Apex Algorithms offers investment in sports betting arbitrage. Previously, according to a February 2018 Daily Mail article, the company was offering unregulated bonds paying 16% per annum. However, recent promotions from the company make no mention of a 16% per annum return and instead offer a “profit share” arrangement.

Profits are shared between Apex Algorithms and the investor according to how much they invest, as follows:

- Foundation £2,500-£5,000 40% / 60%

- Silver £5,000-£25,000 50% / 50%

- Gold £25,000-£50,000 55% / 45%

- Platinum £50,000+ 60% / 40% plus profits paid quarterly

Who are Apex Algorithms?

No details are provided on the Apex Algorithms website as to who is behind the business.

Apex Algorithms is a trading name of Apex Incorporated, although the registered company name is not mentioned anywhere on the website. Apex Incorporated is wholly owned by Nathan Burgoyne, the sole director.

Apex Incorporated was incorporated in July 2013, struck off the register in November 2014, and re-admitted to the register in April 2015. Its latest accounts (July 2016) show net assets of £641 and current assets of just under £19,000.

How safe is Apex Algorithms?

This is an unregulated investment and investors risk losing 100% of their money.

Apex Algorithms use investors’ money to invest in sports betting arbitrage. In betting arbitrage, investors look for two opposing bets on different exchanges that are priced in such a way that if they place a bet on both exchanges, they are guaranteed to make money. For example, if one bookie offers 11/10 on Anthony Joshua to beat Joseph Parker, and another bookie simultaneously offers 11/10 on Parker to win, you can place £100 with both bookies knowing that regardless of which way it goes, one bookie will pay you £210 and the other will take your money, leaving you with a £10 (5%) net profit.

In reality it would be extremely rare for two bookies to screw up quite so obviously. In reality, within minutes both bookies would adjust their odds to, say, 10/11 on both fighters – which means if you bet £100 on both you will lose £9. Also, it should be noted that if Joshua and Parker draw the match, you lose all your money.

Betting arbitrage, while a perfectly legitimate way to earn money, typically produces low returns in exchange for a great deal of time and effort to identify a suitable pair of bets.

Should Apex Algorithms fail to generate sufficient returns from betting arbitrage to meet its costs, or if it gets its bets wrong, there is a risk that investors may lose all their money.

Investors should also note that in a “profit share” arrangement, any interest due to investors who invested in Apex’s 16% per annum bonds must be paid first, before any profit is shared out with “profit share” investors.

Whether investors are invested in Apex via bonds promising interest of 16% per annum, or via a profit share investment, there is a risk of permanent and total loss should Apex Algorithms fail to make sufficient returns via arbitrage to cover interest payments and other costs.

Back testing / past performance?

