Apex Algorithms offers investment in sports betting arbitrage. Previously, according to a February 2018 Daily Mail article, the company was offering unregulated bonds paying 16% per annum. However, recent promotions from the company make no mention of a 16% per annum return and instead offer a “profit share” arrangement.

Profits are shared between Apex Algorithms and the investor according to how much they invest, as follows:

- Foundation £2,500-£5,000 40% / 60%

- Silver £5,000-£25,000 50% / 50%

- Gold £25,000-£50,000 55% / 45%

- Platinum £50,000+ 60% / 40% plus profits paid quarterly

Who are Apex Algorithms?

No details are provided on the Apex Algorithms website as to who is behind the business.

Apex Algorithms is a trading name of Apex Incorporated, although the registered company name is not mentioned anywhere on the website. Apex Incorporated is wholly owned by Nathan Burgoyne, the sole director.

Apex Incorporated was incorporated in July 2013, struck off the register in November 2014, and re-admitted to the register in April 2015. Its latest accounts (July 2016) show net assets of £641 and current assets of just under £19,000.

How safe is Apex Algorithms?

This is an unregulated investment and investors risk losing 100% of their money.

Apex Algorithms use investors’ money to invest in sports betting arbitrage. In betting arbitrage, investors look for two opposing bets on different exchanges that are priced in such a way that if they place a bet on both exchanges, they are guaranteed to make money. For example, if one bookie offers 11/10 on Anthony Joshua to beat Joseph Parker, and another bookie simultaneously offers 11/10 on Parker to win, you can place £100 with both bookies knowing that regardless of which way it goes, one bookie will pay you £210 and the other will take your money, leaving you with a £10 (5%) net profit.

In reality it would be extremely rare for two bookies to screw up quite so obviously. In reality, within minutes both bookies would adjust their odds to, say, 10/11 on both fighters – which means if you bet £100 on both you will lose £9. Also, it should be noted that if Joshua and Parker draw the match, you lose all your money.

Betting arbitrage, while a perfectly legitimate way to earn money, typically produces low returns in exchange for a great deal of time and effort to identify a suitable pair of bets.

Should Apex Algorithms fail to generate sufficient returns from betting arbitrage to meet its costs, or if it gets its bets wrong, there is a risk that investors may lose all their money.

Investors should also note that in a “profit share” arrangement, any interest due to investors who invested in Apex’s 16% per annum bonds must be paid first, before any profit is shared out with “profit share” investors.

Whether investors are invested in Apex via bonds promising interest of 16% per annum, or via a profit share investment, there is a risk of permanent and total loss should Apex Algorithms fail to make sufficient returns via arbitrage to cover interest payments and other costs.

Back testing / past performance?

