature for this investment appears to have been copy-and-pasted from the website for Blackmore Group, an unrelated company.

The text that Grove Developments has copied from Blackmore and adopted for themselves makes very little sense in this context, in particular “The Grove Developments managed product offering includes: traditional funds, discretionary management of equities, property, prviate equity opportunities and renewable energy options”.

There is no mention of operating investment funds or discretionary management on thearoragroup.com or grove-fund.co.uk, which describe Grove Developments as a property development business. Furthermore such activities would require authorisation from the Financial Conduct Authority. Grove Developments does not appear on the FCA Register or claim any other regulatory authorisation for fund management or discretionary management.

Grove Developments appears therefore to have copy and pasted text from Blackmore Group despite the fact that it is a largely inaccurate description of their business.

How secure is the investment?

These investments are unregulated corporate loans and if Grove Developments defaults you risk losing up to 100% of your money.

The purpose of the loan is to allow Grove Developments to buy properties at under market value and sell them at a profit.

If Grove Developments fails to make sufficient profits from its property developments, or for any other reason Grove Developments has insufficient money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Investors’ money is secured on “all land and property assets owned by Grove Developments”.

Before relying on this security, it is essential that investors undertake professional due diligence to ensure that in the event of a default, these securities are valuable and liquid enough to raise sufficient money to compensate investors, as well as any other creditors that Grove Developments has borrowed money from.

Investors should not assume that because the loans are asset-backed, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed loans have been known to lose 100% of their money when it turned out that the collateral was insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Grove Developments, only illustrating the risk that exists with unregulated corporate loan notes even when they are asset-backed.

Grove Developments claims that “multi-layered security reduces risk to an absolute minimum”. There is very little mention of default risk in its investment literature, even under “How secure is my investment?” in its “FAQ” section.

Under this FAQ there is however the curious statement “Your investment is secured by a legal charge over the assets of the Company and in addition, by the Capital Guarentee [sic] Scheme, which works like an insurance policy, paying out up to £250,000 per investor.” There is no previous mention of this Capital Guarantee scheme in the literature, how it works or where this £250,000 comes from.

There is a strong possibility that this statement is another copy-and-paste, possibly from Asset Life plc (another provider of unregulated corporate bonds), which does feature a £250,000 “capital guarantee” scheme.

Unlike with the Blackmore copy-and-paste, I have not been able to find the original text, so cannot say definitively that this is another copy-and-paste. However, I cannot think of another explanation for why this “Capital Guarantee” scheme does not feature anywhere else in the literature or have any details on how it works.

Should I invest with Grove Developments?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 10.9% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Grove Developments’ bonds are higher risk than a diversified portfolio of mainstream stockmarket funds.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees and any other borrowers are paid.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

- Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for an investment with the “absolute minimum of risk”, you should not invest in unregulated products with a risk of 100% capital loss.

Furthermore, even for high-net-worth and sophisticated investors, the numerous inaccuracies in Grove Developments’ literature, specifically regarding 1) its name 2) the identity of its managing director 3) its business activities 4) the existence or otherwise of a £250,000 “Capital Guarantee” scheme 5) the returns on the “Option One” bond, may be of concern.

Thank you for the making this review available.

Having recently been cold called regarding this investment opportunity it helped me run very fast in the opposite direction!

@Chris: Glad it was of help.

Out of interest, who cold called you?

Chap called Michael Robertson on private number witheld