A reader writes:

Dear Bond Review,

Thank you for drawing my attention to the Financial Ombudsman ruling on the IPM case.

I have read the Decision Note you link through to. What is particularly interesting to me, as an investor in loan notes, is these points:

- And the Security did not have any mechanism to enable the Security Trustee to prevent SEB from disposing of secured property which was a fundamental flaw. It meant the Security Trustee could not prevent SEB from paying most of the money raised for investing in solar projects in the UK to its parent in Australia – who then went bust.

What would be interesting to me would be to learn of example paragraphs in loan documentation that would have secured against this particular risk.

The short answer is that I don’t believe there is any way you can secure against this particular risk on an individual loan note basis, and certainly not by inserting paragraphs in the Information Memorandum.

When you hand over money to a company to be invested on your behalf, there is always a risk that they won’t do with it what they said they would.

Once your money is in the hands of a company, the default position is that the directors can do with it as they see fit. What is there to stop them misusing it? There is no regulator or bondholder-appointed governess looking over their shoulder. The answer is mainly the threat of legal action against the company or the directors themselves if misuse results in a loss.

However, legal action is expensive and difficult, and the possibility of an investor recovering their money from the company or its directors may be slim. And, of course, legal action can only take place after the fact.

Let us say that back in 2013 the Secured Energy Bonds documentation included the line “Investor funds will be invested solely for the purposes described in this Information Memorandum and will not be invested in the parent company or any other third party”. SEB then goes ahead and transfers money to the Australian parent anyway. What can investors or the Security Trustee do about it? Not a lot. They probably wouldn’t have even found out until SEB went bust.

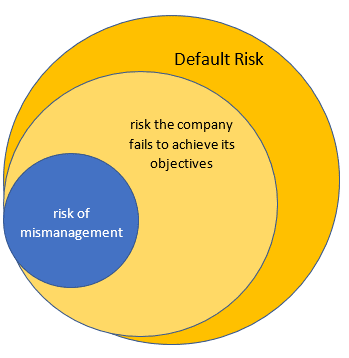

It is important to bear in mind that the risk of the company not doing what they said they would is only a small subset of a much larger risk – default risk. A company can do exactly what it said it would with investors’ money, and still fail to make sufficient returns to pay bondholders, because it does it badly, or has sheer bad luck. Any loan note is subject to default risk.

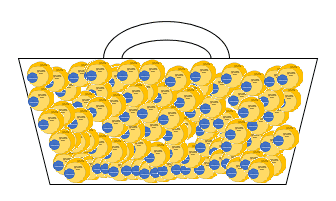

The vast majority of investors secure their investments against default risk by diversifying across hundreds or thousands of companies listed on regulated exchanges worldwide. The risk of any one company on a regulated exchange going bust is small, and diversification ensures that even though a small number inevitably will go bust during the course of a long-term investment, it will only have a negligible effect on the investor’s portfolio.

Some of those busts will be due to mismanagement, some incompetence, some bad luck and often a combination of all three. The investor doesn’t have any reason to care why a company went bust if it only means an imperceptible blip in their portfolio of less than 1%.

The vast majority of investors should not be put in a position where they have to worry about such things.

Have a question about investments? Worried about risk? Problems in the bedroom? Send your questions to the usual address, unless they’re about the last one.

Not sure exactly what the “reader’s” point is in relation to the article published by bondreview https://bondreview.co.uk/2018/09/25/ombudsman-directs-independent-portfolio-managers-to-pay-compensation-for-unregulated-bond-collapses-will-they-pay-up/ reporting on the Ombudsman’s ruling on IPM.

It comes across that the reader is arguing against the Ombudsman’s decision and basically suggesting it’s Mr. D’s own fault he lost a lot of money for not diversifying his portfolio. i.e the reader is arguing contributory negligence on the part of Mr. D.

If I am not mistaken, what the Ombudsman is describing, although not explicitly stated, is “tort by deceit”, and although IPM is not the one doing the deceiving, they allowed themselves to be complicit in the deception.

In the case of Hedley Byrne v Heller [1964] AC 465, the House of Lords held that a Duty of Care can exist in respect of a statement leading to pure economic loss, if the parties were in a ‘special relationship’. The ‘special relationship’ arises when the giver of the information knows the person it is given to is relying on it. An example of such a special relationship can be explained in this instance by:-

Mr. D. relied on IPM’s skill and judgement or their ability to make careful enquiry;

IPM knew, or ought reasonably to have known, that Mr.D was relying on them;

and it was reasonable in the circumstances for Mr D. to rely on IPM. Therefore IPM owed clients a duty of care.

The bullet under discussion is a quote from the Ombudsman’s decision note – under merits, bullet 7 – and in relation to that bullet point, the reader argues:

“… I don’t believe there is any way you can secure against this particular risk [i.e. that the risk the company doesn’t do with your money, what they said they would do with it] on an individual loan note basis, and certainly not by inserting paragraphs in the Information Memorandum.”

I don’t disagree with the reader but this is not the point being made by this ruling.

The Ombudsman is not arguing there exists such a way to mitigate this risk, nor suggesting the insertion of any paragraph mitigating this risk, but that the Information Document is misleading investors by suggesting IPM, in their special role as Security Trustee, are providing such a means to mitigate this risk, when in fact they are not.

IPM were acting as Corporate Director and Security Trustee and this was a major feature in the marketing of the investment, claiming that because of this, the bond was a safer investment than other bonds.

The bullet under discussion alleges IPM did not have any means to stop SEB from basically misusing investor’s money – which the reader acknowledges.

What the Ombudsman is basically saying is IPM ought to have “reasonably known” this was not possible and therefore the Security System was “not fit for purpose” as the Ombudsman puts it.

The information document was therefore misleading and IPM should not have approved it. The Ombudsman is consequently holding IPM to account for failing in their duty of care to potential investors and in particular Mr.D.

By the way, IPM would not have had this accountability had they not taken on the special roles as Corporate Director and Security Trustee! By taking on those roles they were providing a service to Mr.D and as such there was sufficient proximity that they owed him a duty of care.

I don’t think the reader was suggesting that at all. I edited their question slightly for publication so it might be my fault if it appears so.

My understanding is that the reader’s question boiled down to “How can I avoid a situation like Secured Energy Bonds if I am investing in unregulated loan notes?” and my answer boils down to “You can’t, so don’t invest all your money in unregulated loan notes.” I believe they were after guidance on their own future investments rather than apportioning blame for what happened with SEB.

I think the reader had made the common error of thinking you can eliminate default risk or other types of specific risk by “doing your research”. I.e., if the right magic words are in the offer document, you eliminate the risk of the company using the money for something other than the stated purpose (as SEB did by transferring the money to its Australian parent). As I have discussed before, this is not correct.

I agree with your analysis of the IPM Ombudsman case.

OK. I must have misread the question. No prob.

One more thing; the picture is puzzling me. Is the picture in the article implying Brev is female?

No comment ?