Milton Park Capital offers unregulated bonds paying 9.5% for one year or 16.8% per year for two years.

Who are Milton Park Capital?

Milton Park Capital is a trading name of FSE Global Solutions Limited.

The “Team” page on the company’s website says it is headed up by Ronald D Rexvale, and claims “Ronald has a long career in investments and the energy sector, he started as a Secretary and later became the Chief Executive of a mutual health insurer before becoming our director in 2012.”

In reality, Ronald Rexvale only became a director of Milton Park / FSE in August 2017. Companies House shows that FSE Global Solutions was originally incorporated in 2012 as Rexvale Services by what appears to be a company formations outfit.

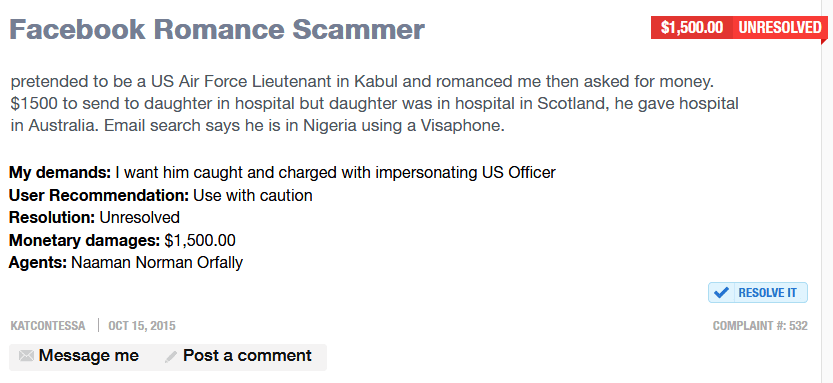

In July 2017 ownership was transferred to a Canadian named Naaman Norman Orfally. Online reports link Naaman Norman Orfally to oil and gas trading scams and Facebook romance scams.

Of course its possible that the former director of FSE Global Solutions is a different and entirely innocent person, but given the unusual name, that would be an Orfally big coincidence.

A month later in August 2017, Orfally resigned as director and the company owners became Ronald Rexvale and Linda Wang in equal shares.

Shortly before Rexvale became director, the company was renamed Apex Corporate Global Limited. In April 2018 it was again renamed to FSE Global Services Limited.

Nominet shows that the miltonparkcapital.co.uk domain was only registered in July 2018.

The claim that Ronald Rexvale was CEO of a health insurer should be easily verifiable, despite Milton Park Capital’s coyness over which insurer he headed, given Rexvale’s unusual name and prominent position. However I was unable to find any previous CV for Rexvale.

Where Rexvale found the time to be involved in energy and investments while simultaneously climbing the corporate ladder from humble secretary to Chief Executive Officer at a health insurer is also not clear.

The company claims to have been founded by Ronald Rexvale in 2012, yet in fact there is no public record of Ronald Rexvale’s involvement until 2017. In addition the company’s website was not registered until five months ago.

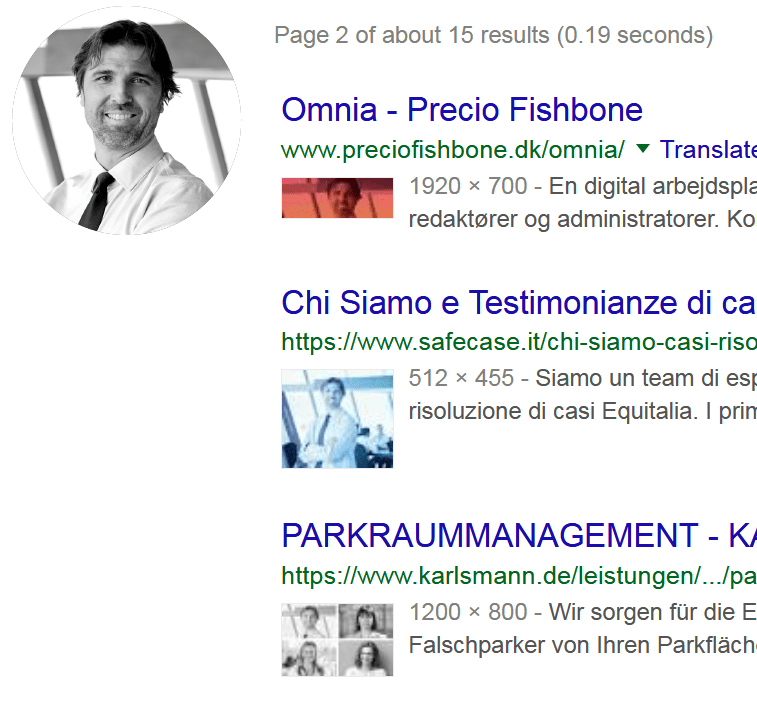

A reverse Google Image search showed that images in Milton Park Capital’s literature which purport to show Ronald Rexvale and at least one other director, Keith Campbell, are in reality stock photos.

If Rexvale looks anything like the stock photo in his company’s investment literature, I want the number of his plastic surgeon. According to Companies House he is 63 years of age.

This lack of transparency leads me to wonder whether whoever is actually behind the company – perhaps this Orfally suspicious character – took over a random dormant company, changed its name and registered false names with Companies House as its directors and shareholders, naming one of the directors after the old name of the company to help give the company a false appearance of longevity. Or just out of a lack of imagination.

Investors should think very carefully before investing with a company that uses stock photos to conceal the identity of its directors.

How safe is the investment?

These are unregulated investments into a micro-cap business and if Milton Park Capital is unable to make sufficient returns from its investments, or for any other reason runs out of money to service its bonds, it may default on payments of interest or capital.

Milton Park Capital’s last accounts show £6.3 million in assets, but these should not be relied upon by investors as they are unaudited. The company did not include a profit and loss account.

Its literature claims “We have a 100% track record of repaying interest and principal payments on time, to over 2,000 UK customers.” Companies House accounts show that the company had no borrowings as at 31 December 2017, and the company’s website was only registered in July 2018. Even if Milton Park Capital’s track record was longer than a few months, its claim to have met all its obligations to date is still, as I have discussed before, completely meaningless.

The difference between the rates on the company’s one year bonds and two year bonds is massive, and are a serious cause for concern. The difference between one- and two-year bonds issued by the same company is usually a percentage point or two, not seven. Why Milton Park Capital believes that that the risk of the company failing in year 2 is much greater than the risk of it failing in year 1 (hence the dramatically higher interest rate) is not clear.

The company’s literature is riddled with errors. For example, its literature states “When lending money to businesses Milton Park Capital place a fixed legal charge over the assets of the company we have borrowed funds too, which adds a extra layer of security In the event one of our borrowers were to default on the repayment of the principle loan and interest.” (The correct spelling here is “principal”.)

Under “Products”, its website states “The technology investments is a variety of areas relating to the research, development and/or distribution of technologically based goods and services.” This sentence is not just ungrammatical, but completely meaningless.

Should I invest in Milton Park Capital?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate loan note, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of up to 16.8% a year should be considered extremely high risk. As an individual, illiquid security with a risk of total and permanent loss, Milton Park Capital’s bonds are much much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Is my portfolio big enough that I could lose 100% of my investment and not worry about it?

The lack of clarity over the company’s history and leadership, and the bizarre disconnect between its one- and two-year interest rates, are all serious red flags. I am tempted to agree with Ms Katcontessa who fell for Naaman Orfally’s Air Force Lieutenant persona –

“use with caution” – except that would be a massive understatement. Do not proceed unless you are prepared for total losses.