Bond on Blockchain is an equity cryptocurrency investment traded on the BitShares platform.

The Bond is designed as a five year investment, with investors permitted to redeem 60% of the Net Asset Value after one year, 70% after two years, 80% after three years, 90% after four years and 100% after five years.

The Bond can also be traded on the BitShares platform at any time provided a market exists.

However, under US securities law, the bonds are “restricted securities” and therefore may not lawfully be sold until one year after purchase.

The Bond’s funds are invested as follows:

- 30% in unregulated bonds issued by UK property companies

- 30% in the Billion Hero Campaign

- 30% in lending Bitcoin to speculators

- 10% in alternative cryptocurrencies

The literature states that the investments “will provide Bond with a steady rate of return, projected at a minimum annual rate of 8% of Net Asset Value”. This is however a projection; no fixed rate of return is promised and the bond’s Form D filing with the SEC describes it as an equity investment, meaning the value will depend purely on the value of its underlying assets (loans to property companies, loans to Bitcoin speculators, the HERO cryptocurrency and alternative cryptocurrencies).

Who are Bond on Blockchain?

Bond on Blockchain is managed by Euskara Management Ltd, registered in Belize.

Robert John Edwards is the sole director and shareholder of Euskara Management and is described in the literature as the founder of the investment. Edwards is also the owner of Vino Beano Limited, a UK wine seller, and was previously the founder of a UK recruitment consultancy, Burrows & Grey Limited (formerly Be A Sport @ Work Limited). Burrows & Grey was dissolved in 2016.

Is Bond on Blockchain regulated?

On Edwards’ LinkedIn profile, Bond on Blockchain is described as “Regulated and 100% Asset Backed.” However, the company has filed with the SEC under Rule 506(c), meaning it is exempt from most of the stringent securities regulations in the US and is to all practical purposes unregulated. Bond on Blockchain is not required to file with the SEC beyond a very short Form D notice.

The Rule 506 exemption means that Bond on Blockchain may only be promoted to “accredited investors”, which generally means investors who earn over $200,000 per annum or have net wealth of $1 million excluding your house. Firms relying on Regulation D 506(c) must take reasonable steps to ensure investors qualify as accredited “which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like.” (SEC.gov)

Sitting slightly uneasily with the requirement to be promoted to accredited investors is a cartoon promotion for Bond on Blockchain featuring the Spot The Dog kiddy language currently beloved of adpeople (This is Tim. Tim has Bitcoin, but the value always fluctuates” etc), the worst beard ever seen in financial advertising,

…and the kind of sexism we thought went out of style fifty years ago (“Tim is very happy. Because now he can tell his wife that they have a secure savings option on the blockchain.”) with a simpering housewife who is seemingly only prevented from sticking her heel in the air and kissing Tim on the cheek by the animators’ inability to draw people from the waist down.

But accredited investors are unlikely to make their investment decisions based on the merits of cartoon adverts, so let’s move swiftly on.

How safe is the investment?

The 30% allocated to cryptocurrency lending is straightforward enough. Bond on Blockchain lends out investors’ money to Bitcoin speculators who attempt to make money speculating on Bitcoin. If they succeed, they can pay Bond on Blockchain back from their profits, but if they fail, there is a risk to Bond on Blockchain that they cannot repay their loans.

https://bondonblockchain.com/asset/ shows that the 30% to be allocated to “Property bond / real estate” will be allocated to three unregulated loan notes issued by UK property companies: Blackmore Bond, Marcello Developments and Nova Prime.

This means that 60% of Bond on Blockchain’s assets consist of fixed interest loans to third parties – UK property companies and cryptocurrency speculators.

The 10% to be invested in alternative cryptocurrencies is self-explanatory.

The 30% to be invested in the “Billion Hero Campaign” is where things get distinctly murky.

Billion Hero Campaign

The PDF literature states that 30% of investors’ money will be invested in the Billion Hero Challenge.

The Billion Hero Challenge was a proposed “contest” from the founder of the HERO cryptocurrency. Bond on Blockchain’s literature refers to the Billion Hero contest as involving the purchase of BitShares. This is not correct – HERO is a separate currency, which is collateralised using BitShares.

HERO’s founders claim that HERO is designed to appreciate by 5% each year with reference to the US dollar. This is achieved via its collateralisation with BitShares, on the grounds that as BitShares rise in value, the HERO will be able to deliver guaranteed returns of 5% per annum from its share in BitShares’ profits.

There is clearly a risk that BitShares fails to make sufficient profits to allow investors in HERO to cash out at the value of BitShares +5%pa.

