Pardus offers loan notes with a 24 month term which pay interest of 1% per month, with coupons paid quarterly.

At least, that’s what their website says, but Pardus is offering special terms via introducers where that return is doubled to 2% per month, with a 2% initial charge.

As for what this means overall, Pardus’ brochure includes a worked example which calculates that the total returned for a £100,000 investment – if all payments are made successfully – would be £147,040. This is equivalent to an annual compound return of 21.3% per year.

There’s nothing wrong with introducers arranging preferential terms, but doubling the return is an extreme version of this – and anyone getting 1% from Pardus’ bonds who subsequently found out that they could have got double the return for the same amount of risk if they’d responded to a different advert, would be justified in feeling a bit miffed. The rest of this review is based on the above preferential terms which were being offered as at June 2020.

Investors’ money is to be used to invest in arbitrage trading – identifying a mismatch between prices for the same asset on different exchanges, buying assets at the cheaper price and immediately selling them at the higher one.

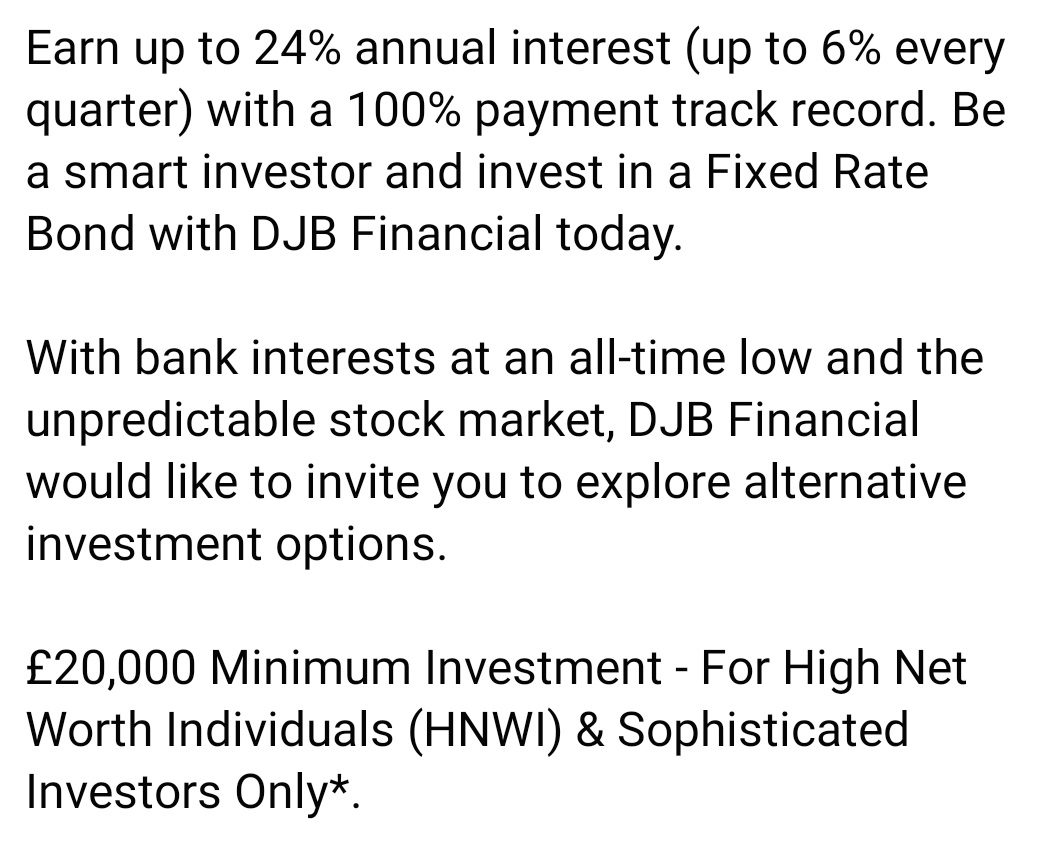

At time of writing Pardus’ loan notes are being promoted by Facebook via unregulated third-party introducers who claim that investors should consider Pardus as an alternative to “bank interests at an all-time low” and the “unpredictable stock market”, going onto claim “Security of the capital invested” as a “Key Feature”. For more on these claims see below.

Who are Pardus?

Pardus is headed and owned by CEO Greg Bryce. Bryce is described in the literature as having “30 years’ experience in banking, broking and the regulatory space”.

This doesn’t tally with Bryce’s own LinkedIn page. While Bryce’s published CV does stretch 32 years (starting from his work as a Booth Manager at Refco in 1989, at age 22), Bryce spent 10 of those years selling bicycles, as CEO of triathlon shop chain Triandrun Ltd. So I make that just over 20 years in banking etc.

A minor point but I’m a stickler for accuracy when it comes to the marketing of investments paying 24% a year.

Both Pardus Fixed Income Bond Company plc and GRMA-Pardus Wealth Limited were incorporated in April 2018. Both are yet to file accounts as an active company.

How safe is the investment?

As described above, Pardus’ bonds are being advertised on Facebook by third parties as an alternative to the “unpredictable stock market” with “Security of the capital invested” as a “Key Feature”.

In reality, as with any loan to an individual company, Pardus is an inherently high risk investment with a risk of up to 100% loss.

Pardus claims that it “will utilise investors capital in connection with contract arbitrage arrangements, therefore the monies are not put at risk”.

However, to return investors’ interest and capital, Pardus has to identify enough arbitrage opportunities to successfully pay interest of up to 24% per year after its costs and any commission paid to introducers.

Arbitrage opportunities are by nature difficult to come by and there is an inherently high risk that it will not succeed.

Pardus’ literature states that “GRMA PARDUS Wealth has guaranteed to indemnify any loss incurred by PARDUS Fixed Income Bond”.

Secured lending is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

This is not in any sense to imply that the same will happen to investors in Pardus, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not Pardus) to confirm that in the event of a default, the assets of Pardus would be valuable and liquid enough to compensate all investors. Investors should not simply rely on what Pardus tells them about their assets.

At the time of GMRA-Pardus Wealth Limited’s last published accounts (April 2019) it was a shell company with £1 in assets. This emphasises the need for full due diligence to establish how much a guarantee by GMRA-Pardus Wealth is worth.

Pardus’ bonds are listed on the Frankfurt Stock Exchange. At time of writing no trading of the bonds is visible on the exchange, meaning the bonds are likely to be illiquid and there is a significant chance that investors would be unable to redeem their investment by selling it to another before maturity.

Should I invest in Pardus?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted startup company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment paying 21% per year (net of the 2% initial charge) is inherently extremely high risk. As an individual, illiquid security with a risk of total and permanent loss, lending money to Pardus is much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

- Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “guaranteed” or “secure” investment, you should not invest in illiquid loans with an inherent risk of 100% loss.