Castle Trust Direct plc offers corporate loan notes paying 2% per annum for one year, 2.15% for 2 years, 2.3% for 3 years and 2.5% for 5 years.

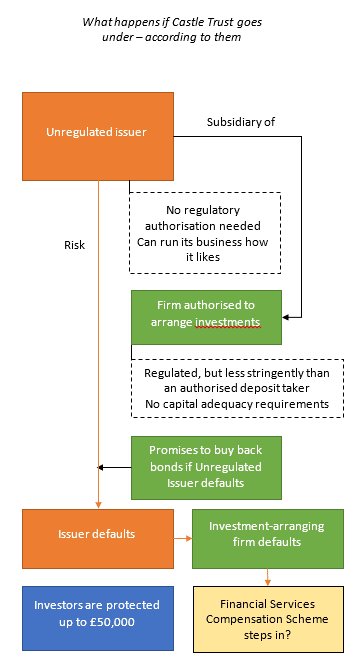

An interesting feature of the bonds is that on maturity, the bonds will either be redeemed by Castle Trust Direct plc, or, if Castle Trust Direct plc is unable to redeem the bonds, Castle Trust Capital plc will repurchase them. Castle Trust claims that this obligation to repurchase the bonds – the “Repurchase Facility” – is covered by the Financial Services Compensation Scheme. For more analysis of this claim, read on.

Previously the company offered loan notes with returns linked to the Halifax House Price Index; these have been withdrawn from sale.

Status

Open to new investment.

Who are Castle Trust?

Castle Trust Capital plc was incorporated in 2010 as Morgan Trust Capital, changing its name to Castle Trust Capital in 2011.

Castle Trust Capital plc, which is the holding company as far as the UK side goes, is 100% owned by Castle Trust Holdings plc, an offshore company incorporated in Jersey. The board consists of Sean Oldfield (CEO), Matthew Wyles (Executive Director), Julian Dale (CFO), Andrew Macdonald (General Counsel), Barry Searle (COO) and Michael Bevan (MD of Omni Capital Retail Finance).

How safe is Castle Trust? And is Castle Trust protected by the FSCS?

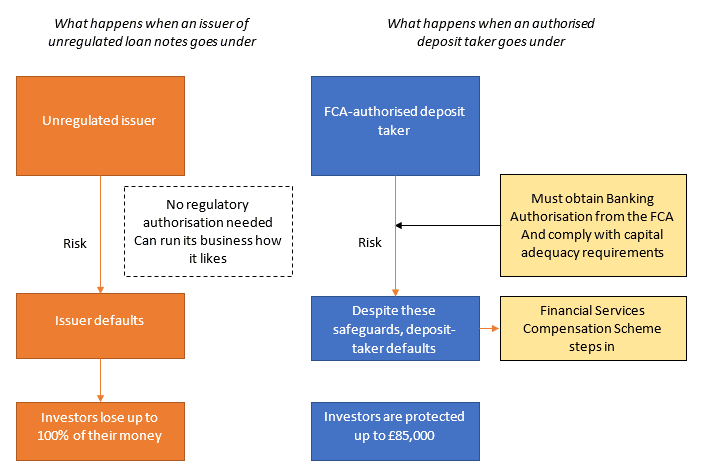

These investments are corporate loan notes and if Castle Trust Direct plc defaults, and Capital Trust Capital plc is unable to honour its promise to repurchase the loans, you risk losing up to 100% of your money.

As mentioned, Castle Trust claims that if Castle Trust Direct plc defaults, and Capital Trust plc is unable to honour its promise to repurchase the loans (as Castle Trust Direct plc represents by far the largest part of Capital Trust Capital plc, it seems highly likely that if Castle Trust Direct has run out of money, the parent company will have too), the Financial Services Compensation Scheme will make good the losses, up to a maximum of £50,000.

This idea rests on Castle Trust’s assertion that “Castle Trust’s legal obligation to buy back Fortress Bonds and Housas is “protected investment business”.”

The FSCS provides cover for investors in the event that, for example, you instruct an FCA-regulated firm to purchase £50,000 of shares on your behalf, and they instead steal your money, and the parent company is unable to make good the losses. This is the kind of thing that is described by “protected investment business”.