We will leave the merits of HERO aside at this point and focus on the Billion Hero Challenge. The rules were simple: a prize fund containing a million dollars worth of HERO would be set aside at the beginning of the contest. Teams of contestants would be encouraged to buy and bid up the price of HEROs until the point that the value of the prize fund reached a billion dollars. At the point the prize fund reached a billion dollars, it would be divided among the twelve teams holding the most HEROs.

I use the past tense because the contest appears to have flopped. The total value of all HERO in existence (market cap) is currently under a million. The contest was to be tracked using a leaderboard on https://sovereignhero.com/, but of this there is no sign. Coinmarketcap.com suggests that the total market cap of HERO has never exceeded a million dollars, so clearly it was not possible to start with a prize fund of a million dollars.

Even if it had successfully launched, the contest strongly resembles a pump and dump scheme. If people are buying HERO in the hope of a) increasing the prize fund value to a billion dollars and b) holding more than other contestants at that point, then when they win the prize, all they have is “a billion dollars worth” of a currency that nobody wants to buy anymore, as the reason for buying it has evaporated.

This problem was explained away by the HERO founder as follows: by the time the prize fund reaches a billion dollars, HERO will be in use as a currency to such an extent that the disappearance of the Billion-Hero-Challenge-led demand will not have a material effect on the price.

With the collapse of the Billion Hero Challenge and HERO’s market cap yet to breach $1 million, it is impossible to say whether mass adoption of HERO was ever a realistic possibility.

Nonetheless, it is notable that Bond on Blockchain, while claiming that “In a market of volatility and ‘get-quick-rich’ promises, Bond offers security and stability”, planned to invest 30% of investors’ money in a get-rich-quick scheme, until it flopped at launch.

HERO now appears to be running something called the Billion Hero Campaign, which “was conceived as a unique platform designed for fundraisers, charities, and foundations with a noble cause”. https://bondonblockchain.com/asset/ now lists the Billion Hero Campaign as the destination of 30% of funds.

It is not clear how exactly charity fundraising is expected to deliver a return for Bond on Blockchain investors. No explanation on how the campaign works is provided by billionherocampaign.com, other than some YouTube videos which demonstrate how to use the website.

Collapse in value

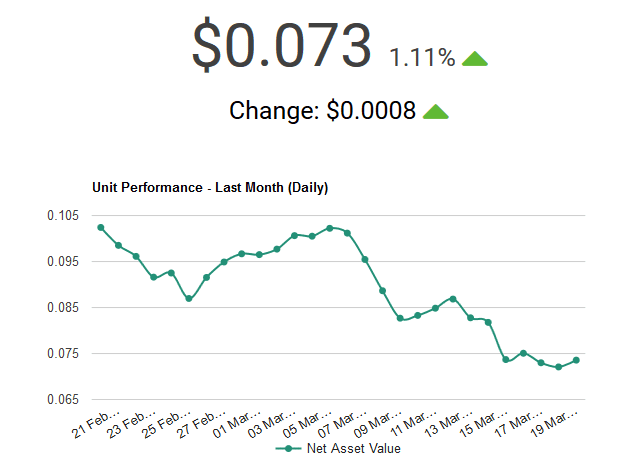

According to the literature, “an initial 5,000,000 Bond Units have been made available for presale purchase, at an initial $1 per unit, with the minimum level $500. At the time of writing, Bond Unit’s value has already reached $1.368 – a 36.8% rise.” The URL of the document dates this literature to December 2017.

As of March 2018, Bondonblockchain.com shows the value has collapsed to 7.3 cents.

Charges and costs

No details are given in the literature or in the Form D filing with the SEC as to what management fees will be collected from Bond on Blockchain, or any other details on how the cost of Robert Edwards’ management of the fund will be paid.

Should I invest with Bond on Blockchain?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Bond on Blockchain has certainly had a rough start to life given that its literature states that its shares were traded at $1.368 in December 2017, and the value has since collapsed to 7.3 cents at time of writing (nearly a 95% loss) according to its website.

Accredited investors who sense a buying opportunity should be aware that they are investing in assets which all have a possibility of total and permanent loss, namely

- “alternative cryptocurrencies” (which may fail to gain acceptance and collapse in value or become untradeable)

- loans to unregulated property companies Blackmore, Marcello Developments and Nova Prime

- loans to cryptocurrency speculators

- and the HERO cryptocurrency via the Billion Hero Campaign.

Buying a product which has lost 95% of its value only makes sense if you have concrete reason to believe that the underlying assets are undervalued by the market and will recover in value, or if you regard the investment as a total gamble and are prepared for 100% losses.

With a 95% fall in value from its December 2017 price and a 92% fall from its initial offering price, Bond on Blockchain has clearly failed in its aim to reduce the volatility associated with cryptocurrency.

Bond on Blockchain’s failure to disclose its charges (or however it pays for the cost of Edwards and others managing the fund) anywhere in its literature or website is disappointing in this day and age.