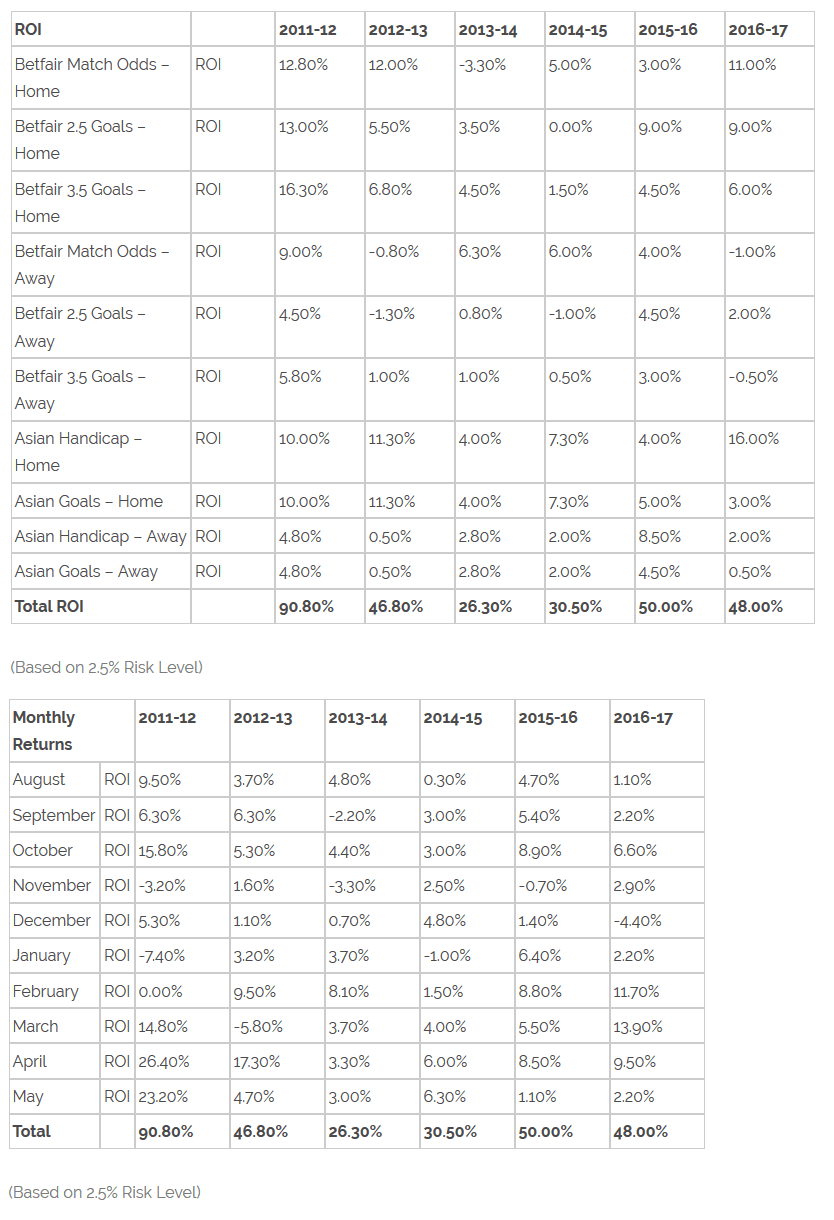

Apex Algorithms provide a table of “past performance” on its website and says this “reflects active trading as and on behalf of the Apex syndicate from 2014 to present day”, with results from 2011 reflecting the performance of syndicate members prior to forming the syndicate.

Confusingly, in a PDF brochure, the same table is referred to as “back testing”. The term “Back testing” refers to results that are not actual past performance, but results that an algorithm would have generated had it been applied in the past. “Back testing” and “past performance” are two completely different things – the former is theoretical performance, the latter is real performance.

Whichever they are, the numbers don’t add up.

Two tables are given; one shows the results broken down by ten types of bet, the other shows ten month-by-month returns.

(Why June and July are missing is not clear. The per-bet table shows only football bets, but Apex’s literature states that they invest in a variety of sports including tennis and American sports. Not all of these sports break off for the summer. Apex’s staff are entitled to a holiday the same as everyone else, but if the entire investment is suspended for two months each year, this should be disclosed.)

Both tables show a total return on investment at the bottom for each year, which, as you would expect, match each other. In each table, the figure in the “total” row is the sum of all the figures above (return per bet or return per month) – with a 0.1% difference in all but one year.

The problem is that in the first table, if Apex Algorithms divided investors’ money among the ten types of bets listed, the total return would be the weighted average, not the sum. If I have £100 and divide it equally between three bets returning 5%, 25% and -5%, I receive £108.30 and my return is 8.3%, not 25%.

The only way it could make sense for the returns per individual bet to generate the total listed is if Apex Algorithms invested all its investors’ money in “Betfair Match Odds – Home”, kept the 12.8% return in cash, reinvested the original stake in “Betfair 2.5 Goals – Home”, banked the 13% return, reinvested the original stake in “Betfair 3.5 Goals – Home”… and so on.

Quite apart from the illogic of Apex Algorithms investing sequentially in this way (the nature of arbitrage is that Apex needs to invest in whatever betting market is offering the opportunity to make risk-free returns), this would mean the table would have to at least show some similarity to the sequence shown in the month-to-month percentages. Not necessarily identical (it would make even less sense for Apex to spend a month investing in one type of bet and the next month investing in another type and so on) but if both tables show a series of sequential ROIs there should at least be some resemblance.

But the following table shows a completely different sequence of percentages. In 2011-12, for example, Apex Algorithms supposedly made a loss in two months even though all of its bets by category showed a profit.

Also note that if Apex Algorithms was reinvesting the profits from its successful bets, the annual total shown in the month-by-month table should be the product of the monthly ROIs plus one, not the sum. (109.8% * 106.3% * 115.8% * 96.8%… etc.) While Apex could conceivably bank profits in cash each month and only reinvest the original capital, why would it do so when it has a low-risk method of generating high returns?

