Allansons, in association with Mortgage Audit Services Limited, are offering investors the opportunity to invest in “litigation funding” whereby investors fund the cost of legal action on behalf of a mortgage customer who has been overcharged by their lender due to “automatic capitalisation” of payments in shortfall.

Should the case succeed, Allansons promises a return of 5% of any award plus 30% of Allansons’ base legal fees, which they estimate will provide a return of “approximately 50% on your money within 6 to 18 months.”

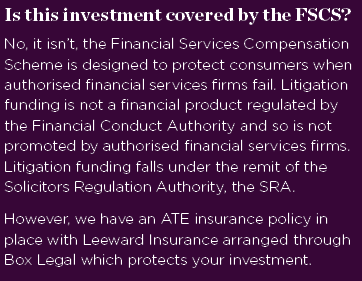

Should the case fail, Allansons promise that your investment is covered by After The Event insurance.

The investment is not promoted on Allansons’ website (and Mortgage Audit Services does not appear to have a public presence) but unregulated introducers have been promoting the investment to members of the public without proof that they are sophisticated or high net worth investors, one of whom passed the details to us.

Who are Allansons LLP?

Allansons is a Limited Liability Partnership with two partners: Roger Allanson and Mohamed Patel. The Partnership had net assets of £98,000 according to their last accounts filed November 2016; as a small company they did not have to audit the accounts or include a profit and loss statement.

Who are Mortgage Audit Services?

Mortgage Audit Services was incorporated in November 2015. It has yet to file accounts as an active company; its only previous accounts in November 2016 were filed as a dormant company. It is owned 72%/28% by the directors Bryan Turner and Charles Haynes.

How safe is the investment?

This is an unregulated investment and if Allanson fails to win the case, and the insurer does not or cannot return your initial capital, you risk losing 100% of your money.

We are not legal experts and cannot comment on the specific merits or otherwise of Allansons’ cases, but it is a truism that no case is guaranteed to succeed in court. Allansons say they “expect to win” and say “The audit report that we use in these breach of mortgage contract claims has been given a 75% chance of success in court” but it is the judge that decides.

If the case fails, Allansons / MAS claim that an insurer providing After The Event insurance, Leeward Insurance, will step in and return investors’ money.

However investors are still at risk of losing money if:

- Leeward Insurance does not pay out (e.g. because an exclusion in the insurance contract applies)

- Leeward Insurance has insufficient resources to return investors’ money

Leeward Insurance is based in the offshore tax haven of Bermuda. There is virtually no public information available on Leeward Insurance.

Should I invest in litigation funding with Allansons / Mortgage Audit Services Ltd?

This blog does not provide financial advice. The following are statements of fact based on publicly available information, or widely accepted investment principles; they are not personalised recommendations. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated investment, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment promising returns of 50% between 6 and 18 months is clearly very high risk in nature.

Before investing investors should ask themselves:

- How would I feel if the case failed, the insurer did not pay out and I lost 100% of my money?

- Do I have a sufficiently large portfolio of investments that the loss of 100% of this investment would not damage me financially?

- If I am placing any reliance on the insurance contract with Leeward Insurance, have I conducted sufficient due diligence to ensure the insurance contract is watertight, and that Leeward Insurance has sufficient resources to return investors’ money?

If you are looking for an investment that provides “security”, you should not invest in unregulated products with a risk of 100% capital loss.

Background

In 2010 the Financial Services Authority (now the Financial Conduct Authority) introduced a regulation stating that if a mortgage customer falls behind with their repayments, the mortgage lender should not automatically add the shortfall into the calculation of their repayments – thereby increasing the amount the customer had to pay when they were already struggling to afford the original amount.

Some mortgage lenders have carried on with this practice regardless, and Allansons is seeking investors’ money to allow these customers to sue their mortgage lender for the amount they have been overcharged.

One thing that is unexplained in Allanson’s literature is why people who have been the victim of automatic mortgage capitalisation need legal funding in the first place. In April 2017, the FCA wrote to mortgage lenders instructing them to “review whether they have… automatically included payment shortfalls in their CMI calculations; if they have, review whether this practice has caused harm to customers… if so, assess and provide appropriate remediation”.

In other words, as with PPI and 1990s pension misselling, mortgage lenders are required to proactively find out if their customers have been the victim of this practice, and if so, offer them redress, without waiting for the customer to complain.

If the mortgage lender fails to do this, the customer can complain directly to the mortgage lender. If the mortgage lender still fails to offer redress, the customer can take their complaint to the Financial Ombudsman, a simple process which by design does not need legal assistance.

It would be possible for Allansons to handle a customer’s complaint to the Ombudsman on their behalf, but the rewards for doing so would be limited to a cut of the customer’s compensation; the Ombudsman does not award legal costs. This would certainly not generate a 50% return to investors.

Nowhere in the literature does it explain why mortgage customers should take their lender to court when they have the option of going to the Financial Ombudsman.

Indeed, judges now generally expect people to attempt alternative dispute resolution (ADR) before going to court; the Financial Ombudsman is one of those means of alternative dispute resolution. So if a customer takes their mortgage lender to court instead of going to the Ombudsman, there is a significant chance the case would be thrown out.

However, we reiterate that we are not legal experts and cannot comment on the legal merits of Allansons’ potential cases.

What is a matter of objective fact is that a) if the case does not succeed and Leeward Insurance does not pay out, investors will lose up to 100% of their money b) unregulated investments with potential to lose up to 100% of investors’ money are only suitable for sophisticated or high net worth investors as a small part of their portfolio.