The administrators of Basset & Gold, the collapsed unregulated investment scheme promoted by West Ham FC, have released their latest update.

Basset & Gold’s funnelled investor funds into payday lender Uncle Buck, via an intermediary shell company, River Bloom UK Services (aka RBUK).

The bad news for investors is that the administrators predict total losses, regardless of how much is recovered from Uncle Buck, due to another River Bloom company, registered in Cyprus, outranking Basset & Gold investors.

Any recoveries in UB are first due to be paid to RBC as they are the senior debt holders, further recoveries after payment in full to RBC are then applied to RBUK and this is where recoveries for Basset & Gold plc bond holders would come from.

The redress procedure will affect the amounts payable to RBC and hence any potential recoveries to RBUK. Based on current information it is unlikely there will be a return, however we will update bond holders in our next report.

The good news for investors is that the Financial Services Compensation Scheme has agreed to bail out one of Basset & Gold’s investors, paving the way for further claims by anyone sold Basset & Gold bonds since 1 March 2018 (including funds which were invested before that date but rolled over afterwards).

We have been advised in recent days that the FSCS has completed the assessment of at least one claim, and found it valid under their rules. Therefore, they will soon be declaring B & G Finance Limited ‘in default’ and commencing the agreement and payment of compensation claims.

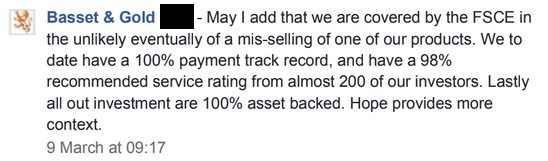

Basset & Gold marketed itself to investors while specifically holding out the possibility that they would be compensated by the FSCS if B&G defaulted.

Mis-selling of Basset & Gold bonds was not an “unlikely eventuality” but part of its business plan. Basset & Gold’s website employed a number of misselling tropes including describing its high-risk loan notes as “cash bonds” and “Pensioner Bonds”, claiming that its structure “protects our investments and your capital” and that its “100% track record” was some sort of assurance rather than completely irrelevant. All these tropes have been identified as misleading by the FCA in the past few years.

As I’ve noted before, this means that B&G attempted the unusual feat of setting the FSCS up as an unwilling guarantor of its unregulated investment scheme in advance. The early signs are that the FSCS is going along with it – unless the successful claims that the administrators refer to turn out to be a small minority.

(Basset & Gold set up a separate limited company to market the bonds which secured regulated status from the FCA in 2018. The investment scheme itself, i.e. the offering of loan notes and the funnelling of that money to Uncle Buck via companies in Cyprus, remained unregulated.)

We can infer that the administrators seem to think that other investors will succeed in their claims, otherwise mentioning the successful claims in their report would achieve nothing accept to give investors false hope. The FCA also gave indications that misselling of B&G bonds had been widespread.

It remains to be seen how many claims of misselling will be accepted by the FSCS, but the general public (who ultimately pay for the FSCS via their bank accounts, loans, pensions and other financial products) should probably brace itself for a very large payout.

The administrators continue to investigate the relationships between the various component parts of the Basset & Gold / River Bloom scheme.

£2.4 million worth of cash has been recovered in addition to an £100k loan made via a P2P platform. Net recoveries currently stand at £1.9 million but this is before the administrators draw their fees, which have been agreed at £1.75 million plus 25% of recoveries.

Can you please explain me what’s going on basic and gold I’m going up the bondholders thank you