Park First previously offered investments in airport car parking spaces with a “guaranteed” yield of 8% in the first two years, followed by “projected yields” of 10% in years 3 and 4 and “projected yields” of 12% in years 5 and 6.

Park First is part of the Group First group of companies, which also owns Store First, which offered a very similar scheme offering “projected returns” of 8% in the first two years.

The Financial Conduct Authority took the view that Park First was promoting a collective investment scheme without authorisation and in December Park First agreed to stop promoting the original schemes and move to a “lifetime leaseback” model, which the FCA agreed was not a collective investment scheme, and therefore not its problem not an activity requiring FCA authorisation.

Money Marketing has now seen details of the new investment and reports that it “offers investors a fixed 2 per cent annual yield plus variable dividends from the management company’s profits.”

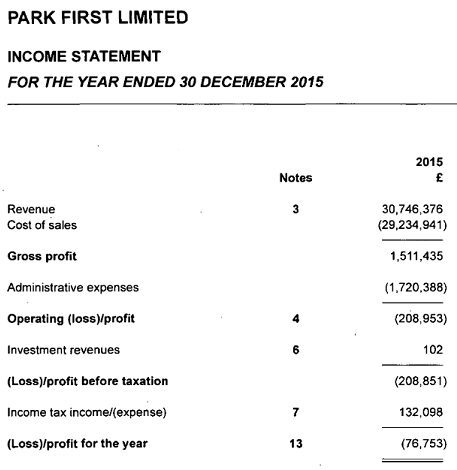

2% per annum plus “variable dividends from profits” – which could be nil – is clearly much less attractive than a “guaranteed yield” of 8%. (Park First’s most recent accounts of 30 December 2015 showed a pre-tax loss of £200,000, so variable dividends will be nil unless profitability improves.)

Furthermore, investors in the original “8% guaranteed” scheme are now apparently being forced to either take up a “buy back option” to get their initial investment back – minus any rental income already paid to them – or switch to the 2% + variable dividends offering. Continuing in the original investment is apparently not an option.

In order to take up the buy back offer investors must hand back title to Group First and then give them a year to sell their space. This would appear to mean that investors must allow Park First to use their money interest-free for a year, plus however long it takes for title to be transferred, to get their original stake back.

In respect of the 2%pa + dividends option, it is questionable how many investors who originally invested expecting guaranteed returns of 8%pa (and 10% and 12% thereafter) would have been willing to invest in a small business in exchange for almost nothing except the hope of future dividends if Park First achieves profitability.

As there is no external market for spaces in Park First’s car park, investors would appear to have no other option available than the buy back option or switching to the new “leaseback” investment.

An investor tells Money Marketing: “I think for the FCA to deem this as a collective investment, and them just let Park First walk away by making a rather clumsy and unpalatable offer of their lifetime lease back scheme is deplorable.

“I have decided to take their buy-back offer, however this offer has many strings attached, like any usage payments would need to be paid back, and that you need to hand back title to the spaces to Park First, which then has a year to sell them. All in all, a great piece of leg work by Park First to make as much out of this as possible.

The FCA suggests that people who have already invested in Park First should seek financial or legal advice about which option to take, and say they will take no further action.

In other words, Park First investors are on their own.

I am also a victim of the parkfirst carpark and together with other investors in hk. We wonder if there is any consumer right in this as this is a one sided determination from ParkFirst to stop the scheme to compile to FCA. Any guru can give some legal advice?

This is an unregulated investment, neither consumer rights nor the FCA apply. You need professional legal advice from a regulated solicitor.

Have you told Park First that you want to opt for the buyback option?

What is HK? Surely not Hong Kong?

I am also a victim of this. Either way there doesn’t seem to be any good choice. If I do the buyback, it will take over a year to get my original investment back. From my understanding It seems I would have got 0% on the investment for 3 years. If i go for life time lease, they say I can keep the original interest but I cannot sell for 5 years. I would get 2% every year. Then they say I can sell privately( seems unlikely) or ask them to find a buyer. They will probably only get 75% of the price I paid or even less. Then they will also charge 5% fee and extra solicitor charges. If I do go for the lifetime lease I may end up getting even less than what I would get from the buyback scheme. Who knows what will happen in 5 years time. They might have got bankrupt and I might have lost everything. I dont know what to do. I really need some advice to decide what I should do. Can anyone please recommend any good financial adviser or lawyer, who knows about this and give me sound advice.

Many thanks

Sindy

Park First’s parent company is £31m in the red (as at June 2017) as a direct result of making a £62m provision to pay back Park First investors. If you get your original investment back in a year that will be an outstanding result.

For the same reason, holding on to your Park First investment for five years in the hope of getting back more than that would be speculative in the extreme. Investors in Store First, Park First’s sister company, which is essentially the same investment only with storage pods in place of parking spaces, have lost all their money (their investments have no yield and no-one wants to buy them).

Whichever option you choose I am afraid you will need to manage your expectations.

Who sold you this investment?

In 2015 I started doing internet search for good return investments. I must have left my phone number on some sites. A company called MCI management rang me and sold me the investment. I wish I had done some more research on it before hand.

I am just now discovering a couple of places where I find other people in the same boat as myself re losing everything with Park First.. i would like to make contact with others if possible to see what if anything, other people are doing re choice of buy back or lease; both to me seems we have all lost everything. It was my first and very naive investment of the money my mum left me when she died,and I foolishly invested it “for my own children” so I am angry not just at myself for being foolish, but at the fact that despite my loss being “my foolishness” it seems crazy that these people are pretty much allowed to go walk free to wash rinse and repeat all over again.I presume I just have to chalk this one up to stupidity?

Were you advised to invest by an FCA-registered adviser?

If not I am afraid you are probably correct to write off the investment.

Your anger is entirely reasonable, but it is not in illegal to run a failed investment. Or more than one.

This investment has been offered in different countries like Brasil, Russia etc. Park First is a scam. After coming out with this pretend agreement with the FCA, neither those who opted for the buyback option, nor those who opted for the lifetime leaseback have seen one single pound in their pockets, while this was supposed to be solved by now. The £ 62 million provision to pay investors is fake! They act in bad faith.

Im now realising that i have probably lost my £25000 investment which leaves me feeling sick. It was money from my divorce which was to form part of my pension. Any advice or help would be much appreciated. I signed up for the long lease as felt there was no other choice. Ive now had a call from a company called Hersall Escrow saying they have a client offering to buy my plot for £40000. Im at a loss as to whether it is a scam or if Park First are even trading (ive emailed this morning). Vicki

Hershall Escrow is a scam, as is Tao Feng Associates or anyone else claiming they want to buy your investment for an implausibly high figure.

According to Companies House Park First are still trading.

Did you invest in Park First within a pension scheme?