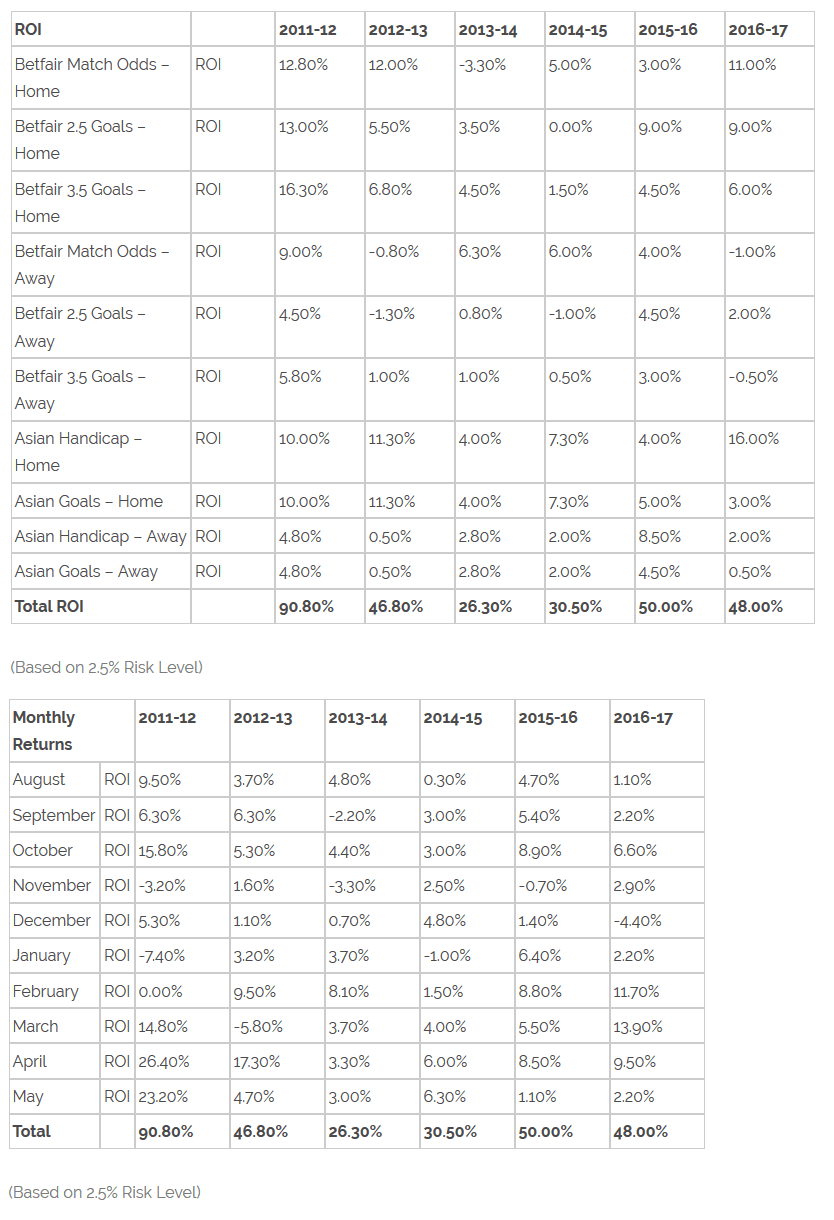

Apex Algorithms provide a table of “past performance” on its website and says this “reflects active trading as and on behalf of the Apex syndicate from 2014 to present day”, with results from 2011 reflecting the performance of syndicate members prior to forming the syndicate.

Confusingly, in a PDF brochure, the same table is referred to as “back testing”. The term “Back testing” refers to results that are not actual past performance, but results that an algorithm would have generated had it been applied in the past. “Back testing” and “past performance” are two completely different things – the former is theoretical performance, the latter is real performance.

Whichever they are, the numbers don’t add up.

Two tables are given; one shows the results broken down by ten types of bet, the other shows ten month-by-month returns.

(Why June and July are missing is not clear. The per-bet table shows only football bets, but Apex’s literature states that they invest in a variety of sports including tennis and American sports. Not all of these sports break off for the summer. Apex’s staff are entitled to a holiday the same as everyone else, but if the entire investment is suspended for two months each year, this should be disclosed.)

Both tables show a total return on investment at the bottom for each year, which, as you would expect, match each other. In each table, the figure in the “total” row is the sum of all the figures above (return per bet or return per month) – with a 0.1% difference in all but one year.

The problem is that in the first table, if Apex Algorithms divided investors’ money among the ten types of bets listed, the total return would be the weighted average, not the sum. If I have £100 and divide it equally between three bets returning 5%, 25% and -5%, I receive £108.30 and my return is 8.3%, not 25%.

The only way it could make sense for the returns per individual bet to generate the total listed is if Apex Algorithms invested all its investors’ money in “Betfair Match Odds – Home”, kept the 12.8% return in cash, reinvested the original stake in “Betfair 2.5 Goals – Home”, banked the 13% return, reinvested the original stake in “Betfair 3.5 Goals – Home”… and so on.

Quite apart from the illogic of Apex Algorithms investing sequentially in this way (the nature of arbitrage is that Apex needs to invest in whatever betting market is offering the opportunity to make risk-free returns), this would mean the table would have to at least show some similarity to the sequence shown in the month-to-month percentages. Not necessarily identical (it would make even less sense for Apex to spend a month investing in one type of bet and the next month investing in another type and so on) but if both tables show a series of sequential ROIs there should at least be some resemblance.

But the following table shows a completely different sequence of percentages. In 2011-12, for example, Apex Algorithms supposedly made a loss in two months even though all of its bets by category showed a profit.

Also note that if Apex Algorithms was reinvesting the profits from its successful bets, the annual total shown in the month-by-month table should be the product of the monthly ROIs plus one, not the sum. (109.8% * 106.3% * 115.8% * 96.8%… etc.) While Apex could conceivably bank profits in cash each month and only reinvest the original capital, why would it do so when it has a low-risk method of generating high returns?

I can only think of one explanation for why the returns in these tables do not correspond with each other or the correct method of calculating an overall annual ROI. What these tables actually show is two sets of made-up numbers which happen to add up to the same number at the bottom.

Should I invest with Apex Algorithms?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Apex Algorithms claim in their literature that this is a “Low risk investment” and their representatives claim “There will never be catastrophic loss like in the stock market.”

The reality is that investors risk up to 100% losses should Apex Algorithms fail to make sufficient returns from betting arbitrage to cover their costs – including the cost of their 16% per annum bonds.

As with any unregulated investment, it is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

There are also serious questions over Apex Algorithms’ supposed “backtesting / past performance” results.

Exercise extreme caution.