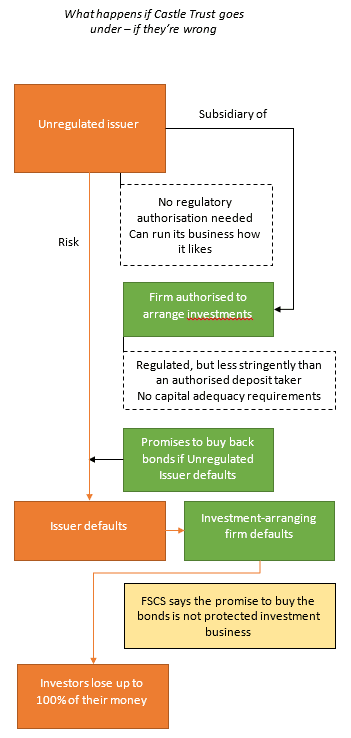

The FSCS does not cover investors who invest in a loan note whose issuer defaults.

Nowhere in COMP 5.5.1 of the FCA handbook does it define promising to buy loan notes in the event of the failure of the issuer as protected investment business.

If it is possible to obtain FSCS cover in this way, why doesn’t every bond issuer set up an FCA-regulated company, have it promise to buy their bonds in the event of default, and by doing so, substantially lower the coupon it will have to pay to attract investors?

If it is possible to obtain FSCS cover in this way, why doesn’t every bond issuer set up an FCA-regulated company, have it promise to buy their bonds in the event of default, and by doing so, substantially lower the coupon it will have to pay to attract investors?

Either every other issuer of loan notes in the country (and for that matter the world, as any company can set up in the UK, and FSCS cover is available to overseas nationals with a valid claim) is missing out on a huge opportunity to lower the cost of its borrowing.

Or Castle Trust’s claim that its loan notes are covered by the FSCS is wrong.

In the footer of Castle Trust’s website, it says “You risk losing capital should Castle Trust become insolvent”. The apparent contradiction between this text and its claim that the FSCS covers the Repurchase Facility is not explained. In our opinion, this section of the website is the accurate one.

Castle Trust will no doubt disagree with our interpretation of the FCA’s rules. Investors should note that in the event that Castle Trust Direct plc and Castle Trust Capital plc become insolvent, it is the Financial Services Compensation Scheme who will decide whether they have a claim, not Castle Trust.

Investors should not expect the FSCS to state one way or the other whether Castle Trust’s claims are accurate; the FSCS makes a decision on whether investors have a valid claim only when a firm actually goes into default. By this point, of course, it is too late for any investor to change their mind.

Investors may assume that as the interest rates on offer are very low given these are corporate loan notes – very similar to what you can get on a fixed-term deposit, which unequivocally is covered by the Financial Services Compensation Scheme – the FSCS must cover Castle Trust’s loan notes as well.

However, the definition of what is a valid claim under the FSCS has absolutely nothing to do with the interest rate on offer. A deposit account is protected by the FSCS – a loan note is not, regardless of what coupon it offers.

Should I invest with Castle Trust?

At time of writing, Atom Bank offers a 1 year bond at 1.8%, while Paragon Bank offers a 5 year bond at 2.4%, marginally lower than Castle Trust’s rates. However, Atom Trust and Paragon Bank are offering deposits, and investors can be virtually certain that should Atom or Paragon default, their bonds will be covered by the Financial Services Compensation Scheme.

With Castle Trust, they are investing in corporate loan notes and relying on the assumption that Castle Trust’s novel interpretation of the FSCS rules is correct.

If investors come to the conclusion they are not willing to rely on FSCS cover, then they should treat these investments as any other corporate loan note – high risk investments which should be held only as part of a wider portfolio.

A cynical person would say that Castle Trust’s rates appear to be calculated more to appear just slightly better than an equivalent deposit account than to reflect the risk of default.

Castle Trust stopped issuing investments linked to house price indices in 2015, but as some of its products were issued with a 10 year term, it will retain liabilities that will go up in line with house price indices until at least 2025. As nobody knows how house prices will move in the next 8 years, this means it is impossible to be certain how much Castle Trust will need to pay out as its legacy HPI-linked investments fall due.

Castle Trust also used to issue mortgages linked to house prices (i.e. if house prices go up the amount you owe goes up), so in theory their HPI-linked liabilities are matched by HPI-linked assets. But investors in their loan notes are bearing the risk that one does not match the other.

Appreciate yiu need to earn money but this site is suddenly full of trashy adverts. Bitcoin, belly fat. Seriously ?

The adverts you see are served by a third party and based on your browser history, like most on the internet. I don’t have any control over them.