A reader writes:

Dear Bond Review,

Thank you for drawing my attention to the Financial Ombudsman ruling on the IPM case.

I have read the Decision Note you link through to. What is particularly interesting to me, as an investor in loan notes, is these points:

- And the Security did not have any mechanism to enable the Security Trustee to prevent SEB from disposing of secured property which was a fundamental flaw. It meant the Security Trustee could not prevent SEB from paying most of the money raised for investing in solar projects in the UK to its parent in Australia – who then went bust.

What would be interesting to me would be to learn of example paragraphs in loan documentation that would have secured against this particular risk.

The short answer is that I don’t believe there is any way you can secure against this particular risk on an individual loan note basis, and certainly not by inserting paragraphs in the Information Memorandum.

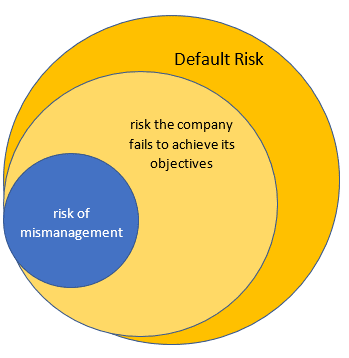

When you hand over money to a company to be invested on your behalf, there is always a risk that they won’t do with it what they said they would.

Once your money is in the hands of a company, the default position is that the directors can do with it as they see fit. What is there to stop them misusing it? There is no regulator or bondholder-appointed governess looking over their shoulder. The answer is mainly the threat of legal action against the company or the directors themselves if misuse results in a loss.

However, legal action is expensive and difficult, and the possibility of an investor recovering their money from the company or its directors may be slim. And, of course, legal action can only take place after the fact.

Let us say that back in 2013 the Secured Energy Bonds documentation included the line “Investor funds will be invested solely for the purposes described in this Information Memorandum and will not be invested in the parent company or any other third party”. SEB then goes ahead and transfers money to the Australian parent anyway. What can investors or the Security Trustee do about it? Not a lot. They probably wouldn’t have even found out until SEB went bust.

It is important to bear in mind that the risk of the company not doing what they said they would is only a small subset of a much larger risk – default risk. A company can do exactly what it said it would with investors’ money, and still fail to make sufficient returns to pay bondholders, because it does it badly, or has sheer bad luck. Any loan note is subject to default risk.

The vast majority of investors secure their investments against default risk by diversifying across hundreds or thousands of companies listed on regulated exchanges worldwide. The risk of any one company on a regulated exchange going bust is small, and diversification ensures that even though a small number inevitably will go bust during the course of a long-term investment, it will only have a negligible effect on the investor’s portfolio.

Some of those busts will be due to mismanagement, some incompetence, some bad luck and often a combination of all three. The investor doesn’t have any reason to care why a company went bust if it only means an imperceptible blip in their portfolio of less than 1%.

The vast majority of investors should not be put in a position where they have to worry about such things.

Have a question about investments? Worried about risk? Problems in the bedroom? Send your questions to the usual address, unless they’re about the last one.