Update 3.10.19: At the time of this review Northbridge was known as The Capital Bridge. It has since renamed to First Northbridge Limited and changed its web address to northbridgeinvest.co.uk.

Northbridge continues to offer IFISA bonds paying 9% per year. The original review follows.

The Capital Bridge is offering three year bonds paying interest of 9% per year.

Money invested in The Capital Bridge (a trading name of Capital Bridge BondCo 1 Limited) will be loaned to Capital Bridging Finance Solutions Limited, which in turn will lend the money to property developers.

Who is The Capital Bridge?

Capital Bridge BondCo 1 Limited is 100% owned by Capital Bridging Finance Solutions Limited, which is in turn 100% owned by Paul Dalton.

Capital Bridging Finance Solutions was incorporated in January 2012. According to its last accounts (January 2017) it had net assets of £179k. The accounts were exempt from auditing due to Capital Bridging Finance Solutions’ small size.

Its subsidiary Capital Bridge BondCo 1 Limited (which is the company actually issuing the bonds) is more recent, incorporated in July 2018. Due to its young age it is yet to file accounts.

Capital Bridge BondCo 1’s other director is Mark Roberts.

Investors can access The Capital Bridge’s bond via an IFISA wrapper provided by Northern Provident Investments Limited. Northern Provident Investments provides ISA wrappers for a number of IFISA bond investments under its umbrella; according to the FCA Register, its current trading names include Northern Provident Investments Limited, Barbican ISA, Capital Bridge ISA, Choices ISA, Fluid ISA, Just ISA and Prime ISA.

How safe is the investment?

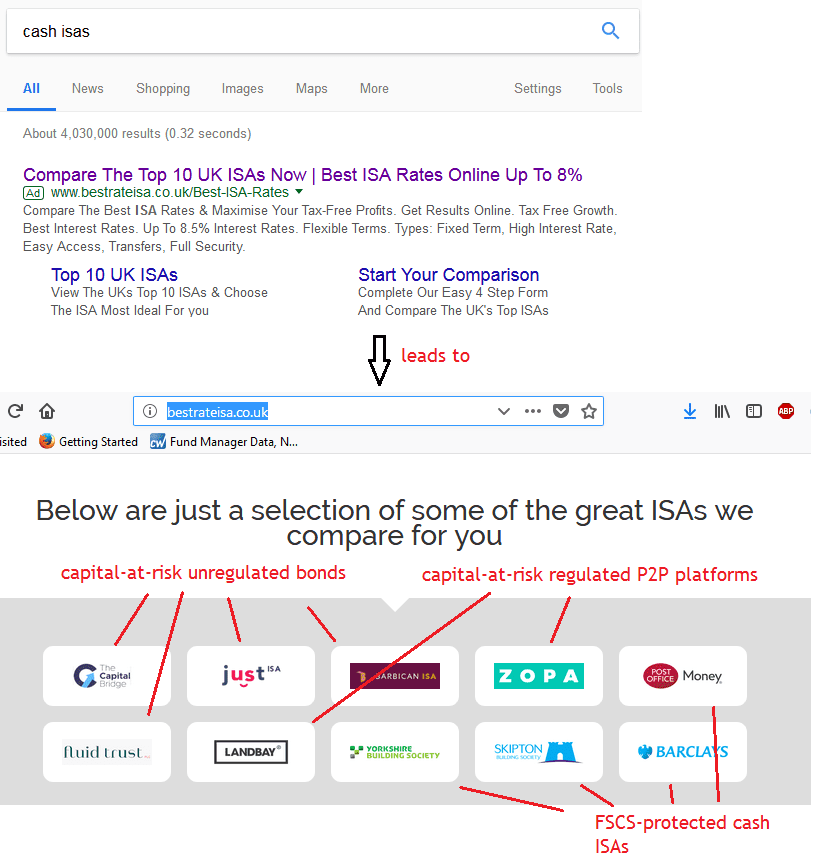

Capital Bridge, along with other capital-at-risk IFISA bonds under the Northern Provident Financial umbrella, is currently being promoted by unregulated introducers to UK investors searching on Google for cash ISAs.

These adverts are taken out by introducers independent of The Capital Bridge and the Capital Bridge cannot be held responsible for misleading promotions such as this one.

It is very important that investors understand that these investments are corporate loans and if The Capital Bridge defaults you risk losing up to 100% of your money. Unlike regulated cash ISAs (e.g. those offered by the Post Office, Skipton and Barclays) which are covered by the FSCS up to £85,000 if the authorised deposit-taker defaults.

The purpose of the bonds is to allow The Capital Bridge to lend money to Capital Bridging Finance Solutions, which will in turn use the money to lend to property developers.

If the Capital Bridge companies fail to make sufficient returns from their property loans, or for any other reason The Capital Bridge runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Asset backed investment

The Capital Bridge aims to mitigate risk by lending money to property companies and ensuring that the underlying loans are secured on the property being developed.

Investors should not assume that because the underlying loans are secured on property, there is no risk of losing money. It is still possible to lose money on secured loans if, for example, the property cannot be sold for enough money to repay the borrower in full or the borrower cannot enforce the security over the asset.

By investing in secured loans, The Capital Bridge aims to reduce the risk of losing money in its underlying business (property development lending). However, merely not losing money is not sufficient for this investment to succeed. The Capital Bridge needs to make enough money from its lending business to meet its set-up costs, salaries and other overheads, and then pay investors 9% each year, in order to be able to pay investors’ interest and capital on time.

Note that investors are investing in Capital Bridge BondCo 1, which in turn lends money to Capital Bridging Finance Solutions. It is Capital Bridging Finance Solutions which holds the security over properties in respect of its loans to developers, not Capital Bridge BondCo 1 itself.

This is a crucial distinction because if Capital Bridging Financial Solutions is unable to meet its obligations to Capital Bridge BondCo 1, the only security that investors will have is the assets of Capital Bridge BondCo 1 itself. In turn the only security that Capital Bridge BondCo 1 has is the assets of Capital Bridging Financial Solutions – some of which may be secured loans.

Long story short, any corporate loan note inherently has a risk of loss, even if it is secured and asset-backed. This is why they pay higher rates than FSCS-protected deposits.

Should I invest in The Capital Bridge ISA?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of 9% a year should be considered high risk. As an individual, illiquid security with a risk of total and permanent loss, The Capital Bridge’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

The investment may be suitable for high net worth and sophisticated investors who will already be well aware of all of the above risks, are looking to invest a small part of their assets in corporate lending, and feel that the return on offer (9% over three years) is sufficient for the risks involved in lending to a small unlisted company.