The administrators of Harewood Associates have released their latest report.

£2.8 million owed by another Kiely-owned company, Lansdown Investment Management, has now been fully repaid.

The administrators are however still expecting only 7p in the pound to be paid to Harewood Associate’s £32 million worth of unsecured creditors.

In further bad news for Harewood investors, those who invested in Special Purpose Vehicles (SPVs) have been told that they will not be considered creditors of the company. While the whole point of setting up an SPV is usually to keep its debts separate from the main company, Harewood investors had previously been given hope of being included in the main administration (if being added to an administration which projects 7p in the pound can be viewed as such a thing). This suggests some sort of corporate guarantee.

The idea was sufficiently strong for the administrators to hire a barrister to look into it, however having done so, they have concluded that the SPV creditors are not creditors of Harewood Associates itself.

FCA-kitemarked offshoot closes its doors via voluntary strikeoff

Harewood owners David and Peter Kiely owned another property firm, Monmouth Regent plc.

In an echo of the Harewood scheme, Monmouth Regent plc was previously offering bonds paying 8% per year on its website.

We are delighted to be able to invite you to participate in Monmouth Regent PLC’s inaugural offers for subscription of 8 percent five-year fixed rate secured loan notes.

Monmouth Regent plc website as at May 2020

In July 2020 Monmouth Regent plc was voluntarily struck off the register, suggesting that its fundraising never actually took place (or you would expect creditors to object). Its website monmouthregent.co.uk has also disappeared.

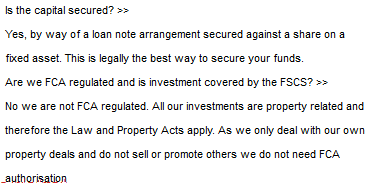

Harewood Associates illegally advertised its bonds directly to the public and claimed that its loan note offering was exempt from UK securities law because Harewood was a property company. As I’ve pointed out before, this is like me soliciting investment from the public in a fast food business and claiming securities law doesn’t apply to me because I’m regulated by the Food Standards Agency.

In contrast, Monmouth Regent plc’s website stated that its offering was approved by an FCA-regulated company, Monmouth Regent Capital Limited, as an appointed representative of Blackheath Capital Management.

The trouble with this claim is that Monmouth Regent Capital only held its appointed rep status from May 2015 to August 2016.

Given that Monmouth Regent plc apparently came and went without taking in any money, or doing anything whatsoever (it filed accounts as a dormant company until its directors struck it off the register) there’s nothing too untoward about it having out-of-date information on a moribund website. However, archive.org shows that Monmouth Regent’s website changed significantly at some point between January 2019 and May 2020, while leaving the false claim to have FCA-authorised sign-off for its ads.

The shuttering of Monmouth Regent leaves one enduring mystery: why Kiely 1 and Kiely 2 went to the bother of (very briefly) securing FCA authorisation via Blackheath in order to promote their new 5 year bonds, when in their world, property companies are exempt from UK securities legislation.

Despite promoting its investments directly to the public from at least 2013 until its collapse, resulting in at least £32m of investor losses, no enforcement action has been taken against Harewood that is in the public domain.