Under UK law and regulations, unregulated corporate loan notes should only be offered to high-net-worth or sophisticated investors. (In the regulatory jargon, they are considered non-mainstream pooled investments, being debentures issued by “special purpose vehicles”, an issuer whose objects and purposes are primarily the issue of securities.)

“Sophisticated” does not mean “clever”. It has a specific definition, meaning a member of an angel investment network, a previous investor in unlisted companies, a private equity professional, or a director of a company with a turnover over £1 million.

Leaving the regulations aside, it is a basic principle that inexperienced investors should not be investing significant amounts of their capital in an investment which has a material risk of total and permanent loss.

Many unregulated firms are currently very keen to promote their high ratings on Trustpilot. Often they display 5-star Trustpilot icons on the home page of their website.

When reading the reviews left on Trustpilot for the issuers of unregulated loan notes, it is clear just how many are highly unlikely to be sophisticated or high-net-worth investors.

In an unscientific survey, I have read through around 300 reviews left for one particular issuer and counted those which showed strong evidence that the reviewer was neither a high net worth investor or sophisticated investor.

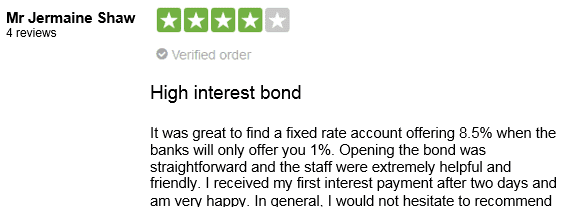

I marked a review as definitely unsophisticated if it stated explicitly that they did not have much experience of investing, appeared to believe they had invested in a deposit account or that the investment was otherwise capital protected, used very broken English, or were under the impression that they had been given advice by the issuer (which they are not authorised to do).

I marked a review as possibly unsophisticated if they seemed to place excessive importance on customer service and the friendliness of the customer representatives, or on receiving their first interest payments promptly.

How efficient and customer-friendly an investment company is should really be of very little interest to a high-net-worth or sophisticated investor. Many of them will be using intermediaries or assistants to deal with their investments on their behalf. Even if they are managing their investments personally, they only have to deal with the company twice over a period of several years – at the beginning, and when they withdraw their money.

Many of these firms have been in operation for less than five years and the fact that they have so far dealt promptly with applications and made interest payments on time is of very little significance.

I found that out of 300 reviews, 32 displayed definite evidence of being from an unsophisticated investor, and a further 40 were possibly unsophisticated.

Most of the reviews were too short to draw any conclusions from.

72 out of 300 may be a minority, but it is a very high amount given the unsuitability of these investments for retail investors. It is likely to represent several millions of pounds worth of life savings at risk. Only 7 reviews showed clear awareness that their capital was at risk.

Two Trustpilot reviewers even left reviews to say that they were not happy about being repeatedly asked by the issuer to leave a review on Trustpilot when they had only been invested for a week.

I have not named the company for two reasons. Firstly, because this survey is inherently subjective. Secondly, because of the possibility that the company’s bonds were sold by unrelated third parties and the issuer itself is blameless for any particular review.

To make it a bit more scientific, I looked up the Trustpilot page for a regulated firm, Octopus Investments, which also invests in asset-backed lending and property finance, but offers its products almost entirely via regulated financial advisers. In statistics, this is known as a “control group”. It had no reviews whatsoever on Trustpilot.

I tried two of its larger rivals, TIME Investments and Foresight Group: they also had no reviews on Trustpilot. So from my control group I draw the conclusion that firms that do not offer their products to retail investors do not get reviewed on Trustpilot, even if they have been around for many years with a good track record.

Conclusion

This is a highly unscientific survey and does not constitute evidence that any individual investor should not have taken out an unregulated corporate loan note.

And there is no reason whatsoever to believe that the 72 people who are or may possibly have invested without understanding the risks will not in due course receive their original capital on time and be perfectly satisfied.

We will keep our fingers crossed.