In early May I reviewed Accumulate Capital’s unregulated loan notes, which were touted as an “Asset Assured Accumulator” paying potential returns of 15% per year.

Accumulate Capital is run by an ex-alumni of Signature Capital, Paul Howells, who formerly described himself as a “Partner” at Signature on his LinkedIn page. Its corporate entity was originally incorporated as EQT Capital Limited by Sarah Schofield, a director of two Signature companies. Signature Capital collapsed into administration in April.

Let’s be very clear – the fact that both Accumulate’s once and current owner were ex-Signature alumni does not mean that Accumulate is the same company as Signature.

One thing Accumulate and Signature do share however (apart from ex-Signature staff) is a predilection for pointless legal threats, while withholding information from their own lawyers.

Back in May 2019 Signature threatened me with legal action over various points in my review. Among their complaints were that I’d said they offered returns of up to 16% per year, which their lawyers vehemently denied despite me being in possession of the promotion in question. They also complained that my review hadn’t paid enough attention to the fact that Signature’s investments were backed by a corporate guarantee.

In January 2020 Signature attempted to argue in court, in a vain attempt to dodge honouring its debts, that this corporate guarantee – the same one they’d threatened to sue me over – didn’t actually exist, because the paperwork wasn’t witnessed. This argument was thrown out of court on its arse. Anyway, enough ancient history, let’s get back to Accumulate.

