The P2P platform Money & Co has launched a “Money & Co Portfolio” service, which can be held via an Innovative Finance ISA.

Money & Co is a “pick your own” P2P platform through which investors lend money directly to firms raising money via the platform. With the “Portfolio” service, investors’ money is managed by Bramdean Asset Management who invest in a range of loans offered by the Money & Co platform.

Money & Co Portfolio’s literature advertises “Fixed rate returns of 7% after fees”.

Eagle-eyed readers will have noticed that I briefly warned against a possible clone scam, based on misleading advertising and the use of a newly-registered URL which was different to Money & Co’s usual one (moneyandcoportfolio.com rather moneyandco.com). Money & Co has confirmed that the offer is genuine and not a clone firm scam. My concerns over misleading advertising, however, remain.

Money and Co has retained Vimiera Limited as a tied agent to market the Money & Co Portfolio via the isamoney.co.uk.

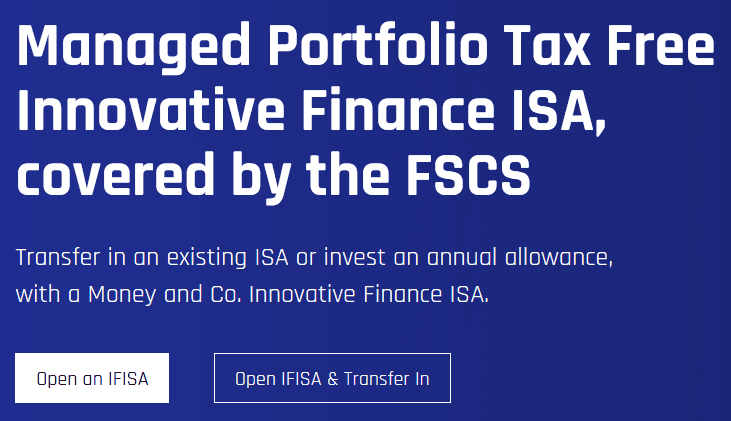

At time of writing, the front page of isamoney.co.uk claims in big letters that the investment is “covered by the FSCS”.

Most retail investors will think of “covered by the FSCS” in the sense it applies to an FSCS-backed deposit, where the FSCS pays up if the bank you lend your money to goes bust.

It is important that investors understand that this is an investment in P2P loans and the FSCS will not pay up if the underlying borrowers default on their loans (in which case you risk losing 100% of the money invested in that particular loan).

The FSCS also does not apply if Bramdean Asset Management makes poor decisions and most of your loans lose money. Poor performance by a portfolio manager does not automatically make them liable. (Otherwise anyone whose investments underperformed would complain and get their money back.)

Vimiera also previously issued Facebook ads to the public which referred to “IFISA offering 7% fixed returns net after fees, asset backed, managed portfolio FSCS protection with flexible draw down”. After I raised my concerns a few weeks ago, the Facebook ads were removed pending a review by by Money & Co’s compliance team. The above isamoney.co.uk promotion however remains visible at time of writing.

Vimiera is not authorised itself to issue financial promotions. It is not explicitly stated on Vimiera’s isamoney.co.uk website which FCA-regulated company has authorised the promotion to be issued to the public.

Who are Money & Co?

Money & Co was founded in 2013 by Nicola Horlick, a well known fund manager. It is a trading name of Denmark Square Limited. Denmark Square Limited does not file full accounts, but its most recent accounts (March 2018) suggest it remains loss-making, with “retained earnings” moving from minus £7.1 million in 2017 to minus £8.6 million in 2018. Due to its small size, the accounts were not audited and did not include a profit and loss account.

Who are Vimiera?

Vimiera Limited, the tied marketing agent behind the isamoney.co.uk website, was set up in June 2018 by Barry Stubley and Lynne Ashton.

Prior to founding Vimiera, Barry Stubley was from February 2013 to April 2014 a director of Premier Advice Club Limited, part of Investaco Asset Management, an unregulated introducer not to be confused with Investec Asset Management.

After leaving Premier Advice Club, Stubley incorporated Contemporary Investors Club Limited, which remained dormant until Stubley dissolved it in September 2018, shortly after launching Vimiera.

Should I invest in the Money and Co Portfolio?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

P2P investment is a legitimate and regulated sector. Personally I don’t think the returns from P2P generally compensate for the risks of lending to very small companies, but this is a personal preference.

Money and Co’s “Loans for Sale” page currently shows a total of 11 different companies seeking investment via Money and Co (albeit some companies are offering multiple loans in different projects). A portfolio of loans to 11 small companies would not be nearly as diversified as a standard corporate bond fund which would typically be invested across dozens or hundreds of companies listed on major stock exchanges.

Before investing investors should ask themselves:

- How would I feel if the majority of my loans defaulted and I lost significant amounts of money?

- Is my portfolio big enough that I could permanently lose a large part of my investment and not worry about it?

- Am I genuinely happy with the risks of P2P lending, or did I come to Money & Co Portfolio because I was attracted by the “covered by the FSCS” statement?

Investors who are happy with the risks associated with P2P and lending to small businesses will need to do their own due diligence.

Investors who are looking for an investment which is “covered by the FSCS” should not invest in P2P loans to small companies which have a risk of significant losses should the borrowers default.

[Comment deleted. -Brev]

Will a Nicola Horlick related entity be subject to a s.166 before the year is out?

“…“retained earnings” moving from minus £7.1 million in 2017 to minus £8.6 million in 2018. Due to its small size, the accounts were not audited and did not include a profit and loss account”

SMALL SIZE?

That is many many times the earnings and even turnover of many small and medium businesses I know and they get checked all the time.

If I were HRMC, I’d have a field day checking them out. Not just because they probably owe taxes, but also endanger savings for the public.

If any two out of of the following three applies: annual turnover under £10.2 million, balance sheet total under £5.1 million, and less than 50 employees, you don’t have to submit audited accounts to Companies House or include a profit and loss account.

“Small” is the official term used by Companies House to describe such companies.

Exercising your right under the “small companies regime” is entirely legitimate and not evidence that you aren’t paying your taxes.

HMRC is not responsible for the regulation of investment schemes.