I can only think of one explanation for why the returns in these tables do not correspond with each other or the correct method of calculating an overall annual ROI. What these tables actually show is two sets of made-up numbers which happen to add up to the same number at the bottom.

Should I invest with Apex Algorithms?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Apex Algorithms claim in their literature that this is a “Low risk investment” and their representatives claim “There will never be catastrophic loss like in the stock market.”

The reality is that investors risk up to 100% losses should Apex Algorithms fail to make sufficient returns from betting arbitrage to cover their costs – including the cost of their 16% per annum bonds.

As with any unregulated investment, it is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

There are also serious questions over Apex Algorithms’ supposed “backtesting / past performance” results.

Exercise extreme caution.

Dear Sirs,

I am writing on behalf of Apex Algorithms regarding your article online. I was directed to your review, read your piece on Apex and there were simply many inaccuracies.

I totally appreciate the theme of your articles in general; to highlight risk factors of investments which are usually unregulated. However, to be considered a ‘review,’ one would think that the analysis should be a balance of positives, negatives, and then a considered conclusion. These articles are breathtakingly slanted and critical. This would be justified perhaps, if it is beyond doubt that the businesses do not offer viable. However, it is deeply unfair when we are legitimate business, we fairly represent our performances every week, good and bad, and are honest with investors about the business and industry.

From the start of your article, with the title ‘investment in sports betting arbitrage,’ the article misses the point. Although I am aware of successful arbitrage strategies, we have never ever used this approach and never suggested such to clients. There are then several paragraphs in your article detailing what you consider our strategy to be. It would be useful for potential investors to understand if this was our method. But, as stated, it is not and we have never suggested it is.

A subsequent paragraph warns about 16% being paid before profit shares to clients. This is simply not true and again, no literature from us would ever give that impression. We offer a straight down the line split. If investors are on a 50:50 profit split, then if the model increases by 10%, we give an investor 5% and we take the other 5%. If it were to drop, then the same principle applies.

As a side note, arbitrage strategies aim to make safe, risk free profits, so if you thought that was our approach, it seems utterly sensationalised and unrealistic to further write about total defaults.

The ‘discussion’ regarding our performance tables seems to suggest our figures ‘don’t add up.’ Well, if I may correct your response – they DO add up. The figures clearly represent soccer markets (2.5 and 3.5 goals trades, Asian handicaps, Asian goals… clearly soccer). Further, the reason that there were no June and July figures was because major European leagues do not play over the summer. Our stats represent across five years, and only recently have we traded the lower liquidity leagues over the summer months. It was a natural progression but it takes a long time to add new leagues to our trading.

The article discusses why the figures must be wrong, you detail a ‘sequential betting’ process which you say we are suggesting. It is the most baffling and confusing method I have ever heard about. What our figures display is not complicated mathematics. It is simple. If we started with £100 and across the course of the season, overall, we made profit in match odds of £20 and profit in goals markets of £15, then, we would tell investors we made profit of 20% and 15% respectively. It is as simple as that. Nothing more complicated and not in need of your six paragraphs of speculation.

One of your paragraphs actually makes me laugh out loud: “Apex supposedly made a loss in two months even though all the bets by category showed a profit.’ Do I honestly need to explain this? Over a two month period, across all the trades, there was a loss. However, the other table displays profits by markets for each year. So the two tables are displaying different information for different periods of time. Therefore, they cannot be compared in the way that you do. We do lose money some months, but across a year, markets usually show a profit.

I feel that your article is misrepresentative, makes false assumptions and gives inaccurate analysis and misleading conclusions. However, I do appreciate that your site wishes to make investors aware of the potential pitfalls when investing. That is a useful sentiment. However, when it is applied in this way to a healthy and decent company like Apex, I feel that is simply not justified. We maintain positive relations with all stakeholders and have always been honest through the good times and bad.

Kind Regards,

Nathan Burgoyne – Director

No they aren’t. The positives of any investment are the potential return, which is the profit share element, and are described in full at the top of the review. The negatives of any investment are the potential risks, which come after. As the postives are listed first, if anything the article is slanted towards the positives.