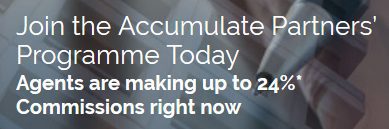

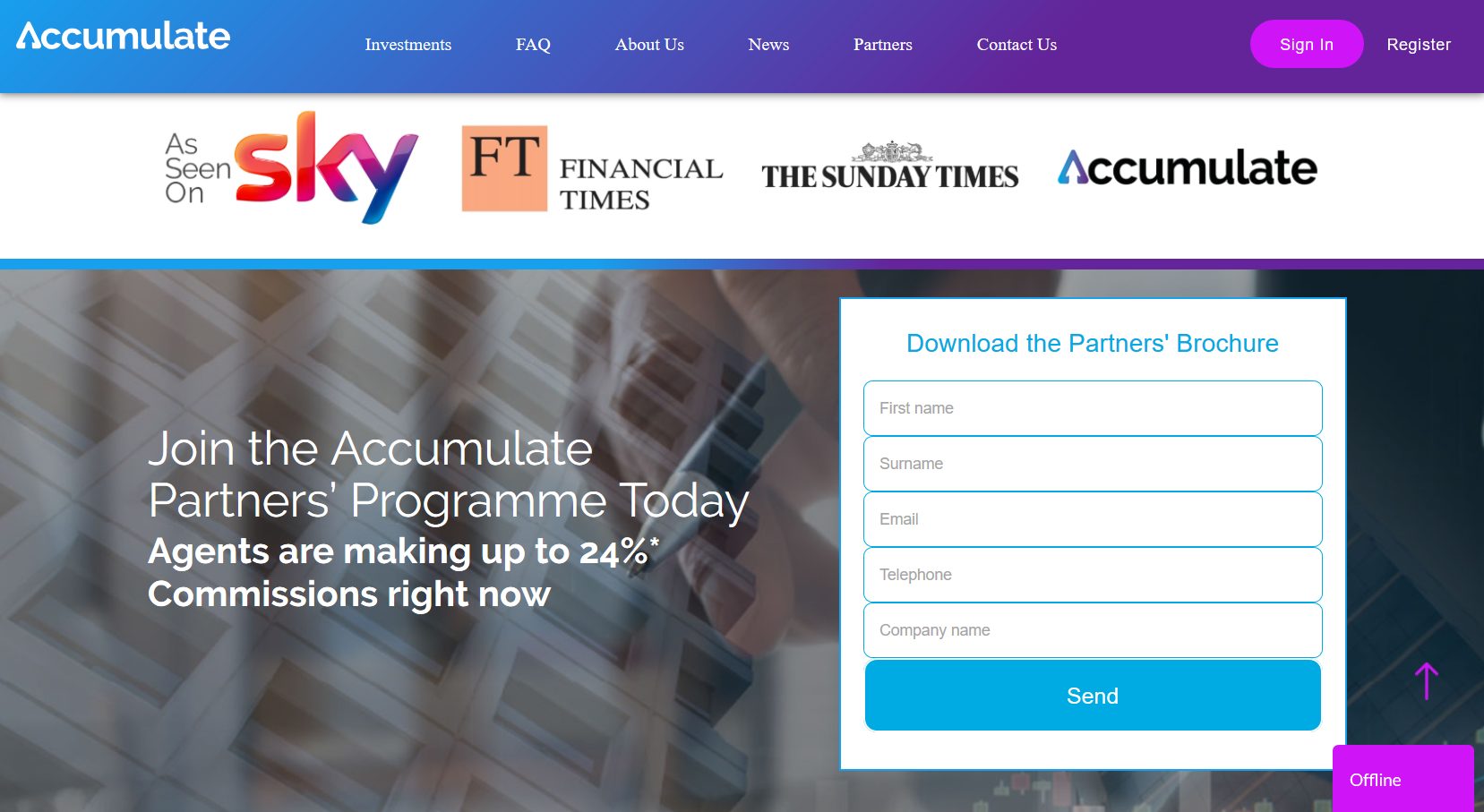

Shortly after my article was published, Accumulate contacted me with various complaints. Some of these related to third-party comments left underneath the article, which have been dealt with as the commenters’ responsibility. Accumulate’s main beef against me personally is that I’d noted a section on their website which promised to pay introducers “up to 24% commissions” .

The fact that Accumulate paid up to 24% commission, according to its website at time of publication of my review, significantly raises the risk of the investment. Assuming it pays out the full 24%, it means it has to generate a 32% return just to get back to the investor’s original capital. That’s before accounting for its own costs, and the returns paid to the investor. (Accumulate’s website touted returns of 15% per year in a testimonial.)

Accumulate’s lawyers claimed “This claim does not feature anywhere on our client’s website and has never been made on its website.” This was false. The original review even included a screenshot of the 24% commission claim, just in case anyone thought I’d decided to start randomly making things up after two and a half years of running Bond Review.

It gets better. According to Accumulate’s lawyers, it was “out of context and misleading” to note that Accumulate advertised commissions of up to 24%, because “a 24% figure was once referenced in a promotional document” [and continuously on Accumulate’s website at the time of the review] “but with an explanation, which you have omitted, that this was three payments of 8% commission.”

As readers will note from the screenshot above, I omitted nothing, as the advertisement to introducers in question didn’t mention anything about the 24% being paid in three instalments.

More importantly, it doesn’t actually matter. Last time I checked my calculator, 8 x 3 = 24.

And if it’s “misleading” to say that 8 x 3 = 24, Accumulate’s website was equally misleading.

Accumulate has since scrubbed the page in question, which now returns a “404 not found” page.

Accumulate then allegedly doubled down on misleading their own lawyers, who told me “Our client has not changed its website or removed any reference to the 24% commission – it was never on its website.” As can be confirmed from the above screenshot of Accumulate’s website as at 16 April, and a comparison with the same page now, this is also false.

Although Accumulate and Signature are entirely different companies, I can’t help being reminded of Signature complaining about me saying they’d offered 16% per year to their investors, when a quick search of their own email server would have confirmed they did.

Similarly, Accumulate’s hapless lawyers could have simply run a “site:” Google search on their clients’ website, instead of wasting investors’ money (lawyers are expensive) claiming that the above webpage never existed.

Accumulate also complained that “Paul Howells has never been a director or partner of Signature Capital.”

I have never claimed that Paul Howells was a director of Signature Capital, but that doesn’t change the fact that he described himself as a Partner on his LinkedIn profile.

He then attempted to scrub his association with Signature from the Internet, but evidence of his time at Signature remained on his profiles with Apollo.io (which scrapes from LinkedIn) and Vimeo long enough to be saved for posterity.

So in summary:

- Paul Howells is a former Partner of Signature, based on his own LinkedIn profile.

- Accumulate openly offered, at the time of my review, up to 24% commission to introducers.

- Both these facts were correct as at the time of my review, despite Accumulate attempting to scrub both from the Internet.

- Accumulate have wasted their investors’ money on lawyers attempting to browbeat me into removing the above facts from my review.

- Which is money they can’t afford to waste given that they offer rates of 15% per year on investors (based on their testimonials at the time of the review) while paying up to 24% commission to their introducers (based on their website at the time of my review).

My review noted that Accumulate’s investments, being unregulated loans to an obscure unlisted company, are inherently high risk with a possibility of 100% loss.

Investors should think long and hard before investing with a company that wastes money on attempting to conceal verifiable facts.

Comments on this article can be submitted via the Contact link at the top of the page.