I assumed that as your literature talks about “low risk” in relation to sports betting, you were employing an arbitrage strategy. Instead you are relying on your perception of the odds being different from that of the bookmakers? This is simple gambling, whatever methods you may use to calculate the odds, and the repeated description of this strategy as “low risk” is highly misleading. If you are wrong and the bookmakers are right, investors stand to lose up to 100% of their money.

It has been documented in the Daily Mail that your company previously offered bonds paying 16% per annum to investors. If any of these bonds were taken up, then your interest payments to your investors in the 16% per annum bonds come out of the profits to be distributed to investors in the profit share.

That makes about as much sense as the two “Total” rows adding up to (almost) exactly the same percentages, which is the issue highlighted in my review.

If you started with £100 and made £20 in match odds and £15 in goals markets, the profits cannot be 20% and 15% because you couldn’t have invested the same £100 in both at the same time. If you split the £100 evenly between the two markets, the profits would be 40% and 30%. If you put £100 in match odds and made £20, then put the £120 into goals markets and made £15, the profits would be 20% and 12.5%.

Whoever put your tables together does not understand maths, either complex or simple.

You have not attempted to address the simple mathematical fact that the “Total” yearly ROI from a series of monthly ROIs (displayed in the second table) is the product of all the monthly returns, not the sum; multiplied together, not added.

If the percentages represent what you describe, there is no way in which the sum of the percentages in the two tables should add up to the same figures. Simple enough?

Simple enough? … Yes, you explain things very simply but you are unfortunately wrong… again.

Sir, your reply made no apology for utterly misrepresenting our trading strategy for several paragraphs. Even an acknowledgement of being a little too eager when making assumptions would have sufficed. However, from this, it is clear that you have no intention at all to offer a balanced critique.

You suggested that you are actually biased in our favour in your article.. although that was a funny quip, you misrepresented our product repreatedly, which seems pretty misleading. Further, to suggest that, if we do not do arbitrage then we are simply gambling is again blatantly flippant and misleading. What your amusing is that, you stated originally that it is dangerous to execute an arbitrage strategy. Now, in your reply, you state how it is dangerous if it isn’t arbitrage. Dangerous if it is and dangerous if it isn’t?. With no caveats stated? We trade based on a statistical model. It might be correct to argue that it is only useful if the probabilities generated are accurate enough to allow generation of steady positive returns. However, to simply accuse it of being gambling is again an unreasonable assumption. Almost all financial trades by professionals use a statistical model in some form, and most major business project proposals would use a model to calculate expected returns. Just because there is uncertainty attached to a forecast does not make it ‘simple gambling’.

A couple of other points; we do not assume from our figures that we invest all the funds at the same time. We make possibly hundreds of trades per month across each market, often for tiny fractions of the total pot. However, if over the month, there was a profit of for example 5%, then we would quote that. This method is perfectly reasonable.

Finally, you commented on paying bond holders 16% before syndicate members. We structure the profit share in a fair way and it is as simple as we have written. If this was debt versus equity, then bond holders would of course be paid first. However, it is not. When a syndicate member adds funds, it does not become the company’s money to use as it likes. Syndicate funds are in a segregated account which is solely for trading. The company then splits the profits according to the ratio and uses it’s own share to its own objectives. Therefore, it would not pay any bond / debt holders before syndicate members.

Best Wishes

N.B

Betting on the outcome of sports matches is gambling. What method or statistical model is used to arrive at the outcome to bet on does not alter that. Nor does it alter the fact that describing a gambling syndicate as “low risk investment” is misleading.

Since the long explanation is lost on you, let’s give it one more go in simple terms.

1) Why is the “Total” row at the bottom of the first table the sum of the preceding rows, when the overall return from a column of different investment categories is the weighted average (each return multiplied by its percentage contribution to the total investment, then all of those weighted returns added together), not the sum?

2) Why is the “Total” row at the bottom of the second table the sum of the preceding rows, when an annual return is the compounded return of the monthly returns (the product or multiplication of all the monthly percentage returns +1), not the sum?

And for bonus points: what regulatory authorisation does Apex Algorithms have to run a collective investment scheme in the United Kingdom?

I came here after googling apex and wanting to learn more about it. And I must say that having spent an hour looking into it, it was clear to me that the author of this article completely failed to understand how Apex works. Cmon Brev, have another look at the two tables or ask someone to explain them to you, it’s really not that hard and they make complete sense. If anything, Nathan’s cool headed responses only made me more likely to test it out.